U.S. Postal Service (USPS) leadership has warned that USPS will exhaust its available cash within the next year. That warning reflects more than a temporary shortfall. After nearly two decades of operating losses, the Postal Service has reached its statutory borrowing limit and cannot finance ongoing deficits through additional debt. This fiscal crisis reflects a structural mismatch between what Congress requires the Postal Service to do and how it is financed.

Americans send far fewer letters than they did two decades ago. Since 2007, First-Class Mail volumes have fallen by more than half as communication has moved online. Yet the universal service obligation (USO) has not changed. Federal law still requires USPS to deliver to 169 million addresses, six days a week, at uniform and affordable prices remains. That nationwide commitment continues to shape the scale and structure of the postal network.

For millions of Americans, particularly in low-density and rural communities, the mail remains essential infrastructure. It delivers prescription medications, ballots, and online purchases, and it supports local small-business activity. In many areas, private carriers do not provide retail access or affordable pricing. The USPS nationwide delivery network ensures that access does not depend on geography or profitability.

The problem is not that the Postal Service has stopped functioning. The challenge is that the financing model designed to support nationwide delivery depends on stable, monopoly-protected letter-mail revenue. As letter volumes have fallen, that revenue base has eroded. The delivery mandate, however, remains fixed.

This primer explains how that mismatch emerged, why retiree and borrowing constraints amplify it, and what policy choices Congress may face as structural deficits collide with a binding borrowing limit. The central policy question is not whether nationwide mail delivery has value. It is whether the financing framework Congress enacted decades ago still works in a digital economy.

The financial model is embedded in statute

The Postal Service’s financial model is defined by federal law. Postal operations have long been funded through the sale of postage and related services, but the Postal Reorganization Act of 1970 formalized the expectation that the modern U.S. Postal Service operate on a largely self-sustaining basis rather than rely on routine annual appropriations. Nationwide service was to be financed primarily through the products the Postal Service sells.

A central component of that model is the Postal Service’s statutory monopoly over certain categories of letter mail. By granting USPS exclusive access to First-Class and other letter delivery, Congress prevented carriers from competing for the then-most profitable segments of the market. The economic value of that monopoly—generated by high-volume, high-margin letter mail—was intended to support the cost of maintaining a nationwide delivery network. In effect, monopoly-protected letter revenue finances the universal service obligation at uniform prices.

Subsequent legislation adjusted how that model operates. The Postal Accountability and Enhancement Act (PAEA) of 2006 modified rate-setting rules and introduced new financial obligations, with significant implications for the Postal Service’s balance sheet. The Postal Service Reform Act (PSRA) of 2022 later removed some of those requirements while codifying elements of the universal service framework.

These reforms changed important elements of USPS’s financial structure, but they did not alter the underlying self-financing model. The statutory framework continues to rely on revenue from mail and shipping to sustain nationwide delivery. But not all revenue supports the system in the same way. This distinction is central to understanding why leadership is warning of a near-term cash drawdown.

Letter mail volumes have fallen sharply

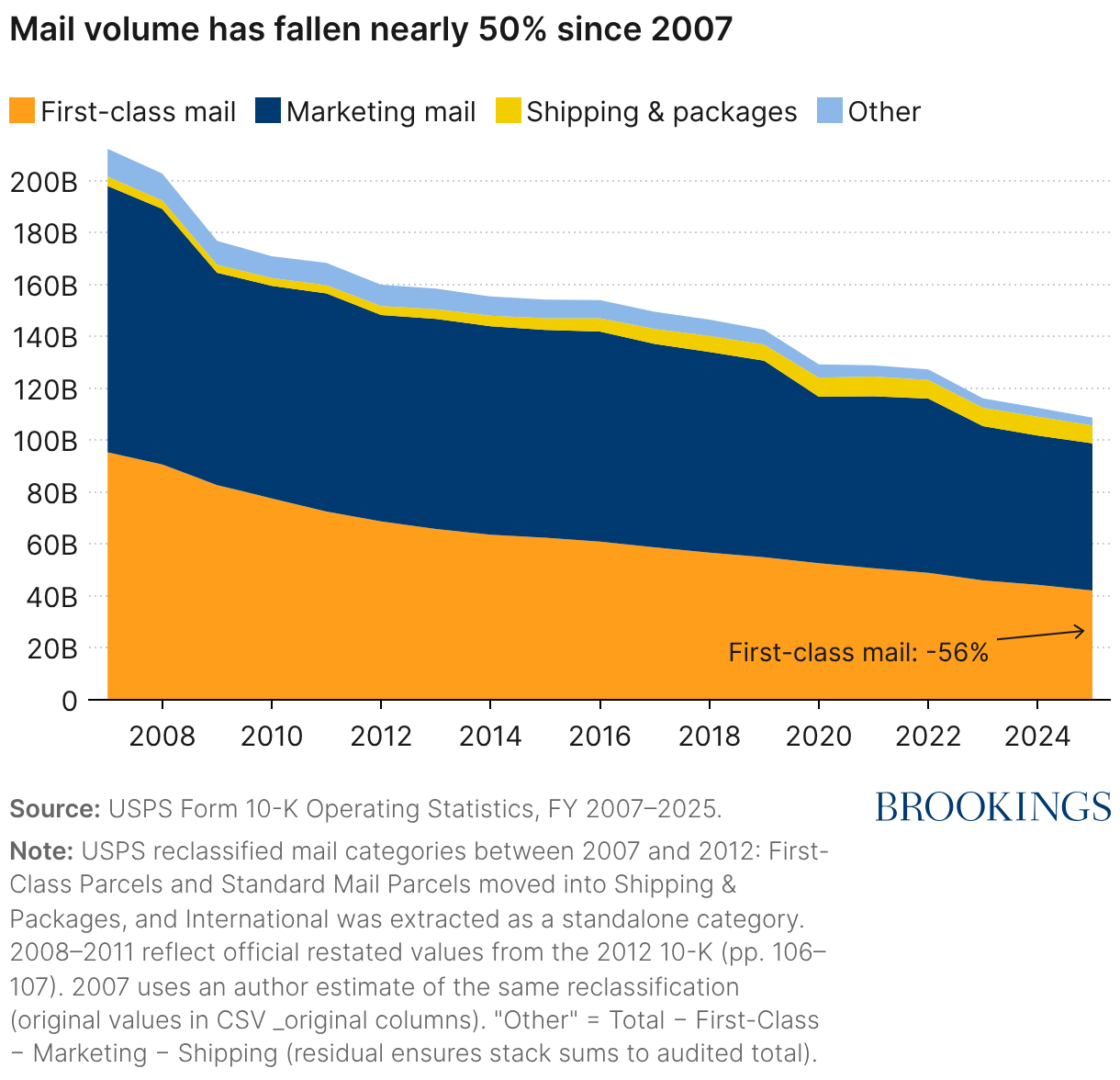

The financial structure described above depended for decades on stable letter mail volumes. That foundation has weakened. Since 2007, First-Class Mail volumes have fallen by nearly 56%, while Marketing Mail has declined by roughly 45%; in total, overall mail volume has dropped by nearly 49% (Table 1). Over the same time period, the broader U.S. economy has expanded significantly, underscoring that the decline in mail reflects technological substitution rather than a temporary downturn.

