As geopolitical tensions and energy price volatility continue to influence global markets, Asia’s stock indices have experienced mixed outcomes, with investor sentiment swaying in response to these developments. Amidst this uncertainty, identifying stocks that are estimated to be trading below their intrinsic value can offer potential opportunities for investors seeking resilience and growth. In the current market climate, a good stock might be characterized by strong fundamentals and the ability to withstand external pressures such as rising input costs or geopolitical disruptions.

|

Name |

Current Price |

Fair Value (Est) |

Discount (Est) |

|

STI (KOSDAQ:A039440) |

₩30750.00 |

₩61372.44 |

49.9% |

|

SILICON2 (KOSDAQ:A257720) |

₩38800.00 |

₩77230.39 |

49.8% |

|

Samyang Foods (KOSE:A003230) |

₩1183000.00 |

₩2353368.90 |

49.7% |

|

Sailvan Times (SZSE:301381) |

CN¥19.34 |

CN¥38.53 |

49.8% |

|

Maguro Group (SET:MAGURO) |

THB19.30 |

THB38.35 |

49.7% |

|

Livero (TSE:9245) |

¥2248.00 |

¥4462.03 |

49.6% |

|

JAC Recruitment (TSE:2124) |

¥863.00 |

¥1716.47 |

49.7% |

|

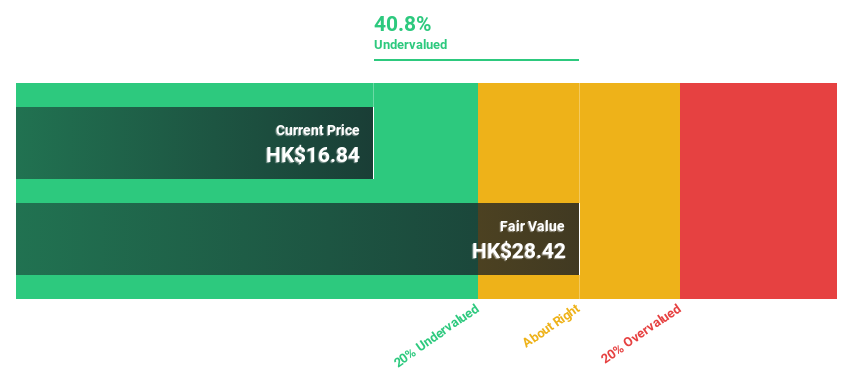

Guoquan Food (Shanghai) (SEHK:2517) |

HK$4.15 |

HK$8.30 |

50% |

|

EMRO (KOSDAQ:A058970) |

₩28600.00 |

₩56873.96 |

49.7% |

|

Caliway Biopharmaceuticals (TWSE:6919) |

NT$81.20 |

NT$162.33 |

50% |

Let’s explore several standout options from the results in the screener.

Overview: WuXi XDC Cayman Inc. is an investment holding company that functions as a contract research, development, and manufacturing organization with operations in China, North America, Europe, and internationally; it has a market cap of HK$74.10 billion.

Operations: The company’s revenue from its pharmaceuticals segment is CN¥5.94 billion.

Estimated Discount To Fair Value: 49.5%

WuXi XDC Cayman is trading at HK$58.9, significantly below its estimated future cash flow value of HK$116.55, indicating it may be undervalued based on cash flows. The company’s earnings are projected to grow 24.2% annually, surpassing the Hong Kong market’s average growth rate of 12.2%. Recent earnings show a net income increase to CNY 1,480.5 million from CNY 1,069.62 million year-over-year, supporting its robust financial health and growth potential in the bioconjugates sector.

Overview: Sinomine Resource Group Co., Ltd. focuses on the development and utilization of lithium battery new energy raw materials, rare light metals, and solid minerals both in China and internationally, with a market cap of approximately CN¥52.68 billion.