In this section, we provide background on (1) affordable housing, (2) the state’s major affordable housing programs and the entities that administer them, and (3) recent efforts by the state to create a more coordinated affordable housing system.

Overview of Affordable Housing

Defining “Affordable Housing.” The term affordable housing is often used in different ways. As used in this brief, it refers to housing for lower‑income people that is deed‑restricted for a period of years (generally 55 years for rental units), with limits on how much occupants have to pay. Affordable housing can include rental or ownership housing, though most affordable housing programs in California focus on increasing the supply of multifamily rental housing (which is the focus of this brief, as well). A “low income” unit or property typically targets people with income levels between 50 percent to 80 percent of the area median income (AMI), whereas “very low income” is between 30 percent and 50 percent of AMI. “Extremely low income” is typically defined as below 30 percent AMI.

Developers Generally Must Secure Public Funds to Finance Affordable Housing Projects. Unlike with market‑rate rental housing, rental income that is expected to come from low‑income housing is typically insufficient on its own for affordable housing developers to obtain a private construction loan or mortgage and to fund ongoing maintenance and other operations costs. Thus, affordable housing developers need public funds for projects to “pencil out.” Generally, the lower the income of the households targeted to live at the property, the deeper the public subsidy that is needed by the developer. Affordable housing developers often must apply for and assemble gap funding from a number of sources, including from local governments (such as proceeds from a city or county housing bond), state, and federal funding. This process is commonly referred to as building a project’s “capital stack.” Below, we discuss state entities that administer California’s major affordable housing programs, including the largest and most ubiquitous source of funding for affordable housing projects—federal tax credits.

Key Affordable Housing Agencies and Programs in California

Historically, funding for and administration of state affordable housing programs has been scattered throughout several departments and entities—including under two separate constitutional officers (the Governor and State Treasurer). Below, we highlight the state’s primary administering entities and programs.

Under the Governor’s Purview

Department of Housing and Community Development (HCD). HCD has several subsidy programs aimed at increasing the supply of affordable multifamily rental housing. HCD’s flagship program is the Multifamily Housing Program (MHP), which provides long‑term, low‑interest (0.42 percent) loans to developers. The vast majority of MHP‑funded units target households at or below 60 percent of AMI, with an average award per project of about $10 million. HCD has smaller, similar‑type programs aimed at the special populations of veterans and farmworkers. (HCD also administers the Infill Infrastructure Grant Program, which does not fund units but provides funding for infrastructure—such as roads and utilities—that supports higher‑density affordable housing in locations designated as infill.) MHP and these other programs have been funded in recent years primarily by a combination of voter‑approved general obligation bonds and direct, one‑time General Fund support. In recent years, HCD awarded more than $500 million annually for these programs. However, with the exception of $120 million one‑time General Fund provided for MHP in the 2025‑26 budget, all bond funds and prior General Fund appropriations have been awarded for HCD’s multifamily rental housing programs. (HCD plans to release a notice of funding availability for the remaining MHP funding in spring 2026.)

California Housing and Finance Agency (CalHFA). Like MHP, the Mixed‑Income Program (MIP) provides low‑interest loans to developers for new rental housing development. MIP tends to target households with a somewhat higher AMI than MHP, supporting units at a mix of incomes between 30 percent and up to 120 percent of AMI. MIP receives about $30 million annually from the state. MIP derives its funding from Chapter 364 of 2017 (SB 2, Atkins), which authorizes a recording fee on certain real estate documents. The amount per MIP award is relatively small, with average awards of about $5 million.