As Figure 1 shows, the decline in letter mail has been steep and sustained. Although Shipping and Package volumes have grown—rising by nearly 90% since 2007—these gains remain small relative to the scale of letter mail losses. The defining feature of the past two decades is therefore the contraction of the letter-based system that once anchored postal finances.

Figure 1

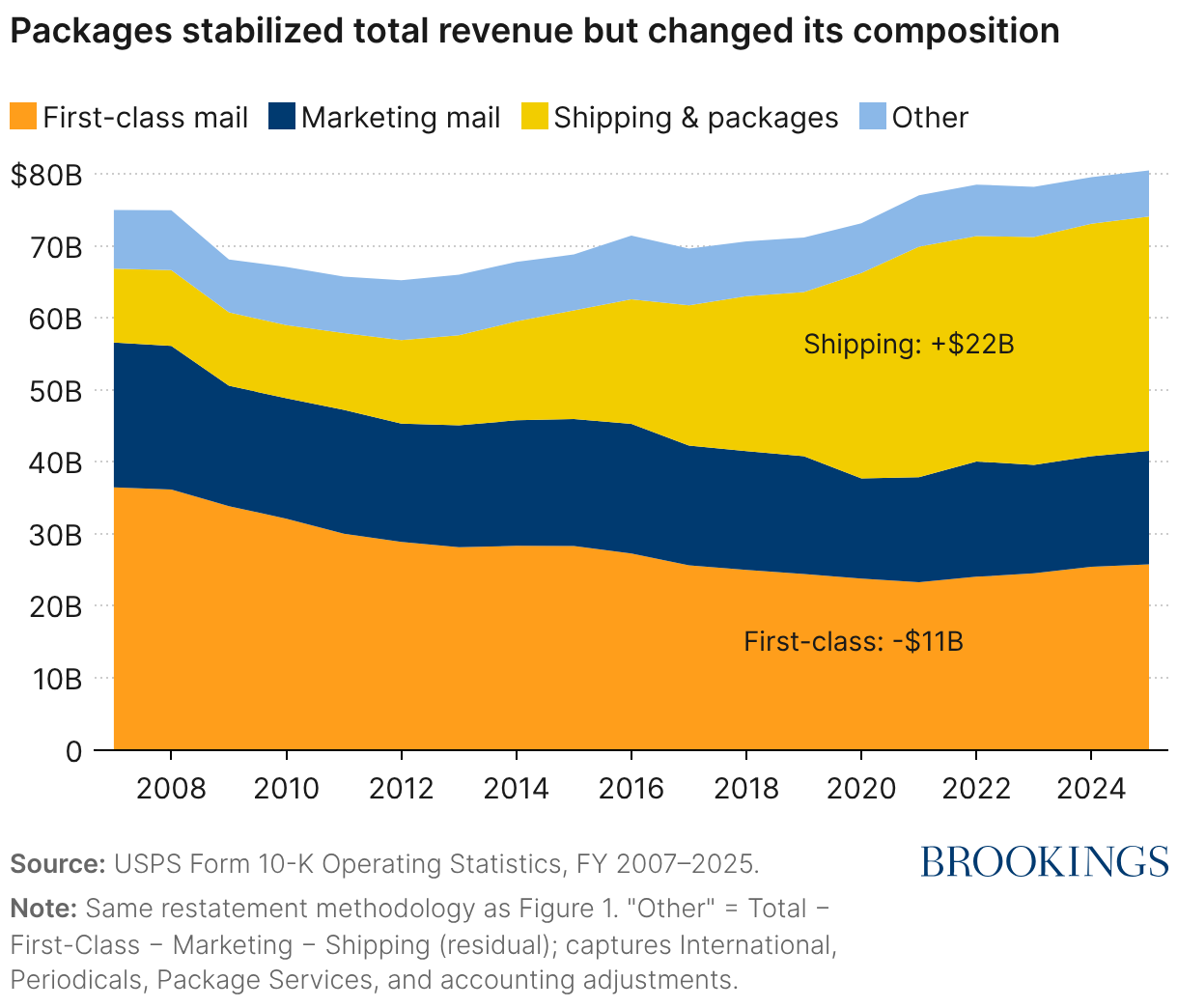

While total mail volume has fallen sharply, total operating revenue has not declined in proportion. As Figure 2 shows, revenue from First-Class Mail has fallen from $36.4 billion in 2007 to $25.8 billion in 2025, a decline of roughly 29%. Marketing Mail revenue has also declined, though more gradually. Over the same period, however, revenue from Shipping and Packages has risen from $10.3 billion to $32.6 billion. As a result, total operating revenue in 2025 is slightly higher than it was in 2007, despite the nearly 49% decline in total mail volume.

Figure 2

This shift matters because the composition of revenue has changed. The system once depended on letter mail, most of which is subject to statutory protections and regulated pricing. Today, a much larger share of revenue comes from package delivery, where USPS competes directly with private carriers. In 2007, Shipping and Packages accounted for roughly 14% of total operating revenue; by 2025, that share had grown to roughly 40%. Over the same period, First-Class Mail’s share fell from nearly 49% to roughly 32%.

In competitive markets, margins are disciplined by market forces rather than supported by statutory exclusivity. As a result, margins are typically narrower than in protected markets. As revenue shifts towards competitive parcel products, the capacity of the system to generate surplus to support nationwide service becomes even more challenging—even if total revenue appears relatively stable. In other words, a revenue base that looks “flat” on paper can translate into less cash generation in practice.

Operating expenses have exceeded revenue for nearly two decades

Despite relatively stable topline revenue, USPS has faced a financial shortfall every year since 2007. As Figure 3 shows, total operating revenue has fluctuated within a relatively narrow band below total operating expenses throughout the entire window. As a result, a consistent feature of the past two decades is a persistent gap between revenues and expenses.

Figure 3

Notably, even as package revenue has increased, the organization has not returned to a durable operating surplus. This likely reflects the persistence of costs tied to maintaining a nationwide delivery network. USPS must maintain routes, facilities, and workforce capacity to serve every address, regardless of shifts in product demand. Changes in revenue mix do not alter the scope of that mandate.

