Executive summary

Congress enacted the GENIUS Act in July 2025 to provide U.S. regulatory clarity for payment stablecoins: privately-issued payment instruments issued on a public blockchain. The goal of the GENIUS Act is to facilitate U.S. dollar-backed stablecoin development and innovation while mitigating risks to users and to the stability of the financial system. Towards this end, GENIUS instructs bank regulators and the U.S. Treasury to write rules so users can trust that payment stablecoins will be a viable medium of exchange and a stable source of value, and not be vulnerable to runs or a risk to financial stability.

GENIUS creates a path for nonbank financial firms to compete with banks for payment services by allowing them to obtain a limited federal bank charter to offer payment stablecoins. In addition, the Federal Reserve recently proposed offering limited Fed payment accounts to payment service providers to support innovation and to ensure a safe and efficient payment system. These developments are likely to increase competition for commercial banks that have dominated the provision of payments services because of their exclusive access to the Fed’s payment rails and settlement services.

Since GENIUS was enacted and new bank regulatory guidance has been issued, activity in this market has accelerated with new fintech entrants and banks developing stablecoins, tokenized bank deposits, and the digital payment infrastructure. There are four important open issues for regulators who are implementing GENIUS and for Congress as it considers additional legislation on digital asset market structure. Resolving these issues will determine if stablecoins can become a safe, trusted, and high-integrity payment instrument that can compete with payment services offered by banks—including tokenized bank deposits and deposit tokens—or if they will continue to be used mainly to trade crypto assets.1

The issues:

(1) Should payment stablecoin issuers be able to pay interest or rewards through affiliates or third parties?

GENIUS intends for payment stablecoins to be a medium of exchange, not an investment asset. Banks, especially community banks, are concerned that allowing stablecoin issuers to pay interest could lead to a greater outflow of bank deposits into stablecoins and constrain bank credit. Although aggregate credit likely will be supported through other channels, rapid growth of stablecoins with fast, always-on payment capabilities and redemptions could raise operational risks and undermine the integrity of payments. In particular, the infrastructure is not in place to be able to monetize underlying reserve assets on a 24/7 basis to meet redemptions, nor are regulations and enhanced technologies able to mitigate the attractiveness for illicit finance. Moreover, even if interest or rewards were to lead to faster growth of stablecoins, there may not be much improvement in the fiscal position because any increase in the net demand for Treasury bills from stablecoin growth will likely be offset by the loss of seigniorage from currency to the Treasury as stablecoins reduce the demand for currency. On the other hand, a prohibition on interest or rewards might be easy to circumvent. For example, a stablecoin provider or third party could bundle the stablecoin offering with “free” ancillary services.

- We recommend enforcing restrictions on the payment of interest initially to gain time to assess the impact of stablecoin issuance and usage on the integrity of the payment system and to minimize unforeseen financial and operational risks. As the stablecoin regulatory regime proves its effectiveness over time, these restrictions on the payment of interest could be loosened.

(2) How can regulators ensure stablecoins maintain the singleness of money?2

GENIUS requires stablecoins to have at least a 1-to-1 reserve backing to support a stable value. Permissible reserve assets extend beyond currency and Treasury bills to uninsured bank deposits and cash borrowing with repo (repurchase agreements), both of which can be risky and illiquid during periods of stress. Thus, capital, liquidity, and risk management requirements are needed to ensure redemption at par during stress periods or if an issuer were to fail. Stablecoins created by issuers who cannot ensure a stable value will likely not be adopted because companies have the option of using tokenized deposits for many payment needs; tokenized deposits are backed by strong bank regulations, deposit insurance, and a lender of last resort for backstop liquidity.

- We recommend strong prudential regulations to ensure that a stablecoin holder can always redeem its stablecoins at par even during periods of stress or the failure of the stablecoin issuer. Given that stablecoin issuers offer much more limited services than banks, they do not need the same level and intensity of capital and liquidity regulations as commercial banks.

(3) How can regulators prevent the use of stablecoins in illicit finance?

GENIUS clarifies that a payment stablecoin issuer is subject to the Bank Secrecy Act (BSA) and needs to maintain an AML/CFT (Anti-Money Laundering/Countering the Financing of Terrorism) program. Stronger AML/CFT requirements are needed for stablecoins than for bank deposit tokens because stablecoins are digital cash—a bearer instrument that can change hands anonymously; a stablecoin issuer cannot easily know or control who will ultimately be using its stablecoins after issuance. In contrast, a bank deposit token complies at issuance with AML/CFT requirements and, if made available on a public blockchain, would likely have guardrails to confine transactions to depositors that are also compliant. With a substitute for payment functions available from banks, stablecoin issuers that are unable to demonstrate the capability to prevent illicit financing activities will likely lose corporate and institutional investor clients to those who can.

