In this feature, we talk to a variety of firms and organisations about the Berne Financial Services Agreement which is now in force, and what it means for banks, insurers, wealth managers and others.

When so much attention is drawn by noisy geopolitics, a

development that may have escaped the radar is a

“ground-breaking” mutual recognition trade deal on financial

services between Switzerland and the UK.

The Berne Financial Services Agreement uses “outcomes-based”

mutual recognition of domestic laws and regulations to enable

cross-border trade in financial services to wholesale and

sophisticated clients, as the UK’s regulator, the Financial

Conduct Authority, puts it. The agreement was signed in

December 2023 and took force on 1 January.

Although a global market access framework for the UK held sway

prior to the BFSA, it was more complex. (The previous set-up was

called the “Overseas Persons Exchange Exclusion Framework.”)

“The BFSA makes this simpler and it is easier to manage,” Vanessa

Dubra (pictured below), head of international at the Swiss

Bankers Association, told WealthBriefing in a

recent interview.

Vanessa Dubra

Swiss banks that meet Swiss regulatory requirements don’t need to

be separately regulated in the UK, and vice versa. “For Swiss

institutions not yet in the UK, it offers easier access to the UK

– particularly for smaller banks,” she said. “This agreement is

not just about the relationship between Switzerland and the UK…it

could serve as a model for other financial markets.”

At PIMFA, the UK-based

wealth management industry association, the message about the

BFSA is positive.

“The Berne Agreement is groundbreaking – it uses outcomes-based

mutual recognition of the UK and Swiss regulatory and supervisory

frameworks, rather than harmonisation of rules and, by doing so,

opens a new chapter in cross-border trade in financial services,”

Maja Erceg, senior policy advisor for EU and government affairs

at PIMFA, told this publication.

“For our member firms – UK wealth business – we see this as an

opportunity to expand market access and secure new business

without the additional challenge and cost that come from meeting

specific Swiss regulatory requirements or from securing presence

in Switzerland. “Most obviously, UK client advisors will now

be able to serve high net worth individuals in Switzerland

without registering in Switzerland,” she continued.

“We see this agreement as giving UK firms an advantage over many

international firms who may have to obtain authorisation and deal

with various other restrictions to operate in Switzerland. We

hope that the framework that is now in place will serve as an

incentive for firms and encourage them to be proactive and use

this opportunity to expand the client base into another

jurisdiction,” Erceg added.

The City of London

The Swiss government told WealthBriefing that the

agreement is significant.

“This agreement between two important European financial centres

is a clear commitment to open financial markets and opens up new

opportunities for cross-border cooperation. Now we look to the

private sector to profit from the potential of the agreement,”

Daniela Stoffel, State Secretary for International Finance at the

Federal Department of Finance, Switzerland, said in an

emailed statement to this news service.

Federal government building, Berne

Familiar faces

Swiss banks and other financial institutions are familiar faces

that operate in London as well as the UK regions, such

as UBS, Julius Baer, Pictet, Lombard Odier and Mirabaud, for

example. UK-headquartered banks with operations in Switzerland

include Barclays Bank (Switzerland) SA; Barclays plc; HSBC

Private Bank; HSBC Bank; IG Bank SA; Investec Bank (Switzerland)

AG; Rothschild & Co Bank AG; Schroder & Co Bank AG; Morgan

Stanley plc London, Zürich branch; JP Morgan Securities plc

London, Zürich branch; Goldman Sachs International London, Zurich

branch; and Citigroup Global Markets plc London, Zurich

branch.

The pact opens the prospect of expanded financial services trade

and capital flows between two European countries that aren’t in

the European Union (although Switzerland does have membership of

the Single Market and Schengen area). The deal is

taking force almost 10 years since the UK public voted to

leave the EU.

WealthBriefing asked Duncan MacIntyre (pictured below),

partner at Lombard Odier, UK,

what a bank that operates in both countries thinks of the accord.

MacIntyre is UK region head at Lombard Odier and leads teams

across London, Geneva, Zurich and the Bahamas.

Duncan MacIntyre

“While the largest UK and Swiss firms doing business in each

other’s countries are already regulated and registered in these

places – which means the Berne accord may have limited impact on

what they do – it could potentially be more significant for

independent wealth managers and others looking to get into these

markets,” he said.

The deal tightens trade relations between the UK, home to the

world’s largest onshore financial hub (London) and offshore one

(Switzerland). The UK is also home to plenty of offshore wealth

as well, if one assumes the cross-border nature of a chunk of it.