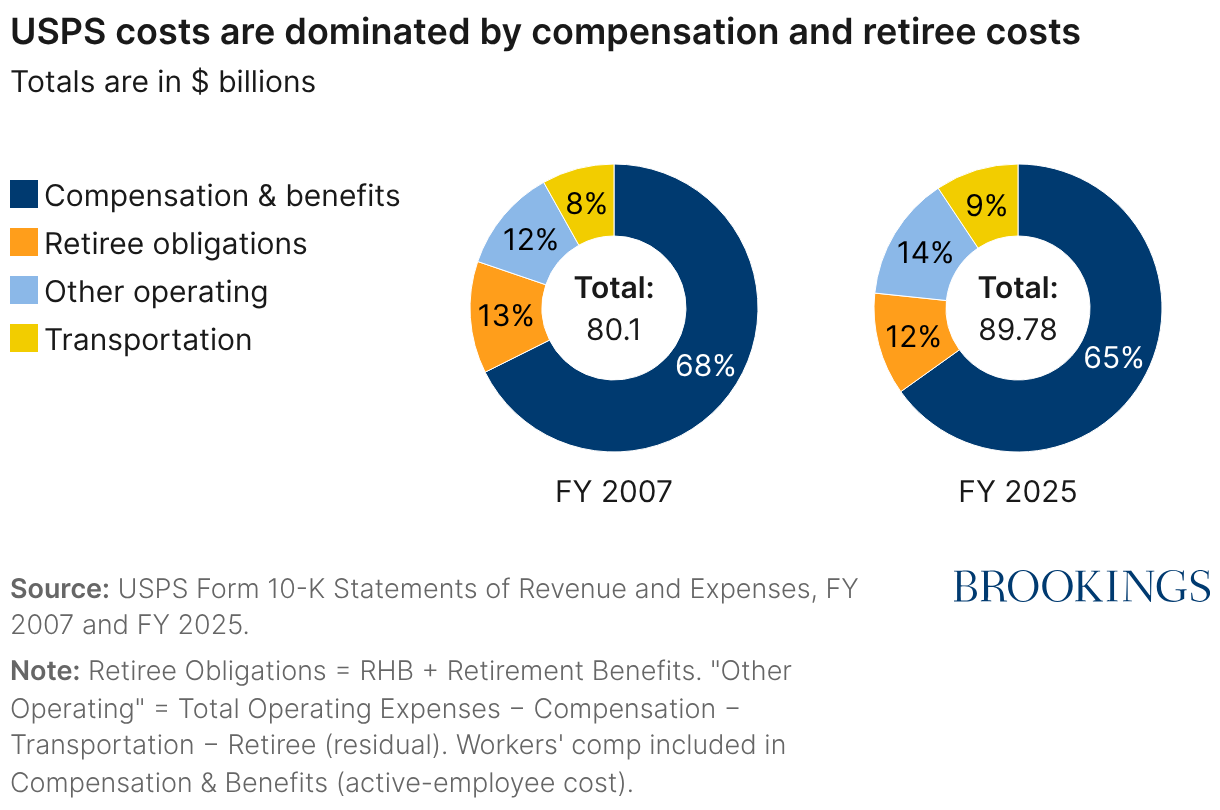

Most USPS costs are tied to compensation and legacy obligations

As Figure 4 shows, compensation and benefits account for the majority of total operating costs—68% in 2007 and 65% in 2025. Transportation and other operating expenses make up most of the remainder. These are the routine costs of sorting, transporting, and delivering mail and packages across the network.

Figure 4

Retiree and legacy obligations account for a smaller but still material share of expenses: 13% and 12% in 2007 and 2025, respectively. In recent years, retirement-related costs have been about $10 billion annually. In 2007, these costs were driven largely by retiree health benefit pre-funding required under PAEA. By 2025, they reflect pension amortization payments determined by the Office of Personnel Management (OPM).

Strikingly, this suggests that while the composition of USPS revenue has changed substantially over the past two decades, the composition of its costs has not. The organization remains labor-intensive, and long-term benefits commitments continue to represent a meaningful share of expenses. In other words, changes in what USPS sells does not automatically change what it must spend.

Retirement costs are financed differently for USPS than for most other federal groups. While federal agencies receive annual appropriations to cover required employer contributions—and Treasury makes amortization payments for non-postal agencies—USPS must fund its retiree obligations from operating revenue. When retirement liabilities increase, the financial impact flows directly into USPS’s operating results.

With this in mind, retiree benefits have long been a meaningful component of USPS expenses. In the years following the PAEA, retiree health benefit prefunding dominated annual retiree charges. These prefunding payments were fixed and front-loaded, and they coincided with the steep decline in mail volume during the Great Recession. As a result, retiree health prefunding contributed meaningfully to reported losses beginning in 2007.