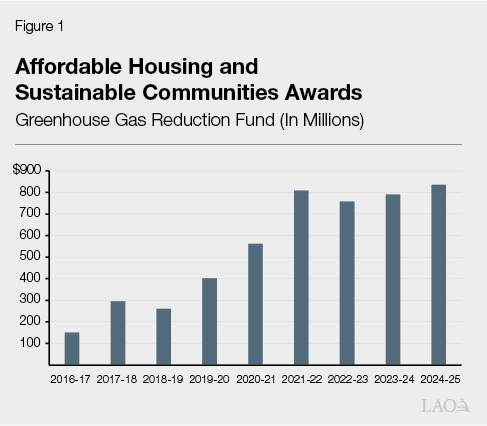

Strategic Growth Council (SGC). A key source of gap funding for developers is the Affordable Housing and Sustainable Communities (AHSC) program. AHSC is funded on an ongoing basis by Greenhouse Gas Reduction Fund, with revenues derived from cap‑and‑invest (previously known as cap‑and‑trade) auction proceeds. The program is statutorily required to receive 20 percent of auction revenue, with at least half of AHSC funding for affordable housing. The purpose of AHSC is to fund projects that reduce greenhouse gases by supporting high‑density, energy‑efficient developments and encouraging transit and “active transportation” (such as cycling). The affordable housing component of AHSC provides a low‑interest loan similar to HCD’s and CalHFA’s programs; the “sustainable communities” component consists primarily of a grant for transportation adjacent to the housing that is built (such as for bus shelters and bike‑path upgrades). Currently, applicants submit a single application with a project proposal that must integrate housing with transportation. Each funded project can receive up to a $35 million award for affordable housing and up to $15 million for transportation (sustainable communities). AHSC is administered by SGC, which develops the guidelines for the program. HCD currently performs a number of programmatic functions for AHSC, including preparing the notice of funding availability, assisting SGC staff with the review and scoring of applications, and disbursing the award monies to recipients. Figure 1 shows total award amounts since the first year of the program.

Under the State Treasurer’s Purview

As described below, the State Treasurer’s Office has two committees that for decades have administered a set of complex funding programs.

Two Types of Federal Low‑Income Housing Tax Credits. Federal low‑income housing tax credits (known as “LIHTC”) are the foundation of the capital stack for virtually all affordable rental housing projects. Developers receiving a LIHTC award generally sell the tax credits to private investors. (Typically, the investor pays somewhat less for the tax credit than the tax credit’s “face value,” such as 80 cents or 90 cents for every $1 in tax credit benefits they receive.) Developers use the resulting equity they receive from the sale of the tax credits to finance their affordable housing projects. Once the housing project is placed in service (made available to tenants), investors can claim the tax credits over a ten‑year period to reduce their taxes. There are “9 percent” tax credits and “4 percent” tax credits, with the 9 percent tax credits generally providing more than double the equity for a developer’s project than a 4 percent tax credit. (The box nearby provides an example explaining the 9 percent and 4 percent tax credits and how they support affordable housing development.) As a result, 9 percent tax credits tend to be used to support construction of developments serving larger shares of very‑low and extremely low‑income households. Figure 2 shows the value of the federal 9 percent and 4 percent tax credits provided to California since 2017.

Understanding the 9 Percent and 4 Percent Tax Credits

How did the 9 percent and 4 percent tax credits get their name and how much subsidy can they provide for an affordable housing project? Below, we provide an explanation using two simplified examples.

A 9 Percent Tax Credit Can Generate a Roughly 70 Percent Project Subsidy… Suppose a developer wanted to build a small multifamily rental complex targeting low‑income households with a cost of construction of $10 million. A federal 9 percent credit would generate a stream of tax credits equal to $900,000 (9 percent x $10 million) per year for ten years, or $9 million in total. On average, though, the developer may only receive about 80 cents in equity per $1 in tax credits sold to investors. As a result, the total actual equity for the $10 million project would be roughly $7 million (80 percent x $9 million). Effectively, then, a 9 percent tax credit may provide a 70 percent subsidy for this hypothetical project.

…While a 4 Percent Credit Can Result in a Roughly 30 Percent Subsidy. A 4 percent tax credit would work in a similar way for a $10 million project. The difference is that a 4 percent tax credit would generate a stream of tax credits equal to $400,000 (4 percent x $10 million) per year for ten years, or $4 million in total. Assuming the developer receives 80 cents per $1 sold to investors, the total actual equity for the $10 million project would be roughly $3 million (80 percent x $4 million), resulting in a 30 percent subsidy for the project.

Figure 2

Since 2017, California Has Benefited

From $40 Billion in Federal Tax Credits

Federal Tax Credits Awarded to Developersa (In Millions)