- We recommend that regulators consider establishing a common global registry of trusted counterparties with which stablecoin users can transact, based on the minimal data necessary to ensure compliance. Such a registry could be developed for banks and tokenized deposits if that were deemed a more efficient means of ensuring compliance than in the current system in which each bank is responsible for its own set of customers and there is considerable duplication of effort.

(4) How can regulators mitigate operational risks such as fraud, cyber theft, and operational outages?

For payment stablecoins that use permissionless blockchains, outstanding issues about governance and resiliency become particularly important when something goes wrong. The traditional financial system has standards and processes to protect customer funds against fraud or bank failure. Stablecoin issuers need to develop and adopt mechanisms to manage disputes and to reverse fraudulent payments in a way that balances providing the intervention necessary to protect users with the initial aims of decentralization on a permissionless, immutable blockchain.

- We recommend that regulators create comprehensive standards to ensure operational resiliency and to encourage further innovation, perhaps in off-chain application and governance layers, to protect users. This should include setting expectations about what outcomes should be achieved, acceptable means for doing so, and periodic evaluations that assess whether stablecoin providers are meeting the regulatory standards.

I. Background

Stablecoins and Tokenized Deposits

GENIUS payment stablecoins are privately offered digital payment assets redeemable at par value and used as a substitute for cash or bank transaction accounts. Such stablecoins would be backed by a dedicated pool of liquid and low-risk reserve assets, on at least a 1-to-1 basis, combined with new capital, liquidity, and risk management standards to ensure convertibility at par. GENIUS makes clear that stablecoins are not a national currency, are not a security, and are not backed by deposit insurance—and stablecoin issuers are not entitled to automatic access to the Federal Reserve payment and settlement services through master accounts. GENIUS directs regulators and the U.S. Treasury to set rules for financial soundness, user protections, and AML/CFT compliance.

Advocates see important benefits to stablecoins. As a new payment instrument, they would bring cheaper, faster, and more efficient payments based on blockchain ledger technology. The ability to embed smart contracts within the stablecoin ledger holds the promise of much greater functionality, with payments being triggered automatically when a particular condition is satisfied (e.g., goods received, services rendered, or a financial market price reached). Because almost all outstanding payment stablecoins are backed by and denominated in U.S. dollars (USD), advocates also say they would support the global use of the dollar and increase the net demand for Treasury bills.

Since the passage of GENIUS, U.S. bank regulators have taken significant actions. The Office of the Comptroller of the Currency (OCC) conditionally granted national trust bank charters to Circle, Paxos, and three other nonbank financial firms in December 2025. More applications are expected. Federal banking regulators issued new supervisory expectations for risk management for banks involved in crypto-related activities, including stablecoin issuance, tokenization of deposits, and custody and other services, and withdrew earlier, much more restrictive guidance.

Also, the Fed is considering offering limited access to the Fed’s payment rails for federally regulated stablecoin issuers with bank charters. A “skinny” master account would cap balances, not pay interest on balances, not have daylight overdraft privileges, and not be eligible for discount window borrowing. It would permit a non-bank stablecoin issuer with a national trust bank charter to directly clear and settle transactions in central bank money, reducing settlement and liquidity risk.3 By facilitating convertibility into fiat currency on Fed payment rails, this would simplify the exchange of stablecoins with bank deposits and cash.

Banks are considering issuing their own stablecoins or offering tokenized blockchain-based deposits, which can provide some of the functionality of stablecoins (see Table 1). In contrast to payment stablecoins, which are backed by a pool of liquid and low-risk assets and tailored prudential regulatory requirements, a blockchain-based deposit is backed by a bank’s capital and the more robust regulatory requirements that apply to banks because they use short-term funds (e.g., deposits) to make longer-term loans. In addition, a tokenized deposit is backed by deposit insurance (up to a limit) and the central bank’s lender of last resort capabilities, safeguards that reduce the risk of deposit runs and financial instability.

Tokenized deposits may meet many needs of users who want faster, more efficient, and functional payments, and may be more attractive to those who want to operate within the banking system. In contrast to stablecoins, which are a bearer instrument, tokenized deposits currently do not circulate independently as a financial asset, reducing the risk they will be used for illicit finance because of existing AML/CFT safeguards. Tokenized deposits generally are offered on a permissioned blockchain or a permissionless blockchain with built-in controls to restrict access to a community of possible users, rather than on an open permissionless blockchain.