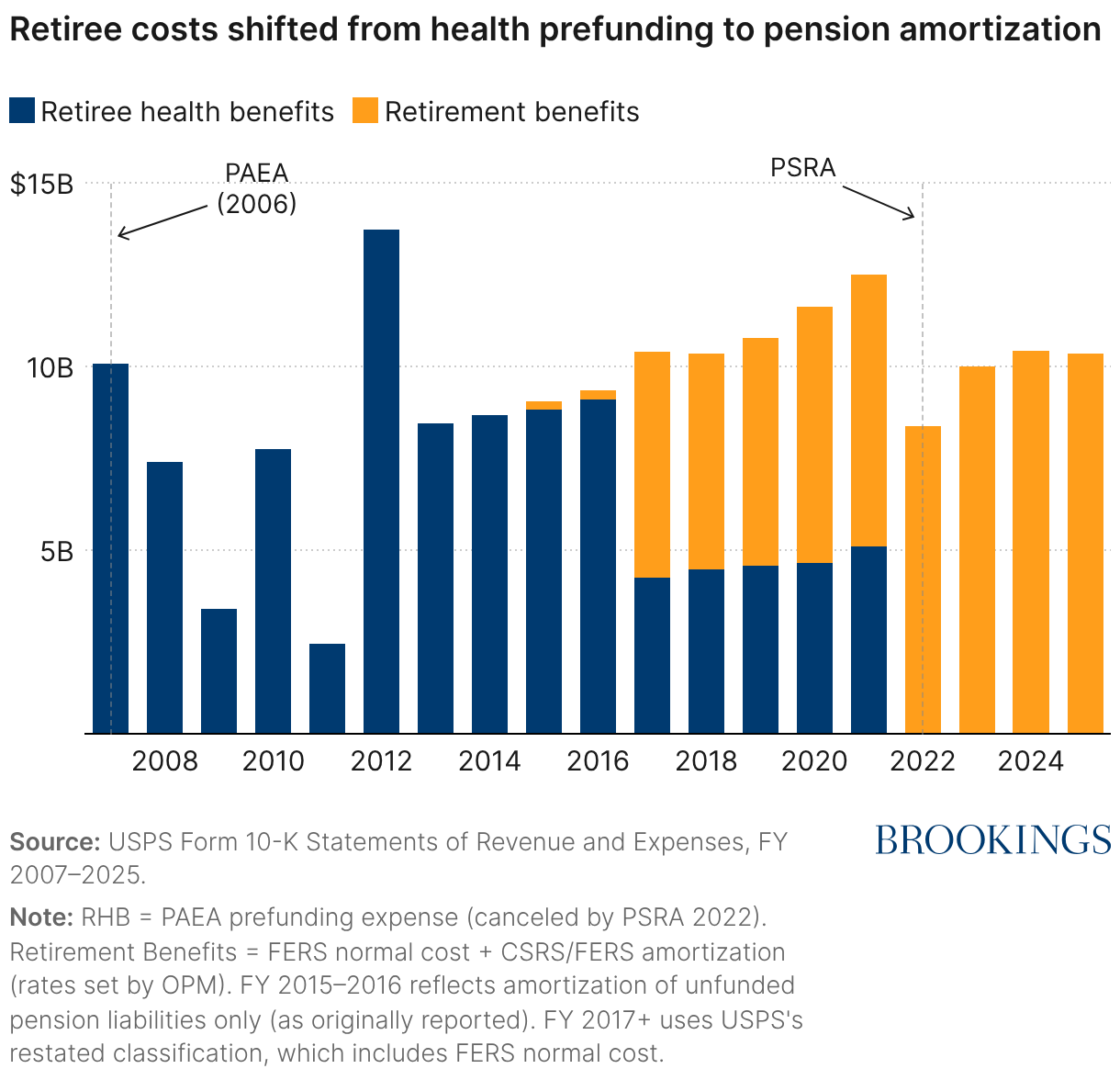

The PSRA eliminated the retiree health prefunding requirement, removing a major accounting burden from USPS’s financial statements. However, retiree costs did not disappear. Instead, required pension amortization payments—a part of total retirement benefits expenses—have grown to replace them. Pension amortization represents scheduled payments to cover shortfalls in the retirement trust funds, or the gap between projected future benefits and the assets currently available to pay them. As Figure 5 shows, annual retiree costs have remained substantial even as their composition has tilted from retiree health prefunding to pension related expenses.

Figure 5

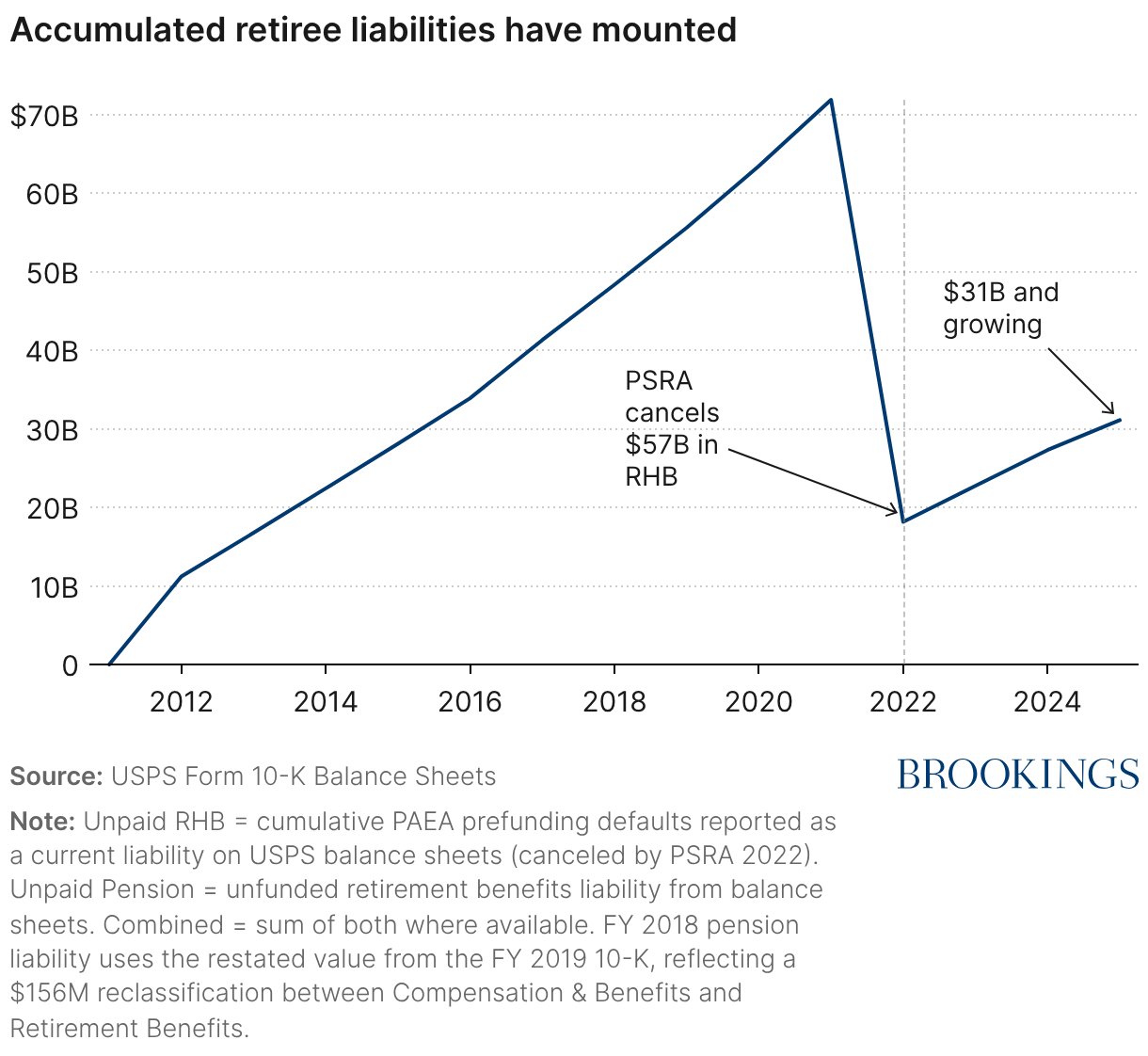

In recent years, required retiree-related payments—including both retiree health prefunding under PAEA and pension amortization payments—have approached or exceeded $10 billion per year. USPS, however, has not consistently made the full payments required for either category. Instead, unpaid amounts accumulate as liabilities on its balance sheet. As Figure 6 shows, the cumulative balance grew to more than $70 billion in 2021—or roughly 93% of total operating revenue. The next year, Congress eliminated roughly $57 billion in retiree health prefunding obligations under the PSRA. Pension amortization liabilities, however, continue to accrue, leaving approximately $31 billion (and growing) in unpaid obligations.