|

9 Percent

|

4 Percent

|

Total

|

|

|

2017

|

$971

|

$1,249

|

$2,220

|

|

2018

|

1,090

|

2,144

|

3,234

|

|

2019

|

1,115

|

2,416

|

3,531

|

|

2020

|

2,102

|

3,017

|

5,119

|

|

2021

|

1,914

|

3,590

|

5,504

|

|

2022

|

1,177

|

2,801

|

3,979

|

|

2023

|

1,106

|

3,870

|

4,976

|

|

2024

|

1,139

|

4,355

|

5,494

|

|

2025

|

1,180

|

6,399

|

7,580

|

|

Totals

|

$11,795

|

$29,841

|

$41,636

|

Different Processes to Obtain Two Types of Federal Tax Credits. For a 9 percent tax credit, developers apply directly to the State Treasurer’s Tax Credit Allocation Committee (TCAC). TCAC reviews and scores applications and makes awards to winning proposals based on the amount of 9 percent credits made available to the state by the federal government. (States receive an allotment of 9 percent credits each year based primarily on their population size.) In contrast, federal rules require developers to finance a portion of their affordable housing project with “private activity bonds” as a condition of receiving the 4 percent tax credit. Each year, the federal government sets a cap—also based primarily on population size—on the amount of private activity bonds each state is entitled to. (Please see the nearby box for more information about private activity bonds.) Thus, developers seeking a 4 percent tax credit apply to the State Treasurer’s Office’s California Debt Limit Allocation Committee (CDLAC) for their private activity bonds. TCAC then pairs the 4 percent tax credits with the private activity bonds that developers receive from CDLAC. (This pairing of 4 percent tax credits is automatic as long as the developer and project meet specified requirements.) Both TCAC and CDLAC make awards two or three times per year. Upon receiving an award, developers generally are expected to begin construction within 180 days. As a result, CDLAC and TCAC typically are the last stops for developers in building their capital stack.

Explaining Private Activity Bonds

Federal Government Allows for Tax‑Exempt Bonds for Certain Private Projects. Unlike bonds issued by public entities for purely public purposes (like a highway or city hall), bonds issued by public entities for facilities that will be privately owned generally are not tax‑exempt for investors. Federal law, however, allows for state and local agencies to issue a certain amount of tax‑exempt bonds for certain types of private activities described below. (Investors generally are willing to accept a lower interest rate on bonds for which they do not have to pay taxes on interest earned, thus decreasing developers’ financing costs.)

Federal Law Permits Bonds to be Used for Specified Housing and Nonhousing Purposes. Federal law specifies the types of projects that may use tax‑exempt private activity bonds. These projects are deemed as having a “public benefit” and consist of both housing—most notably low‑income rental housing—and nonhousing purposes (including industrial development, waste treatment, desalination plants, and certain other purposes). The federal government sets a cap on the amount of private activity bonds that can be issued in each state per year. The cap is based on population size. In California, CDLAC then allocates the allowed bonds among housing and nonhousing purposes.

Affordable Housing Developers Receiving Private Activity Bonds May Be Entitled to 4 Percent Tax Credits. By themselves, private activity bonds are not a particularly advantageous financing tool for affordable housing developers, since developers must still pay debt service on the bonds (albeit at a lower rate than otherwise given that the bonds are tax exempt). However, federal law makes affordable housing developers eligible for an automatic award of federal 4 percent tax credits (assuming they meet all other eligibility requirements for the tax credits) if they finance at least 25 percent of their construction costs with private activity bonds. (This is a recent reduction from a 50 percent requirement that was in place for many years.) In this way, there is technically an unlimited supply of federal 4 percent tax credits for states—limited only by the federal cap on private activity bonds.

State Tax Credits. California has its own tax credit programs for low‑income rental housing. There are two state tax credit programs: “statutory” and “discretionary.” The nearly 40‑year old statutory state credit, which is continuously appropriated, is adjusted by inflation each year. In 2025‑26, the amount of the statutory state credit is about $130 million. Under TCAC regulations, most of the statutory state tax credits are paired with projects receiving a federal 9 percent tax credit; a smaller proportion of the statutory state tax credits are paired with projects receiving a federal 4 percent tax credit. In addition, every year since 2019‑20, the Legislature has approved $500 million in discretionary (also known as “enhanced”) tax credits. Statute requires all discretionary state tax credits to be paired with projects receiving a federal 4 percent tax credit. (Because the annual amount of state tax credits is so much less than federal tax credits, only a subset of projects receiving a federal tax credit also receive a state tax credit.) Tax credits have a delayed effect on state revenues since investors cannot claim tax credits until units are built and placed in service, which can take several years.

Governance Structures for TCAC and CDLAC. Figure 3 shows that both TCAC and CDLAC have the State Treasurer, State Controller, and Director of the Department of Finance as voting members. (The Legislature does not have representation on either committee.) TCAC and CDLAC have about 80 positions and 20 positions, respectively, and are led by an executive director. (Currently, one person serves as executive director for both committees.) Both committees are funded by fees paid by developers, with no state General Fund support.