Recent activity

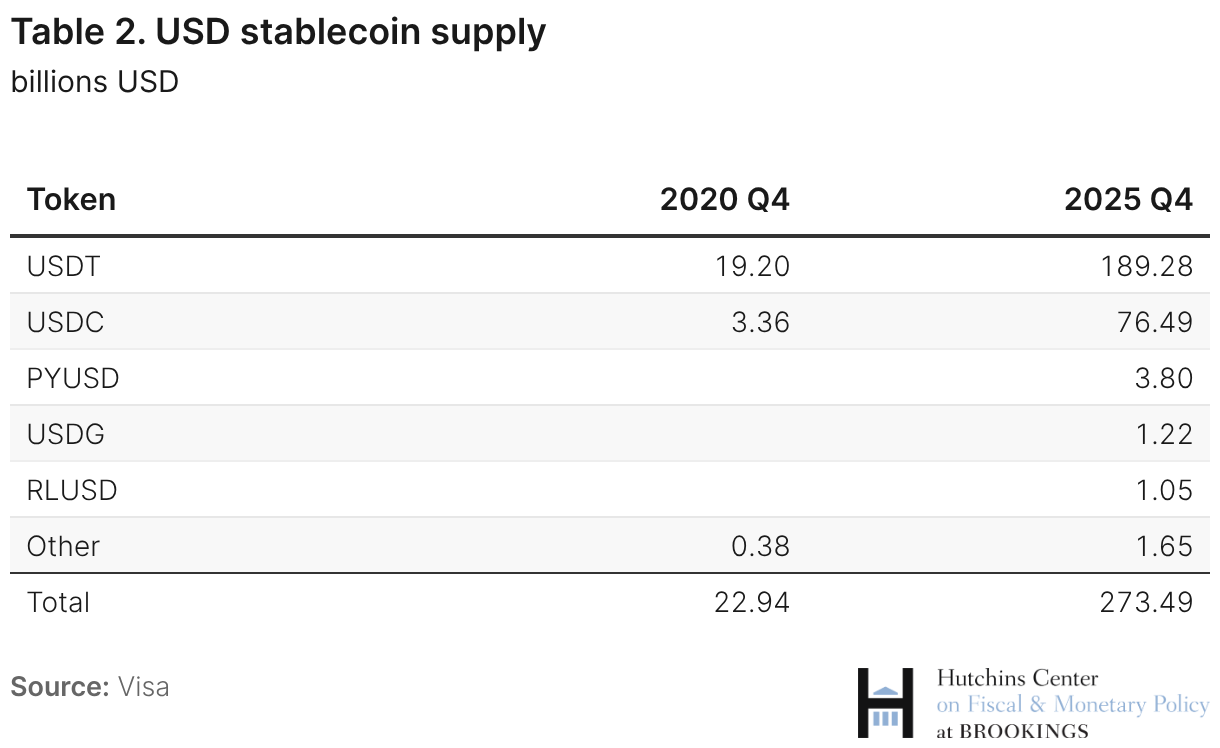

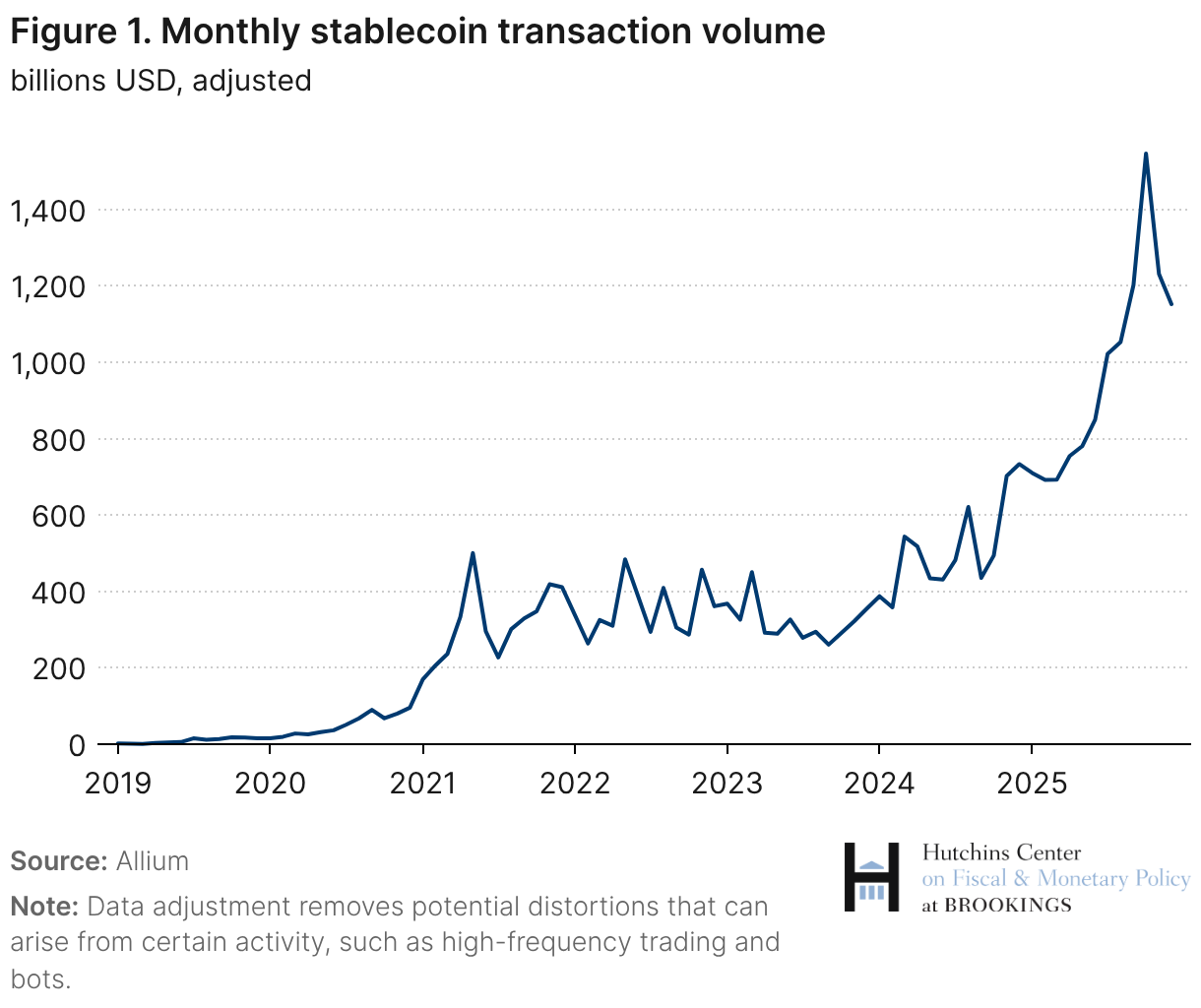

The volume of outstanding USD stablecoins has been growing quickly, rising to nearly $280 billion at year-end 2025 from about $25 billion in 2020 (Table 2). Transaction volumes have increased sharply since 2024 (Figure 1). Supporters predict that much more growth lies ahead. For example, Treasury Secretary Scott Bessent has estimated that the volume of stablecoins outstanding could grow tenfold to $3 trillion by 2030. A recent EY survey of 350 companies reports that while only 13% currently use stablecoins, more than 50% of non-users expect to adopt them in the next six to 12 months. Most expect to use stablecoins for cross-border payments (to suppliers and receipts from customers) and expect that stablecoins will be used for 5%-10% of cross-border payments by 2030, equivalent to $2.1 to $4.2 trillion, according to EY estimates.

Some argue this growth could increase the demand for Treasury bills and reduce the government’s debt-service costs and improve its fiscal position.4 However, as discussed in Box 1, the net impact on debt service costs is likely to be negligible because the new demand for Treasury bills may come at the expense of banks and money market mutal funds (MMMFs), which already invest in Treasury bills. Also, demand for stablecoins from abroad may come at the expense of demand for currency, and the seigniorage of stablecoins would accrue to the stablecoin issuer rather than the U.S. Treasury.

Given that U.S. commercial banks have long-standing relationships with their clients and deposits exceed $18 trillion, the outlook for stablecoins will be heavily influenced by what banks do. Among the 250 nonfinancial corporations in the recent EY survey, 63% would prefer to use traditional banks to implement their stablecoin capabilities, and 68% said they would prefer