Figure 6

These pension amounts are determined by OPM under federal retirement statutes. USPS does not control the actuarial assumptions, cost-of-living adjustments, investment policy, or contribution rates that influence the size of these payments. Because the underlying liabilities are recalculated annually, required amortization payments can rise or fall materially from year to year. This structure makes retirement costs significant, volatile, and largely outside USPS’s operational control, introducing earnings volatility that is unrelated to underlying delivery operations.

Retiree obligations materially shape reported operating results

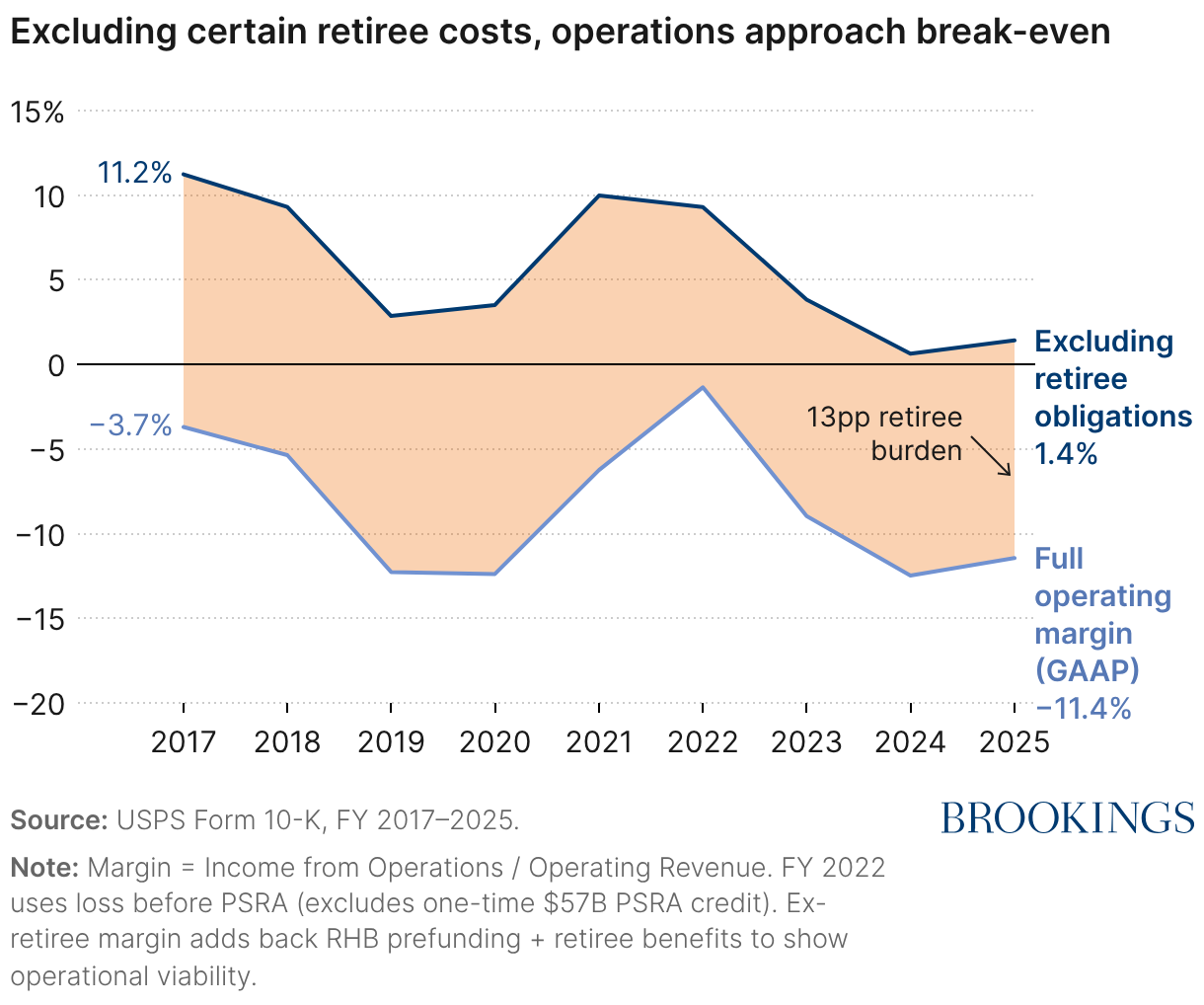

In 2025, total USPS operating revenue was approximately $80 billion, and total operating expenses were approximately $90 billion, with retirement benefits accounting for $10.3 billion of those expenses. Including retiree obligations, USPS reported an operating margin of approximately -11.4% in 2025. Excluding retiree charges, the operating margin improves to approximately 1.4%, as shown in Figure 7.

Figure 7

In fact, retiree costs account for the difference between near-operational balance and substantial reported losses over the last several years. In other words, the day-to-day business of collecting, sorting, transporting, and delivering mail and packages to 169 million addresses generates revenue that is much closer to covering current operating expenses than headline loss figures suggest. Once retiree costs are included, however, the operating margin turns negative.

This distinction does not imply that retiree costs are optional or inappropriate. These commitments are binding and must ultimately be financed. Rather, it clarifies the structure of the financial strain faced by USPS. Reported losses reflect not only the economics of current mail and package delivery but also the financing of legacy obligations that are externally governed and funded from operating revenue. Because USPS receives no general taxpayer funding for these costs—unlike most federal agencies—current postage and package revenue must absorb them. As letter mail volume has declined, that revenue base has become less able to absorb both current operating costs and these legacy obligations simultaneously.

Persistent deficits have translated into liquidity risks

Operating deficits do not immediately produce insolvency if an institution can borrow or draw on reserves. For many years, the Postal Service relied on both. That flexibility is now limited. That’s why a long-running structural deficit now shows up as an oncoming liquidity crisis.