Figure 3

Somewhat Different Voting

Memberships of TCAC and CDLAC

|

TCACa

|

CDLAC

|

|

|

State Treasurer

|

✓

|

✓

|

|

State Controller

|

✓

|

✓

|

|

Director of DOF

|

✓

|

✓

|

|

CalHFA representative

|

✓

|

—b

|

|

HCD representative

|

✓

|

—b

|

CDLAC Decides on Share of Private Activity Bonds to Go to Affordable Housing. The federal government specifies allowable uses of private activity bonds. Each state may decide to use them for housing or nonhousing purposes. Nonhousing can include industrial development projects, waste treatment, and certain other types of private projects. CDLAC engages in an annual process to gauge demand for private activity bonds. CDLAC does so by surveying developers each fall on the projects they have in the pipeline and their intent to seek private activity bonds in the following year. CDLAC uses this “demand survey” to help set the amount of private activity bonds to make available by region and for certain other project pools. Then, each January (the beginning of the new round), CDLAC board members formally vote on how much in private activity bonds to designate for affordable housing and other allowable purposes of the bonds.

H.R. 1. Expands Significantly the Availability of Federal Tax Credits. H.R. 1, which was passed by Congress and signed by the President in July 2025, permanently increases the size of the 9 percent tax credit program by 12 percent. For California, this means about $150 million more in 9 percent tax credit authority per year. More importantly, H.R. 1 has the effect of up to doubling the availability of 4 percent tax credits per year—potentially by up to $4 billion annually. This is because under H.R. 1, developers will only need half of the private activity bonds they previously needed to access the 4 percent tax credits (25 percent versus 50 percent of financing). So the amount of private activity bonds does not change under H.R. 1, but the effect is that they are stretched up to twice as far—thus increasing the amount of tax credits.

Recent Efforts to Simplify State’s Affordable Housing System

In some cases, a developer may only need tax credits for an affordable housing project to pencil out. (These typically are for projects intended to house tenants with higher AMI, who will be paying higher rents.) Often, though, funding from the tax credits alone (or tax credits with some local funding) is insufficient, such that developers also need to seek gap funding from state programs. For years, developers have characterized this multistep process as fragmented, siloed, and cumbersome to navigate. Developers often describe significant time and difficulty completing multiple applications for multiple state entities with different time lines and scoring criteria. Additionally, because of the different competitions, developers may secure an award from one program but not from another—thus impeding their ability to secure full project funding. In response, the Legislature has been seeking to simplify the process and move toward a more coordinated funding system, as described below.

Set‑Aside of Tax Credits for MIP. To create a more seamless connection between tax credits and CalHFA’s MIP, statute requires TCAC to set aside up to $200 million of the discretionary state tax credits to pair with projects receiving an MIP award. Additionally, CDLAC has a practice of setting aside private activity bonds for MIP awards (to allow for pairing with 4 percent tax credits). Each year, CalHFA informs TCAC and CDLAC of its estimated need for state tax credits and private activity bonds based on its MIP funding amount.

“AB 519” Workgroup. Chapter 742 of 2023 (AB 519, Schiavo) established the Affordable Housing Finance Workgroup. Chapter 742 requires HCD, CalHFA, and CDLAC/TCAC to convene, study, and make recommendations on the creation of a common application for affordable housing developers and a coordinated review process of applications. The initial report is due to the Legislature by July 2026. In addition, Chapter 742 requires the workgroup to, by January 2026, consider a number of issues in the development of a potential common application and review process, including technical requirements that would be needed and the “optimal means of application completion” by affordable housing developers. The workgroup recently released a draft update that considers two options for doing so, including creating an integrated process for receiving a state subsidy and tax credit.

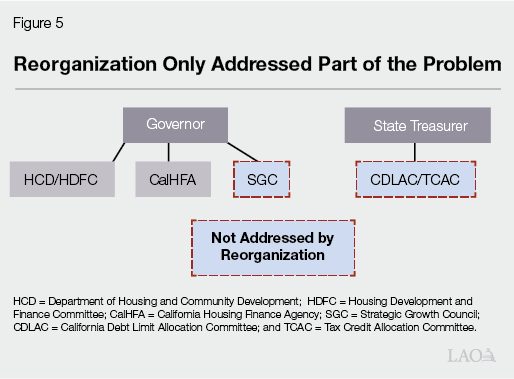

Recent Reorganization Approved a New Agency… Throughout 2025‑26 budget deliberations, the administration pursued a reorganization of the Business, Consumer Services, and Housing Agency through a statutorily defined executive branch reorganization process. The primary stated intent of the reorganization was to (1) have an agency focused on housing and homelessness and (2) create a “one‑stop shop” for developers seeking state funding for affordable housing. In July 2025, the Legislature completed its review of the administration’s plan and provided funding for the reorganization. Figure 4 shows the entities that will be part of the new agency, effective July 2026.