the stablecoin issuer to be a bank. Some large banks already are offering blockchain-based deposits to existing clients on private internal blockchains. For example, JPMorgan Chase (JPMC) is offering a deposit token to institutional clients on a privacy-enabled public blockchain for global transactions between corporate clients, and Bank of New York is offering tokenized deposits to its clients to improve collateral and margin workflows. On the retail side, some smaller banks are working through consortia to issue USD stablecoins to improve their ability to compete with nonbank payment firms for cross-border remittances and small-business merchant transactions.

II. Open issues

Although GENIUS has spurred activity, important issues remain related to deposit competition, financial stability, illicit activities, and consumer protection. How these issues are resolved will determine whether stablecoins will develop into a safe, trusted, and high-integrity payment instrument that can compete with payment services offered by banks, including tokenized deposits, and become an integral part of an updated payment system–or if they will continue to be used mainly to trade crypto assets.

First, GENIUS intends for stablecoins to be a payment instrument and prohibits the payment of interest by the issuer, which may push stablecoin issuers to compete with bank deposits on payment functionality. Should payment stablecoin issuers be able to pay interest or rewards through third parties or affiliates?

Second, GENIUS does not ensure the singleness of money because the list of permissible reserve assets includes uninsured bank deposits and secured cash borrowing by the issuers, both of which are risky and potentially illiquid. It gives regulators the authority to set capital, liquidity, and risk management standards. How can regulators ensure stablecoins maintain the singleness of money?