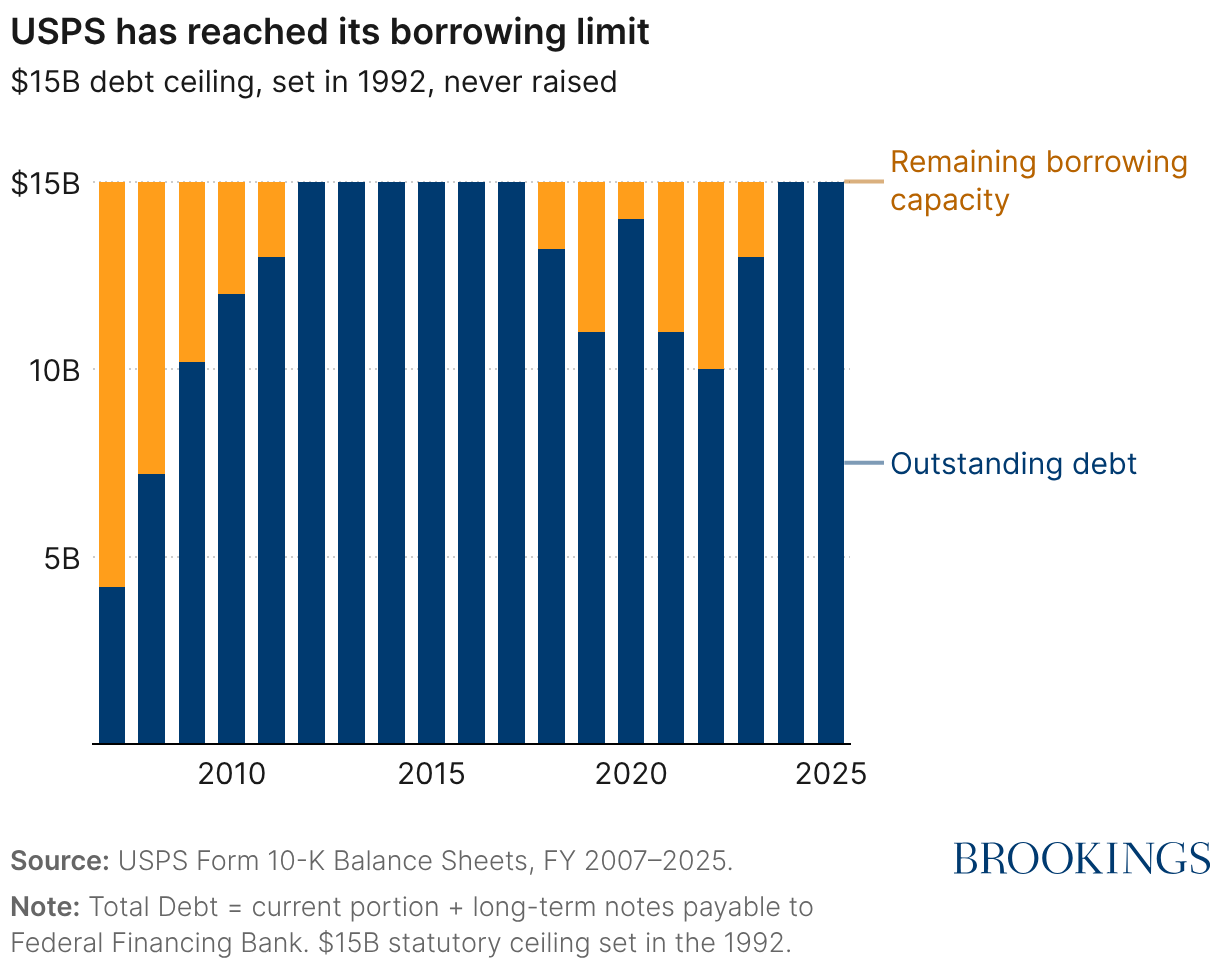

USPS may only borrow from the U.S. Treasury and only up to a statutory ceiling of $15 billion. This ceiling has been in place since 1992 and has never been adjusted for inflation or delivery-point growth. USPS cannot access private capital markets, issue bonds, or raise equity capital. When annual expenses exceed revenue, Treasury borrowing is the only formal backstop.

As shown in Figure 8, USPS first reached its $15 billion borrowing limit in 2012. Although over time some debt was repaid, the organization again hit the ceiling in 2024. As a result, it functions as a hard constraint on the institution’s ability to absorb ongoing deficits, consistent with recent statements from the postmaster general indicating that the Postal Service will soon run out of cash.

Figure 8

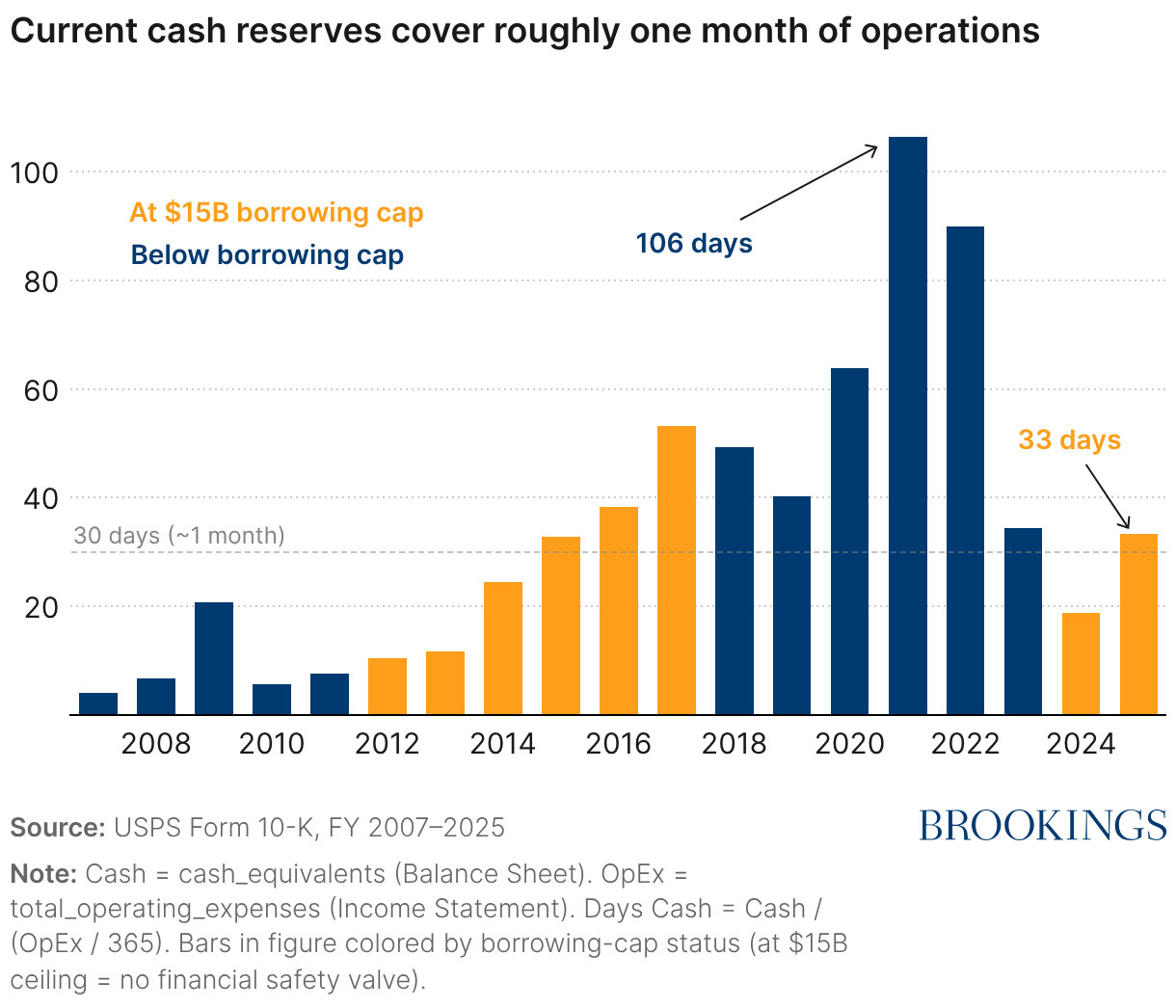

Borrowing constraints would be less consequential if the Postal Service maintained substantial cash reserves. It does not. As shown in Figure 9, days of cash on hand have fallen significantly over time. USPS ended 2025 with approximately $8.2 billion in cash. With annual operating expenses approaching $90 billion, that cash balance covers approximately 33 days of operation.