…And a New Housing Finance Entity Within That Agency. As part of the reorganization, the 2025‑26 budget also included initial funding and position authority for a new Housing Development and Finance Committee (HDFC). Led by an executive director, HDFC will be charged with centralizing administration of various affordable housing programs currently administered at separate departments. Figure 5 shows that last year’s reorganization plan addressed part, but not all, of the problem: CalHFA’s subsidy program (MIP) is to join HDFC (along with various multifamily rental housing programs at HCD), but the reorganization did not address how to coordinate with AHSC and the tax credit programs.

Governor’s budget includes several proposals—involving HDFC, AHSC, and private activity bonds and their accompanying federal tax credits—intended as next steps in the streamlining of the state’s affordable housing funding system, as described below.

HDFC

Transfers Positions From HCD to HDFC. The Governor’s budget proposes to transfer six positions (and an accompanying $1.5 million General Fund) from HCD to HDFC as the next step in building capacity at the envisioned new one‑stop shop. Figure 6 shows that, when combined with actions included in the 2025‑26 Budget Act, HDFC would have a total General Fund budget in 2026‑27 of $5.3 million in support of 21 positions. (As discussed below, the Governor’s budget also transfers eight special fund‑supported positions from HCD to HDFC as part of the administration’s AHSC proposal.) Overall, the six positions would be charged with laying the foundation for a newly coordinated funding system at HDFC, including creating a single application for multifamily rental housing programs; developing a common application portal; and, where appropriate, aligning program rules, scoring, and awards processes.

Figure 6

Approved and Proposed Funding and Positions for New HDFCa

General Fund (Dollars in Thousands)

|

2026‑27 Funding

|

Positions

|

||||||

|

Transferred

|

New

|

Total

|

Transferred

|

New

|

Total

|

||

|

2025‑26 Budget Act

|

$1,552

|

$2,253

|

$3,805

|

9

|

6

|

15

|

|

|

January budget proposal

|

1,491

|

—

|

$1,491

|

6

|

—

|

6

|

|

|

Totals

|

$3,043

|

$2,253

|

$5,296

|

15

|

6

|

21

|

|

AHSC

Separates AHSC Into Two Discrete Programs. The Governor’s budget also includes a proposal for HDFC to administer the affordable housing component of AHSC, with SGC to administer the sustainable communities component. Beginning in 2026‑27, developers would no longer be required to submit an application for projects that integrate both aspects (affordable housing and transportation). Rather, they could choose to pursue a project that just builds affordable housing, for example, or just transportation infrastructure. In conversations with the administration, staff indicate that this approach would provide more flexibility to developers to address local needs. Some areas and neighborhoods of the state, for example, might be in need of affordable housing but do not necessarily need transportation upgrades (or vice versa). In addition, administration staff indicate a future desire to incorporate AHSC’s affordable housing component as part of a single application for HDFC awards.

Splits Funding for Each Component Based on Historical Award Amounts. The Governor proposes to provide the affordable housing program under HDFC with 70 percent of total AHSC funding, with sustainable communities receiving 30 percent. This is consistent with past breakouts of funding for the two components of AHSC. Figure 7 shows the Governor’s proposed multiyear expenditure plan for each program. (Actual amounts for each will depend on total revenues received from auctions.) The Governor’s budget provides $396 million in Greenhouse Gas Reduction Funds to HDFC (from what otherwise would have been in SGC’s budget) in 2026‑27, along with eight program‑administration positions currently at HCD.