Third, GENIUS subjects stablecoin issuers to BSA requirements and requires the U.S. Treasury to set rules for issuers to implement an AML/CFT program to restrain the use of stablecoins for illicit purposes. It also instructs the Treasury to seek public comment to identify methods and techniques to detect illicit finance activity, and for FinCEN to issue guidance and rules within three years. How can regulators prevent the use of stablecoins for illicit finance activities?

Fourth, stablecoins currently lack governance mechanisms to protect users from fraud and lack standards to ensure the continuity of payment services. Moreover, there is a fundamental tension between the decentralization and immutability provided by permissionless blockchains and intervening to protect users from fraudulent acts. How can regulators help to mitigate operational risks, including fraud, cyber theft, and operational outages?

We discuss these four issues below and make specific recommendations to support the development of stablecoins while mitigating emerging risks to financial stability.

(1) Should payment stablecoin issuers be able to pay interest or rewards through affiliates or third parties?

The GENIUS Act clearly intends for payment stablecoins to serve as a medium of exchange, like a bank transaction deposit or cash. It makes clear that payment stablecoins are not a national currency, a security, or an investment asset, and explicitly prohibits payment of interest. The prohibition on interest reduces direct competition from stablecoins for bank deposits and may push stablecoin issuers to compete on payment functionality.

Banks criticize GENIUS because it does not prohibit interest or interest-like awards by affiliates or third parties. For example, Coinbase currently offers rewards for Circle’s USDC, and PayPal offers rewards on its stablecoin PYUSD. Banks are concerned that stablecoins with awards will siphon away deposits and transactions, increasing their costs and reducing their ability to extend credit. The Independent Community Bankers of America argues that community banks would lose substantial deposits if stablecoins were to pay interest, leading to a significant decline in community bank lending (a loss of $1.3 trillion in deposits and $850 billion in loans).

While we come down on the side of preserving (at least for a while) a prohibition of interest and rewards so stablecoins can further develop their payment functionality and reduce the risk of unintended consequences, we believe the argument that a resulting reduction in bank credit provision would be enough to harm the economy is overstated. Banks are responding to competitive threats to offer better payments services by using tokenized deposits, speeding payments with FedNow, and improving their mobile apps—and can also adjust deposit yields to keep those customers they are most vulnerable to losing. Banks and other financial intermediaries still have incentives to extend credit when there are profitable loans to be made. Banks with fewer deposits could securitize loans they originate, and other financial intermediaries can extend credit. There is no strong prima facie case that bundling loans and deposits together on banks’ balance sheets necessarily will lead to greater credit availability in the aggregate or a more efficient financial system.

In addition, the amount of interest that would actually be paid by stablecoin issuers will likely be lower in the future, mitigating this threat to bank deposits. Stablecoin issuers will face higher operating costs as they face more stringent capital, liquidity, and risk management standards to ensure financial and operational resilience, and higher compliance costs to prevent the use of stablecoins for money laundering and terrorist financing. In addition, to the extent that the new reserve requirements restrict holdings of risky assets, they are also likely to reduce stablecoin issuers’ net interest margins.

Moreover, a ban on interest payments through affiliates or third parties will ultimately likely be ineffective and circumvented. In general, such prohibitions rarely work and often have unintended consequences. Consider, for example, Regulation Q, first enacted in 1933, which capped the interest rates that banks could pay on their time deposits. This cap ultimately was repealed in 1980, but only after stimulating the growth of the offshore Eurodollar market and domestic MMMFs. A prohibition of payment of interest creates strong competitive incentives to circumvent the prohibition. On the corporate side, treasurers will figure out ways to maximize the return on their cash assets, as they do today. For example, transaction account balances above a defined minimum are often swept into MMMFs and other interest-bearing assets. Moreover, corporate treasurers may one day be able to automatically convert stablecoins that do not earn interest into tokenized MMMFs and instantaneously convert them back into stablecoins when they are needed to execute payments.

That said, we support the intent of GENIUS to keep stablecoins in the medium of exchange lane for the time being, rather than also functioning as an investment asset. This would reduce the transition risk to stablecoins and limit any unintended consequences from changing the structure of the financial system too quickly. With less rapid growth, stablecoin issuers would have more time to implement effective methods to prevent use for illicit finance and to anticipate and manage new operational complexities. For example, stablecoins involve linking an always-on payment instrument that is convertible into fiat currency to the legacy infrastructure for Treasury bills that operates during traditional hours and may not be able to offer assurance of Treasury sales to cash on a 24/7 basis, which could lead to runs.5 Financial stability risks would also be lower if stablecoin issuers were not too large and interconnected when the bankruptcy process specified in GENIUS is put to the test for the first time. In addition, prohibiting interest payments reduces the financial stability risks of runs into stablecoins during periods of market stress because the opportunity cost to run to stablecoins that do not pay interest is higher than for stablecoins that pay interest. Finally, it is difficult to anticipate at this early point in the evolution of digital ledger technologies how the broader financial system will evolve and what types of payment instruments will be needed or appropriate. Encouraging evolution rather than a revolution seems most prudent at this stage.