Figure 9

With no remaining borrowing capacity and no access to private capital markets, ongoing deficits cannot be financed through additional debt. When current annual operating losses (roughly $9-10 billion per year) interact with just one month of liquidity, structural imbalance effectively becomes a binding financial constraint. In practical terms, this helps clarify the immediate meaning of “out of cash”—without a backstop, normal deficits can no longer be carried forward.

The monopoly no longer fully funds the universal service obligation

The Postal Service’s financial model rests on a simple institutional logic: Revenue from protected letter-mail products is intended to support universal delivery at uniform prices. Federal law grants USPS exclusive access to certain categories of letter mail to prevent private carriers from serving only profitable routes. In exchange, USPS operates under rate regulation and service standards overseen by the Postal Regulatory Commission (PRC). In this way, the value of its monopoly rights is a crucial part of the financing mechanism for universal service.

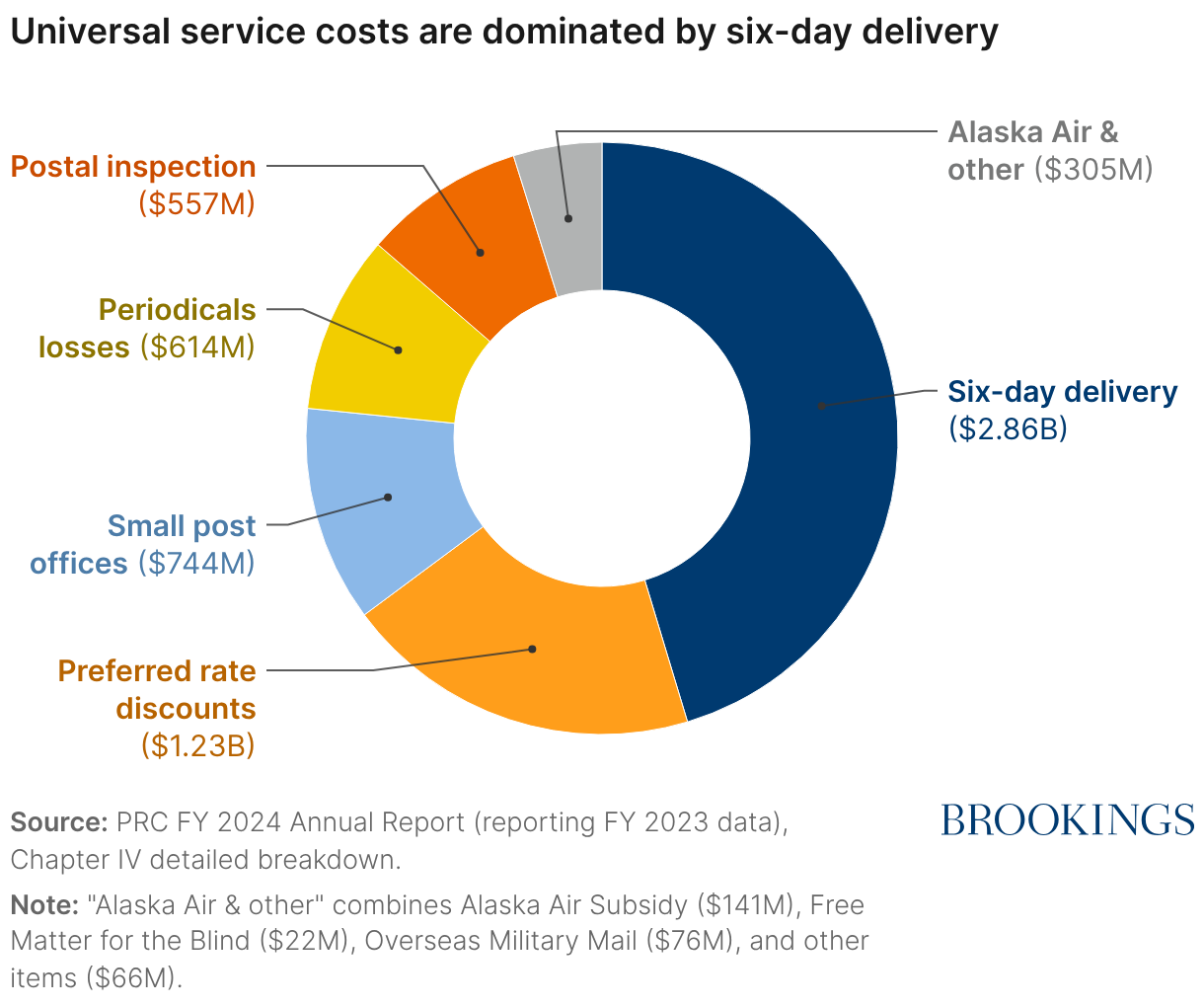

According to the PRC, total USO costs in 2023 were approximately $6.3 billion. These costs include six-day delivery (45%), preferred rate categories such as periodicals, maintaining small post offices in low-density areas, and other statutory service requirements.