Figure 7

Governor’s Budget Proposes to Split AHSC

Into Two Discrete Awards

Proposed Expenditure Plan (In Millions)

|

Affordable

|

Sustainable

|

Total

|

Percent for

|

|

|

2026‑27

|

$396

|

$170

|

$566

|

70%

|

|

2027‑28

|

435

|

186

|

621

|

70

|

|

2028‑29

|

475

|

204

|

679

|

70

|

|

2029‑30

|

516

|

221

|

737

|

70

|

|

Totals

|

$1,822

|

$781

|

$2,603

|

70%

|

Private Activity Bonds and Tax Credits

Specifies in Statute the Amount of Private Activity Bonds for Affordable Housing. Proposed trailer bill language requires CDLAC, through January 1, 2037, to dedicate at least 90 percent of total private activity bonds each year for affordable rental housing. The language allows CDLAC, by a unanimous vote, to reduce the amount to 80 percent in a given year and to reallocate unused private activity bonds for nonhousing purposes. The trailer bill declares that establishing a private activity bond “floor” for affordable housing “reflects the statewide priority” to support affordable housing in the state and to “provide certainty in long‑term planning and investment” for developers.

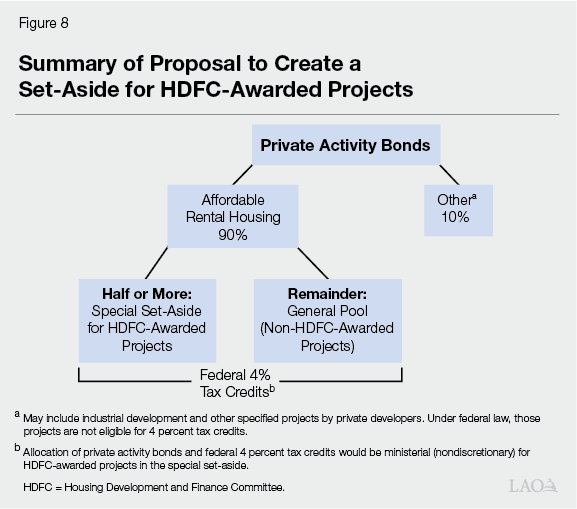

Designates at Least Half of Affordable Housing Private Activity Bonds for HDFC‑Awarded Projects. This proposal would have the effect of creating a special set‑aside of federal 4 percent tax credits exclusively for projects receiving HDFC gap funding (which would include MHP and the affordable housing part of AHSC, among other subsidy programs to be under HDFC’s purview). Under the proposal, CDLAC and TCAC would retain control of the allocation of private activity bonds and tax credits, respectively, but the allocations would be “ministerial” (nondiscretionary) decisions. The stated intent of the Governor’s proposal is to eliminate developers’ need to have to compete for tax credits after receiving an HDFC award—thereby fast‑tracking their capital stack assembly and accelerating time‑to‑construction. The other half (or less) of private activity bonds—and thus tax credits—would be part of a “general” pool that could be used by CDLAC and TCAC for affordable housing projects that do not need or seek an HDFC subsidy. If, by November 1 of each year, there are private activity bonds that have not been allocated to (claimed from) the special set‑aside HDFC pool, proposed trailer bill language would allow CDLAC to re‑designate them for the general pool. Figure 8 summarizes the proposals for the private activity bonds and 4 percent tax credit set‑aside.

Administration Indicates Intent to Leverage Existing Processes to Identify a Set‑Aside Amount Each Year. The proposed trailer bill states that CDLAC “shall reserve at least one‑half” of private activity bonds for HDFC‑awarded projects but does not specify the process for determining a certain percentage each year. In conversations with the administration, staff envision identifying a set‑aside amount using processes that build off current practices. Broadly, this would consist of (1) CDLAC conducting an annual survey of developers about projects in their funding pipeline and intent to seek private activity bonds in the coming year (CDLAC’s existing “demand survey”), (2) discussions between CDLAC and HDFC about the latter’s assessment of resources it will have available to make awards (similar to a process already used to estimate MIP’s set‑aside), and (3) an estimate of what proportion of overall private activity bonds will be needed for HDFC projects. Based on this information, HDFC would then formally request to CDLAC a certain set‑aside amount (such as 50 percent or 60 percent) of private activity bonds (already set aside for affordable housing).

Proposal Is Silent on Federal 9 Percent Tax Credits and State Tax Credits. The Governor’s proposal only creates a set‑aside for the private activity bonds—and thus the federal 4 percent credits. The administration does not address the question of what role the federal 9 percent tax credits as well as the state tax credits would play in the proposed new funding model, including whether or not federal 9 percent and state tax credits also should be set‑aside for projects receiving an HDFC award.

Below, we provide our assessment of the Governor’s proposals. In general, we find merit with the Governor’s overall approach, though in some cases identify opportunities for refinement and improvement.