Recommendations:

- Congress should reinforce the prohibition on the payment of interest on stablecoins to reduce the risk of disorderly disruptions and to ensure the integrity of the payments system. Regulators might subsequently revisit this issue after Treasury implements stronger rules to strengthen AML/CFT compliance and evaluates the ability of the rules, as well as new methods and technologies, to reduce illicit finance risks, and once stablecoins have demonstrated their financial and operational resilience.

- The Fed should restrict access to “skinny” payment accounts to stablecoins designed to facilitate payments and revisit this issue later. The Fed could define stablecoins that pay interest as not meeting the standard of being predominantly payment instruments.

(2) How can regulators ensure stablecoins maintain the singleness of money?

The singleness of money is fundamental to economic and financial stability. It requires that holders are always confident that their payment stablecoins can be converted at par, that is, that they receive $1 of fiat money for every $1 in stablecoins delivered to an issuer on demand. Because stablecoins are not a national currency but can circulate as a money and payment instrument, widespread adoption could pose risks to the singleness of money if holders were to worry that they could “break the buck.” Such worries could lead to runs and cause stablecoins to trade at a discount to par, reinforcing the run dynamics and disrupting their use for payments. And the consequent liquidation of the assets used to redeem the stablecoins could also lead to disruptions in those asset markets, especially those that are riskier and less liquid.

GENIUS requires bank regulators to set capital, liquidity, and risk management standards to minimize run risk. Because stablecoin issuers are not permitted to take deposits and make loans, as banks do, their prudential regulatory requirements can be lower and simpler than for banks while still being sufficient to support the singleness of money. But because the reserve assets permitted under GENIUS go beyond coin, currency, and Treasury bills, regulations need to reflect the risk of other eligible reserve assets. For example, permissible assets include uninsured bank deposits. As the March 2023 U.S. regional banking crisis demonstrated, uninsured deposits are not always risk-free or highly liquid. Also, when stablecoin reserves are bank deposits, problems at a bank could prompt a run on a stablecoin backed by that bank’s uninsured deposits. Similarly, a stablecoin issuer deemed at risk of breaking the buck could lead to a rapid withdrawal of deposits at banks that otherwise were sound.

Permissible assets also include repurchase (repo) agreements, in which the stablecoin issuer receives cash by acting as a seller of Treasury bills and agreeing to buy back the security the next day. GENIUS limits such transactions except for the purposes of meeting margin obligations or creating liquidity to meet redemption requests. While repo transactions are generally low risk, the provisions would allow stablecoin issuers to borrow, creating leverage. In periods when redemptions were increasing, this could prompt even more redemptions. Moreover, the cash lender would have a priority claim on the Treasury collateral if the stablecoin issuer were to fail, which could cause reserves to fall below 1-to-1 and impair the ability to redeem the stablecoin at par value.

Preventing stablecoin runs is less straightforward than for bank deposits or MMMFs because most stablecoin users do not transact directly with the issuer but instead purchase and redeem stablecoins on the secondary market through arbitrageurs. Prices in the secondary market are determined by supply and demand. Arbitrageurs limit the deviations in prices from par by buying stablecoins in the secondary market when they are trading below $1 and presenting them to the issuer for $1, and selling stablecoins in the secondary market when prices exceed $1. These arrangements are not standardized; they are determined by the issuer. Ma, Zeng, and Zheng (2025) document that Tether, the largest stablecoin issuer, averaged about six arbitrageurs redeeming tokens in a given month, and imposes a lower bound limit on redemptions of $100,000 and charges a fee, the greater of $1,000 or 0.1%.6 In contrast, Circle, the second largest stablecoin issuer, had 521 arbitrageurs in an average month and much lower redemption limits and fees.

Stablecoin redemptions could provoke runs in three ways. First, if there were heavy redemptions, arbitrageurs might demand greater concessions to par. If the discount increased, this in turn could spur greater redemptions. Second, if there were more sales than purchases, this could spill over to the primary market with redemptions by the arbitrageurs from the issuers. Third, this in turn could lead to the sale of reserve assets by the issuer to raise the cash to meet these redemptions. This could push down asset prices and the value of the remaining reserve assets. GENIUS requires that issuers disclose their redemption policy and offer timely redemptions, but it does not require that redemption policies should discourage runs. Thus, it is critical that capital and liquidity requirements are sufficiently robust to ensure that stablecoin holders are never worried about the value they will receive if they wish to sell their stablecoins to the arbitrageurs or present the stablecoins directly to the issuer.