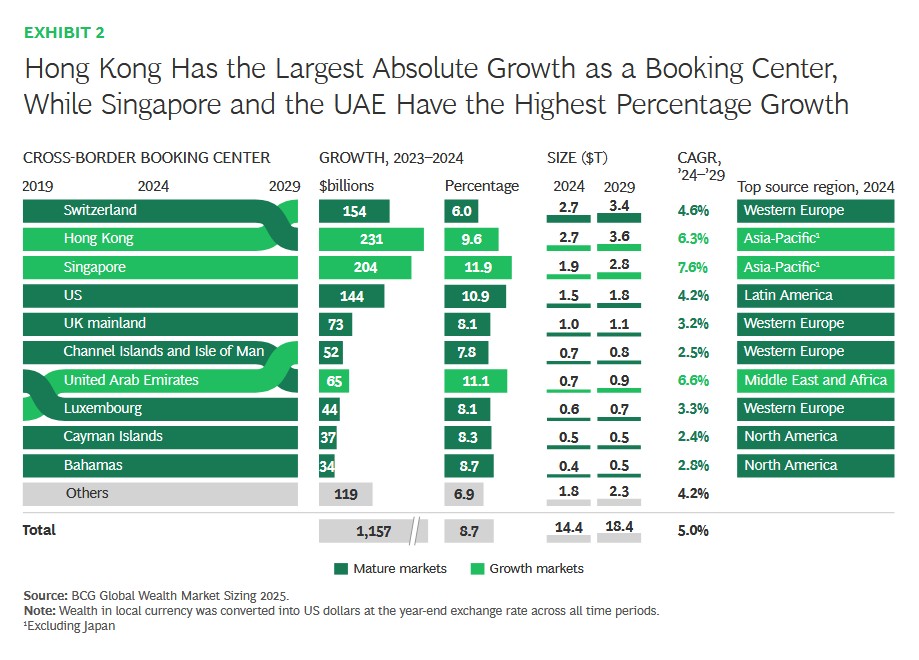

According to Boston

Consulting Group last year, the UK mainland is home to $1

trillion of cross-border wealth; if jurisdictions that are linked

to the UK, albeit with a level of autonomy are included, that

takes the figure to about $2.6 trillion (The Bahamas, Channel

Islands and Isle of Man, Cayman Islands). Switzerland had a total

of $2.7 trillion. And that is just the cross-border part

– it does not include the domestic wealth in both countries.

Cross-border centres, ranked

Source: BCG

“You have got the largest onshore financial centre – the UK – and

the largest offshore financial centre – Switzerland – coming

together,” MacIntyre said.

From the Swiss perspective, the Berne accord is more about the

opportunities for private banking and wealth management; on the

UK side, this has more potential for its insurance industry, he

continued. “It creates a new paradigm. It says `you respect our

laws and we will respect yours’. At the broad level, this [mutual

recognition of standards approach] is a brilliant idea,” he

said.

Streamlining

“The BFSA streamlines regulatory requirements by reducing

duplicative licensing and compliance obligations, enabling

financial institutions to operate in the counterpart jurisdiction

largely on the basis of their home-state regulatory regimes,” Dr

Ariel Sergio Davidoff (pictured below), LLM, TEP, told

WealthBriefing.

Ariel Sergio Davidoff

“Swiss financial institutions are therefore well positioned to

strengthen their competitive standing in the United Kingdom. The

agreement enhances access to one of Switzerland’s most

significant wealth management export markets and allows Swiss

banks to service UK high net worth clients with greater legal

certainty, without the need for local authorisation,” he

said.

High net worth – now an official

concept

The agreement allows Swiss financial services suppliers in

particular to provide cross-border investment services for

professional and “high net worth” clients in the UK in

selected areas.

Interestingly, the concept of “high net worth” is now given a

kind of official status for regulatory purposes. According to the

FCA’s own account of this point, it says “To provide registered

services under the BFSA to a natural person who wishes to be

treated as a high net worth client, the agreement requires a

Swiss firm to satisfy that such a client has net assets of £2

million ($2.71 million) or more.”

British insurance companies can provide cross-border services in

Switzerland in selected areas of non-life insurance. In the area

of financial market infrastructures, the BFSA facilitates the

recognition of central counterparties, strengthens cooperation

between parties about trading venues, and simplifies certain

requirements for over-the-counter derivatives. In the area of

asset management, the agreement sets out the regimes already in

force in Switzerland and the UK.

Conversations with bankers and others suggests that industry

players will take time to work out exactly how the system works

in practice, and how much, for example, will a Swiss-regulated

bank or independent asset manager need to do in compliance and

reporting terms with the UK’s FCA, and vice versa for UK-based

firms seeking to enter the Swiss market.