HDFC

Proposed Resources Transfer to HDFC Is in Line With Legislative Direction. The Governor’s budget is consistent with the policy goals of the reorganization approved by the Legislature in July 2025, which is to re‑envision and implement a more integrated and accessible funding system. The administration’s overall plan is for HDFC to begin making awards beginning in 2026‑27 but with HCD and CalHFA staff providing support over the next year or two as HDFC engages in this redesign work and builds internal capacity.

AHSC

Merit to Moving Affordable Housing Awards to HDFC… Overall, having AHSC’s affordable housing program at HDFC has the potential to simplify how developers build their capital stack. This is because, rather than having programs spread across SGC and other state entities, developers would be able to apply for funding at one place—HDFC. Also, HCD currently plays a key role in the review and implementation of AHSC, so it already has “in house” knowledge of the program. Further, the intent is that this knowledge and program capacity will be transmitted to HDFC through the proposed position transfers from HCD to HDFC.

…Though, for Some Projects, Approach Would Run Contrary to Streamlining Goals. We concur with the administration’s point that no longer requiring applications to include both affordable housing and transportation components would provide more flexibility to developers to address local needs. In some cases, though, developers may wish to obtain funding to undertake both components for a given project. Yet, under the Governor’s proposal, in such cases the developer would have to begin applying in two places: HDFC for affordable housing and SGC for the transportation component—with no guarantee the project would be approved by both entities. Such an approach, though, would work at cross‑purposes with the state’s policy goals of (1) reducing the number of places and times a developer must apply and (2) no longer potentially having scenarios in which a project is approved by one state entity but rejected by another.

Unclear Whether Proposed Funding Split Is the “Right” One. The Governor’s proposal to provide 70 percent of total AHSC funds for affordable housing (and 30 percent for the transportation aspect) is based on the historical split. This split, in turn, is based on SGC’s practice of awarding up to $35 million per project (70 percent) for affordable housing and up to $15 million (30 percent) for transportation. Yet, there is no inherent policy rationale for that 70/30 split. The Legislature may find that the need and demand for affordable housing is different from what is proposed by the Governor and that proportionally more (or less) funding should be provided for that purpose.

Private Activity Bonds and Tax Credits

Merit to Setting in Statute the Proportion of Private Activity Bonds for Affordable Housing. The amount of private activity bonds CDLAC has designated for affordable rental housing in recent years has varied somewhat—from a high of 93 percent to a low of 86 percent. We find that designating the vast majority of private activity bonds for this purpose, as CDLAC has done, is consistent with good public policy given (1) the state’s priority to support more affordable housing and that (2) doing so unlocks federal funding via the 4 percent tax credits. (The federal government does not allow 4 percent tax credits to be used for nonhousing projects receiving private activity bonds.) Setting the percentage in statute, as proposed in the Governor’s budget, thus would ensure that CDLAC’s decisions remain consistent with legislative priorities. In addition, the trailer bill language allows CDLAC some flexibility to reduce the percentage split should future demand for private activity bonds among affordable‑housing developers change for some reason in a given year.

Promising Idea of Providing Tax Credits for HDFC‑Approved Projects… The Governor’s proposed concept of automatically awarding private activity bonds and tax credits to HDFC‑funded projects has the potential to address an important and fundamental problem in the state’s affordable housing funding system: developers having to apply to different state entities for project funding, with no assurance that awards will be made consistently to fund projects. An advantage of the Governor’s proposal is that it builds on a similar process already in place for MIP. Another advantage is that it allows CDLAC and TCAC to retain their authority as technical administrators of a highly complex funding mechanism (private activity bonds and tax credits), rather than attempt to transfer those responsibilities to an entity under the Governor (HDFC) with no such experience or expertise. In addition, the Governor’s approach would retain the ability of developers who are not seeking gap funding through HDFC to apply directly to the State Treasurer’s committees.