To be sure, if the sole goal is to guarantee the singleness of money, prudential regulations offer a second-best solution compared to full backing by central bank reserves. But given other objectives—including fostering innovation and supporting the reserve status and use of the U.S. dollar—GENIUS provides regulators with sufficient authority to mitigate the risks to the singleness of money for stablecoins. The key will be regulation sufficient to ensure that stablecoins will always be convertible at par, but not unnecessarily onerous so that it undermines the economics of stablecoin issuance and their utility for payments. Finding a sweet spot seems feasible when issuers are earning positive interest on the assets held as reserves, as is the case currently.

The singleness of money could also be threatened if a large nonbank firm were to create an internal closed system of money and payments—a stablecoin that resides on a permissioned blockchain ledger within a single corporate entity. The existence of such walled gardens would increase the barriers to moving easily from one stablecoin to another. Such an outcome could also result in an excessive concentration of power. The nonbank firm could expand from its current business that already had strong network effects, like e-commerce, into payments, reinforcing the network effects and benefits of scale. If the issuer were not a bank, the connection would undermine the long-standing separation of banking and commerce in the United States. These concerns are why Facebook’s Libra (and subsequent Diem) stablecoin proposal was met with intense scrutiny by U.S. and foreign regulators and central banks.

The GENIUS Act addresses the separation of banking and commerce by prohibiting publicly traded nonfinancial companies from becoming payment stablecoin issuers. It also states that stablecoin issuers are subject to anti-tying provisions, though enforcement of anti-tying prohibitions has often proven difficult in practice. The Treasury, Fed, and FDIC (the members of a new Stablecoin Certification Review Committee created in GENIUS) have discretion with respect to the conditions under which a non-publicly-traded firm could issue stablecoins.

Recommendations:

- Regulators should set capital, liquidity, and risk management standards to ensure convertibility at par recognizing that some reserve assets permitted by GENIUS are risky and illiquid. This includes establishing higher standards for issuers who want to hold riskier assets, such as uninsured bank deposits and repo, rather than U.S. coins and currency, deposits at the Federal Reserve, and Treasury bills.

- Regulators should not permit the securities available for repo transactions to be included in the reserves needed for 1:1 backing and held in segregated accounts. This would prevent reserves from falling below 1:1 if the stablecoin issuer failed and could not return the cash and the repo lender seized the collateral.

- Regulators should set standards to encourage the option of timely and low-cost redemption directly from the issuer. This would reduce potential frictions during periods of stress and limit the size of deviations of secondary market prices from par value.

- The Fed should require stablecoin issuers to be subject to robust federal regulation that ensures convertibility at par as a condition for access to its proposed Fed “skinny” master accounts with limited services. Access to central bank settlement will strengthen operational resilience by reducing interdependencies in the correspondent banking system that nonbank payment innovators currently have to use in order to indirectly gain access to Fed settlement.

- Accounting standard setters should not treat stablecoins as a cash-equivalent asset unless the prudential standards set by the regulators can ensure convertibility at par on demand.

- Congress should extend the current prohibition on publicly traded nonfinancial firms becoming payment stablecoin issuers to all nonfinancial firms. This would prevent non-publicly traded technology and e-commerce firms from being able to exploit the network scale advantages of their existing businesses to extend into payments and create an excessive concentration of economic power.

(3) How can regulators prevent the use of stablecoins for illicit finance activities?

One goal of GENIUS is to restrain the use of stablecoins for illicit purposes. AML/CFT standards for stablecoin issuers must be stronger than for banks because stablecoins are bearer instruments and secondary market transactions cannot easily be tracked in real time by the issuer, like physical cash transactions. That is, while an issuer or exchange can vet the customer with whom it interacts directly, it has little control over where stablecoins go when they are used to execute payment transactions by the holder. In contrast, a tokenized bank deposit is not a bearer instrument. Moreover, the speed of stablecoin transactions leaves less time for traditional fraud detection mechanisms to identify and prevent illicit activity.

GENIUS clarifies that a payment stablecoin issuer is a federal financial institution for the purposes of BSA requirements, indicating that issuers that have been subject to money transmitter requirements will now face new, stronger standards. Moreover, stablecoins offered by a foreign issuer may not be offered for trading in the U.S. by a digital asset service provider (DASP) unless the issuer has the technological capability to comply and does comply with BSA requirements. Treasury is required to issue rules to implement AML/CFT and sanctions programs. GENIUS also instructs the U.S. Treasury to seek public comment to identify methods, techniques, or strategies to detect and mitigate illicit finance activity and to conduct research on this issue.7 In addition, FinCEN is required to issue within three years public guidance and rules on implementation of innovative or novel methods to detect illicit activity and tailored risk management standards.