Figure 10

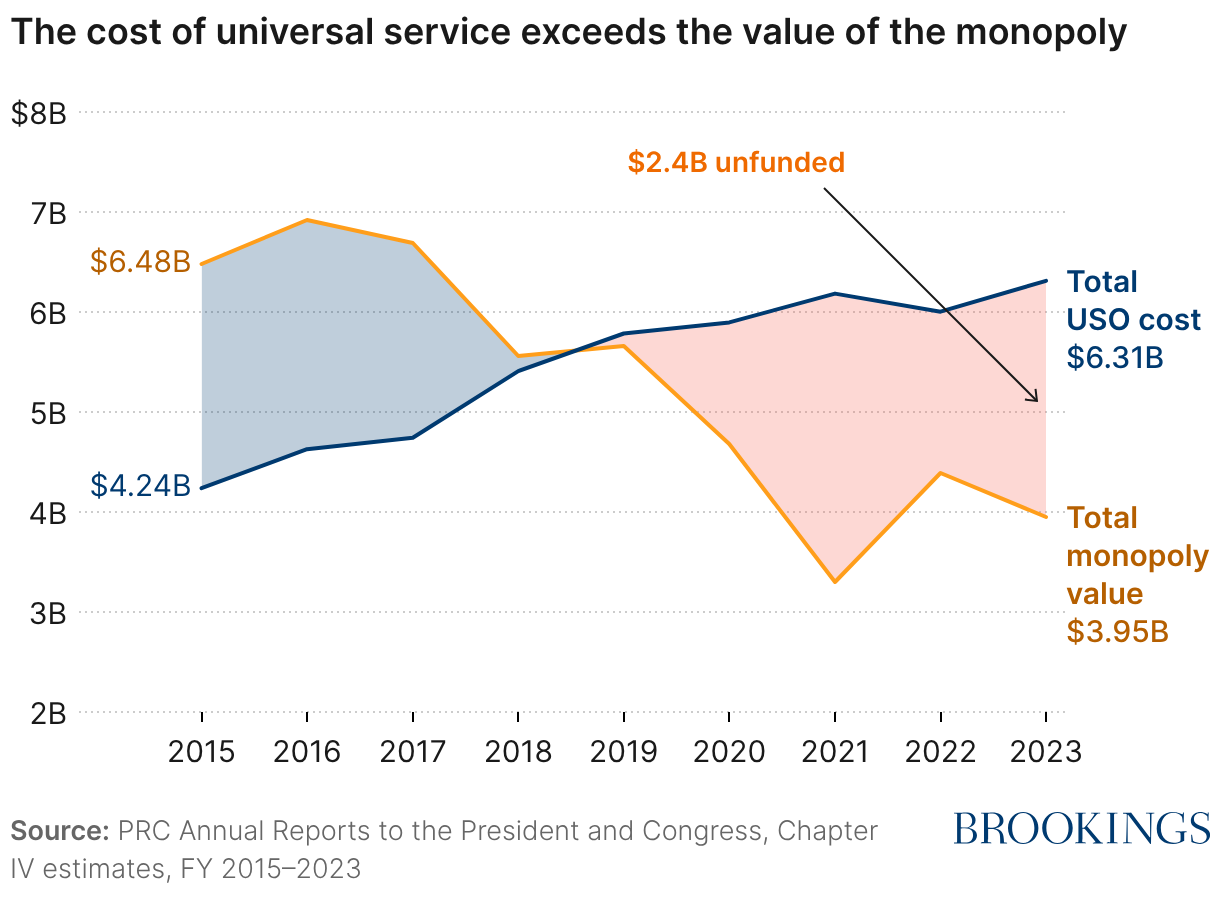

In the same year, the PRC estimated the value of the postal monopoly to be $4.0 billion (Figure 11). The difference—approximately $2.4 billion—represents the portion of the USO that is no longer covered by the monopoly-based financing mechanism. That gap must now be financed from the same operating revenue that also funds pension amortization and other legacy operations. In dollar terms, this shortfall represents an important element of the underlying structural mismatch.

Figure 11

Absent structural reform, this gap must be closed through higher prices, cost reductions, or additional borrowing. Yet price increases are restrained by regulation and competition, cost reductions are limited by statutory service requirements, and borrowing authority is capped. The resulting imbalance is not the product of a single year’s operating performance; it reflects a financing model that no longer fully aligns with the mandate Congress has imposed.

The central policy question is therefore not whether universal service has value. It’s whether the financing mechanism established decades ago is fit for purpose.

What Congress can change—and what operational adjustments cannot fix

The Postal Service’s fiscal position is shaped by statute. That means the most consequential reforms must also come from Congress.

Operational adjustments—consolidating facilities, optimizing transportation routes, modernizing the processing network to better accommodate parcels—can improve efficiency at the margin. They cannot, on their own, resolve a structural mismatch embedded in federal law.

Three categories of reform fall within Congressional authority:

- Pension financing and amortization structure. Pension amortization payments are determined by OPM under federal retirement statutes. USPS does not control the actuarial assumptions, discount rates, investment policy, or repayment schedules that determine these obligations. As a result, required payments can fluctuate materially from year to year and directly affect USPS’s reported margins.

Congress could restructure how pension liabilities are financed, including shifting these costs to the Treasury, as is done for other federal agencies. Any such reform would not eliminate the obligation, but it could change the timing, volatility, or revenue source earmarked to cover these expenses. For lawmakers, a key question is not whether the obligations exist—it’s how they are financed and who ultimately bears the risk when costs fluctuate.

- Explicit appropriations for universal service. The PRC estimates that the cost of the universal service obligation exceeded the value of the postal monopoly by roughly $2-$3 billion per year for the last several years. These services reflect a public good provided by the Postal Service. Congress could fund that mandate explicitly through annual appropriations.

Most countries maintain universal service by providing direct public funding to the designated universal service provider for these components. The United States does not. An explicit appropriation for the USO would align financing with the scope of the mandate rather than relying solely on cross-subsidy from declining letter volumes.

- Capital access and borrowing authority. USPS is in the process of implementing a multi-year modernization effort known as Delivering for America. This effort includes modernizing its vehicle fleet, processing operations, and facilities. These changes are intended to improve operational efficiency and reduce long-run costs.

However, USPS is undertaking this transition while operating under a now-binding $15 billion borrowing ceiling that has been in place since 1992. Congress could raise its borrowing cap or provide targeted capital funding for infrastructure.

Additional capital flexibility could ease short-term liquidity pressures and allow USPS to finance modernization over time rather than from current cash flows. It will not, by itself, resolve the structural gap between the cost of the USO and the declining value of the postal monopoly. But it could prevent a liquidity crisis from forcing abrupt service degradation before Congress acts.

What operational changes alone cannot resolve

It is tempting to view the fiscal challenge as a management problem or a uniquely American problem. It is neither.

Postal operators around the world are confronting the same structural shift: Digital communication has permanently reduced letter volumes, while the cost of maintaining nationwide delivery networks remains tied to geography. The tension between declining revenue and fixed universal service obligations is not specific to USPS—it is a defining feature of modern postal systems.

The United States has thus far required the Postal Service to preserve universal service without fundamentally revising how it is financed. Rate increases alone will not close the gap. Service reductions redistribute costs onto rural and low-density communities. Continued reliance on borrowing is constrained by statute. What remains is a policy choice.

Congress can realign the financing framework with the universal service mandate it has imposed. Or it can allow liquidity constraints to narrow that mandate by default. In practice, that “default” path would likely involve deferred payments, delayed investment, and increased pressure for service cuts that fall most heavily on the communities most reliant on the mail.

The central question is not whether universal service has value. It is whether Congress will finance that value explicitly in a digital economy where the old cross-subsidy no longer suffices. Today, the same shrinking revenue base is expected to fund both universal service and the federally governed retirement obligations—an arrangement that converts long-run structural imbalance into an immediate cash constraint.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).