…Though the Set‑Aside Amount Needed Will Vary and Could Fall Below Half in Some Years. We do have some concerns with the Governor’s proposal to designate in statute a specific amount of private activity bonds (half or more) that must be set‑aside for HDFC projects. In reality, the amount of such bonds (and thus 4 percent tax credits) needed for HDFC projects will be dependent on several factors—some which cannot be anticipated at this time—and could vary widely. Were a large statewide general obligation bond to pass, for example, state funding for MHP (and likely other gap funding programs) would increase. As a result, many projects would receive an HDFC award, and thus there would be an increase in calls on the proposed set‑aside pool. In years of leaner supplies of state subsidies, however, demand for the set‑aside pool will be much less and a mandatory 50 percent set‑aside for HDFC projects could be too high. This prospect becomes even more likely due to the up‑to‑doubling of the availability of federal 4 percent tax credits resulting from H.R. 1. The drawback of the Governor’s proposed language is that, even if it were clear ahead of time to CDLAC and HDFC that the 50 percent set‑aside was going to be too high in a particular year, private activity bonds could not be re‑allocated until toward the end of the year (when CDLAC would be permitted to transfer unallocated resources to the general pool for other developers to access). In such cases, this rigid approach would result in resources being tied up unnecessarily for most of the year, undercutting the state’s priority of quickly deploying funds for developers to build projects.

State Would Benefit From Leveraging Federal 9 Percent and State Tax Credits Too. The Governor’s budget is in some ways incomplete in that it is silent on the treatment of federal 9 percent tax credits and state tax credits for the proposed set‑aside pool. Because 9 percent tax credits generally deliver more than twice the equity of 4 percent credits, they can be a powerful tool for supporting deeply affordable housing projects (that is, projects targeting people with the lowest income levels). The state tax credits, meanwhile, serve to further enhance equity available for a subset of projects receiving federal tax credits so they, too, tend to support deeply affordable projects. A significant benefit of using 9 percent tax credits for HDFC‑awarded projects is that the state would have the ability to “stretch out” its MHP (and other gap funding) among more projects than otherwise.

Governor’s Budget Lacks a Way to Assess the Impact of Proposed Policy Change. The Governor’s stated goal for his proposals is to reduce time and cost for developers to build their capital stack and construct projects. Yet, as currently proposed, the Legislature would have no way to assess the extent to which policy changes have that desired impact.

Below, we provide our recommendations on the Governor’s proposals.

HDFC

Recommend Approval. We recommend the Legislature approve the proposal to transfer positions and resources from HCD to HDFC, which is consistent the purpose of the reorganization.

AHSC

Approve Proposal, With Two Modifications. First, we recommend the Legislature direct the administration to retain an option for developers to submit a single application for an integrated housing‑transportation project (rather than requiring them to split up their project into a proposal for HDFC and a separate proposal for SGC). Under this approach, a joint committee of HDFC and SGC staff could review and decide on integrated project proposals. Second, we recommend the Legislature require the administration to report back at the end of the 2026‑27 award cycle on demand for (1) affordable housing and (2) sustainable communities—including the number of applications received for each type, funding requested, and qualified applications denied due to insufficient funding. The Legislature could use the data to help decide whether to modify the funding amounts provided for the two components.

Private Activity Bonds and Tax Credits

Approve the Designation of Private Activity Bonds for Affordable Housing. We recommend the Legislature approve the proposal to set in statute a 90 percent floor (with the administration’s language that provides CDLAC some flexibility in given years) for private activity bonds designated for affordable rental housing.

Reject Minimum Statutory Set‑Aside Requirement; Direct HDFC and TCAC to Prioritize Federal 9 Percent and State Tax Credits for HDFC‑Awarded Projects. To avoid situations in which too much is set‑aside in a given year, we recommend the Legislature approve the concept of a set‑aside for HDFC‑awarded projects but remove the proposed language about the minimum having to be at least 50 percent. Instead, the amount should be determined through the above‑mentioned process envisioned by the administration. (Alternatively, the Legislature could choose to specify a minimum set‑aside but allow CDLAC to reallocate unused private activity bonds to the general pool earlier in the year—that is, before November 1.) In estimating the need for tax credits in the special set‑aside pool, we also recommend the Legislature direct HDFC and TCAC to prioritize awarding 9 percent federal tax credits and state tax credits to HDFC‑funded projects targeting the lowest‑income residents. Finally, we recommend that HDFC, CDLAC, and TCAC report to the Legislature each year on where they landed in this process of deciding on allocations for the private activity bonds and each of the tax credit programs.

Add a Reporting Requirement. We recommend the Legislature require HDFC to report periodically to the Legislature on the outcomes of the streamlined funding system. To do so, the administration could compare like‑projects under the old funding system to new ones to identify (1) changes in the total time developers take to assemble funding for their projects and begin construction and (2) the estimated savings to developers. Having a study would allow the Legislature to assess the extent to which the streamlining efforts are having the desired effect.