The U.S. Treasury is seeking comment on the development and potential use of four specific technologies listed in the GENIUS Act to advance AML/CFT and sanctions compliance—application program interfaces (APIs), artificial intelligence, digital identity verification, and use of blockchain technology and monitoring. It seeks to promote innovation to streamline compliance, while minimizing the added resource and operational burdens to adopt and use new tools in order to be AML/CFT-compliant.

Stablecoin issuers that develop effective ways to comply with these obligations will likely see greater adoption for payment use than those that do not because companies and institutional investors will not want to be associated with a stablecoin viewed as tied to illicit activities. Companies also can likely turn to bank deposit tokens that inherently have fewer AML/CFT risks for most of their needs. Although all transactions on a public blockchain can ultimately be identified, current practices to block and freeze accounts may be too slow and too late to prevent illicit transactions, even as efforts are being made to improve on-chain tracking and monitoring. Firms also are developing digital credentials to streamline compliance, to help users and service providers verify the identity and know your customer (KYC) characteristics of their counterparties, and to establish protocols to restrict transactions to certain parties with known addresses on public blockchains.

Creation of a common international digital registry of permitted counterparties could reduce the cost of AML/CFT compliance and reduce payment delays and frictions. The registry would be automatically queried when a stablecoin transaction was initiated and the transaction blocked if the counterparty were deemed non-compliant. This registry would operate essentially as a permission layer with common identity verification to join the system and would apply to all stablecoins. Some are concerned that a common registry would be overly restrictive on access or would violate privacy if substantial data were collected and stored. An alternative is to require users to have blockchain-registered certificates based on a minimal level of personal user data in order to transact. Identities would not be exposed unless transactions were marked as suspicious.8 This alternative may not differ materially in the amount of data collected and the length of time stored, but it would differ by allowing some illicit transactions to occur with the response coming only after they were deemed suspicious.

A registry that would block transactions from occurring in the first place has several other advantages. First, it would reduce the complexity and redundancy of the current AML/CFT regime in which many different financial intermediaries have to conduct the background checks and establish the bona fides on a very large, overlapping group of customers. Second, it could take advantage of the smart contract functionality embedded in stablecoins by enabling the inquiry to take place automatically and without any further human intervention. Third, it would create economic incentives (e.g., lower costs, increased ease of use, and less AML/CFT risk) to establish common standards and greater interoperability, which could increase usage globally.

Recommendations:

- To ensure AML/CFT compliance, stablecoin transactions should be restricted to registered private wallets held at regulated custodians that meet international AML/CFT standards.

- Regulators should evaluate the feasibility of establishing a global registry of trusted counterparties with which stablecoin users can transact. Such a registry could also be developed for use by banks and tokenized deposits in order to simplify and minimize the duplication of effort in the current AML/CFT banking regime.

(4) How can regulators mitigate operational risks, including fraud, cyber theft, and operational outages?

Under GENIUS, payment stablecoins are not supported by any explicit government guarantee to ensure their value (unlike insured bank deposits, and issuers have no access to a lender of last resort backstop to provide liquidity during times of stress. This underscores the importance of establishing governance and operational resiliency standards that will ensure that users are not highly vulnerable to fraud or cyber theft, and that stablecoins can be expected to continue to function as payments or be redeemed at par even when operations are disrupted. Can issuers reverse fraudulent payments, or, if a particular blockchain stopped operating, could the stablecoins move easily to another blockchain with no disruption of payment flows or loss of security of ownership rights? Mechanisms to protect users in these situations exist in traditional payments, and work is ongoing to develop them for stablecoins based on permissionless blockchains. For example, Circle announced a pilot mechanism to reverse fraudulent or hacked transactions that would operate on a layer on top of the permissionless blockchain. The pilot illustrates how Circle is trying to balance a decentralized immutable blockchain technology with an expressed desire by users and regulators to intervene to protect users from fraud.9

Recommendations:

- Regulators should establish operational standards that stablecoin issuers must meet to ensure resilience and protect users. Regulators should adopt the principle that the same risk should lead to the same regulatory outcome, recognizing that the regulations for stablecoin payment providers might differ from those for banks given differences in business model, institutional setup, and technology. In addition, the standards could be made proportional with tougher requirements for larger stablecoin issuers, where disruption could pose greater threats to payments and financial stability.

- Such standards should include:

- The outcomes that the regulators want to ensure that the stablecoin issuer can meet. For example, this might include standards for operational continuity (e.g., 99.999% standards).

- The means by which stablecoin issuers would ensure that such outcomes would be achieved. For example, this could include requirements for geographic diversity in terms of operational capacity and the ability to fail-over to backup sites in the case of outages or cyberattacks that disrupt a particular site’s operational capabilities.

- Periodic assessments that the controls, procedures, and operational regimes will be effective in achieving the operational outcomes that the regulators seek. This might include periodic examinations and/or outside evaluations by third parties that the controls and procedures are in place and effective.