Preparations

Swiss banks are getting ready.

“Swiss banks have already begun implementing the agreement.

However, as some guidelines were only published in autumn 2025

and the Memorandum of Understanding between the UK and Swiss

supervisory authorities was signed only last September, the

process remains at an early stage,” the Swiss Bankers

Association’s Dubra said.

“Some [firms] have been preparing the business cases and some

will do so in the next few months,” she said.

Kerstin Mathias, director of international affairs at UK Finance, a London-based

trade body representing UK banks, is optimistic.

“We are very positive about it. We see it as setting a gold

standard of an agreement between two well-regulated and

sophisticated financial centres,” she said. There is a

“side-letter” in the agreement – originally signed by the

previous UK government – giving scope for new areas to be covered

in time.

Corridors

The agreement also highlights how jurisdictions, in pushing to

gain a market edge and adjust to new circumstances, carve out

trade “corridors” – a theme this news service has

explored before.

For Switzerland, the pact has taken place when relations with the

EU haven’t always been easy. Switzerland has a mass of bilateral

treaties with the EU on topics as varied as transport, free

movement and agricultural trade. The EU wanted to sweep all these

into a framework pact. Switzerland is not likely to ratify new

agreements before 2027 and will have to hold a referendum

first.

At the margins, the BFSA may give a bit of export revenue hope

for firms in the UK seeking new markets. Even allowing for the

loss of some UK resident non-domiciled wealth from the UK since

the system was closed off by the current government, some of

those persons might have moved to Switzerland – so they

remain in the mix as potential clients.

Switzerland, for its part, has had to adjust over the past decade

after its bank secrecy laws – at least when used by

non-Swiss people – ended. (Bank secrecy remains very much in

force for Swiss citizens, however.)

Davidoff said the Berne deal will influence the kind of treatment

clients receive.

“These regulatory simplifications are anticipated to influence

client-servicing models, enabling cross-border private bankers

and advisors to engage with clients remotely or via periodic

on-site visits, rather than maintaining a permanent local

presence,” he said. “In the asset management sector, the BFSA

affirms existing cross-border fund distribution and delegation

arrangements, creating opportunities for innovative product

offerings and closer collaboration between UK and Swiss firms

under a more permissive delegation framework.

“We are observing keen interest from a range of market

participants, particularly from a technical perspective, with

many seeking clarity on the practical implementation steps

required prior to entering the UK or Swiss market. As reflected

in the practical guidance, the initial steps will invariably

involve legal analysis and clarification to ensure compliance.

There is no expectation of rushed action; rather, a measured,

step-by-step implementation approach is envisaged,” Davidoff

said.

Predictions

PIMFA’s Erceg said the removal of regulatory barriers to UK firms

who wish to operate in Switzerland is “clearly the most important

aspect of this agreement.”

“Costs associated with administration are a hugely important

factor in any cross-border business, and the removal of these

barriers should create unhindered market access and new

opportunities for wealth managers.

“However, it’s important to note that the agreement is not set up

to ensure trade flows in one direction. To this end, it may be

that the most important aspect of the agreement for UK wealth

firms is the £2 million threshold HNW individuals need to meet to

be classified as professional by a Swiss firm.

“In this context, it’s important to note that the FCA is

currently consulting on client categorisation rules in the UK,

and whilst we are supportive of the regulator’s intention to

refresh the requirements to opt clients up to professional

status, their proposed threshold of £10 million is significantly

higher. The risk remains that agreements such as the Berne

agreement may place the UK at a competitive disadvantage going

forward,” she said.

Trade still humming

Almost a decade on from Brexit, the Swiss pact with the UK, along

with other trade deals that countries have signed up to, perhaps

pushes back against the idea that globalisation of financial

services is in retreat.

“The UK’s position as the world’s leading financial centre is

underpinned by its adherence to global standards and its openness

to cross-border trade. In the post-Brexit world, the agreement

shows that the UK can build coalitions with other nations in

Europe in the pursuit of closer economic ties and growth,” Erceg

said. The agreement moves from the traditional EU-style

equivalence to deference – a more flexible model allowing firms

to do business in other markets following their home country”s

regulations. This provides businesses with much needed legal

certainty.

“The dynamic character of the agreement is important, and we

welcome the intention to expand its sectoral coverage to include

sustainable finance in the future too. The two sides have

committed to develop internationally comparable standards for

climate-related corporate disclosures and to align financial

flows with the goals of the Paris Agreement. This is encouraging

as working across borders is nowhere more important than in

sustainable finance,” Erceg concluded.

If you value this content and want to add comments or

contribute ideas, email the editor at tom.burroughes@wealthbriefing.com.