Matthew Ball’s 165-page slide deck was a bit relentless about giving sobering news for the game industry. Things might not be going as well as we thought, and some folks were mad at Ball for pointing it that gaming faces an attention war.

I talked to Ball about the reaction to his somewhat tough message and the hopes he has that gaming can evade some of the traps ahead in its future and move on to its rightful place in the entertainment pantheon.

To summarize Ball’s findings, he started out saying that global video game content sales had a strong 2025, with revenues hitting $195.6 billion, 5.3% above last year’s numbers per eight different market researchers including Ball’s own Epyllion firm. Mobile, PC and console numbers all grew and there were plenty of indie hits like Clair Obscur: Expedition 33, Blue Prince, and more. Many have noted gaming’s inexorable growth in most years, despite the multiple years of layoffs numbering in the tens of thousands.

But those numbers are perhaps an inch deep. When Ball examined the numbers more closely, he found that gaming now has some serious fragmentation in parts that are growing and shrinking, and that it also has deadly competition Ball in what Intel CEO Andy Grove once called the “war for eyeballs.” Ball calls it the “attention war,” where there is so much competition for our attention and only have 24 hours in a day.

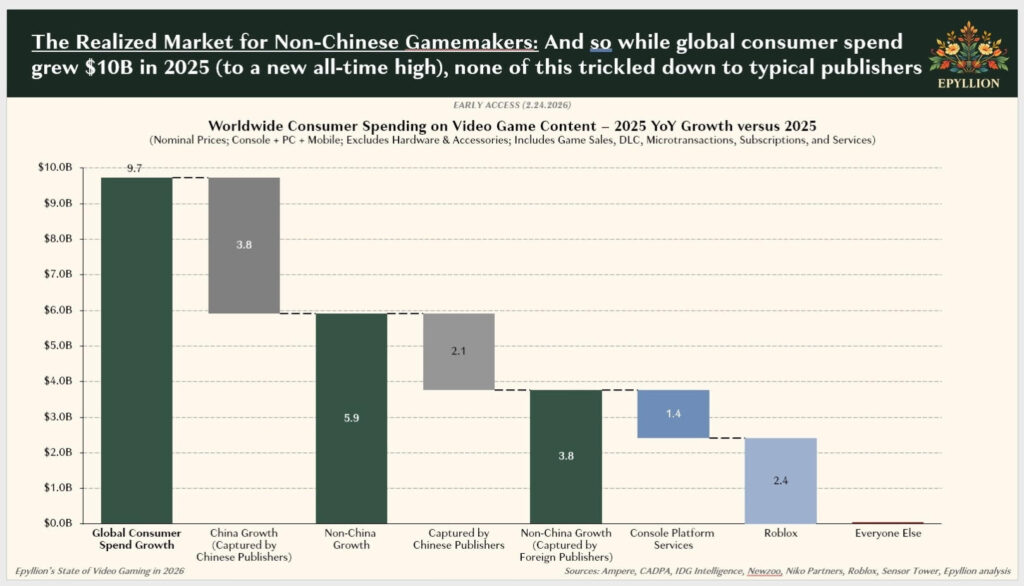

The growth of the “addiction markets” include fast growth for Only Fans, AI companions, online casinos, sports betting, prediction market wagering, YouTube, TikTok, and cryptocurrency and meme coins. Meanwhile, growth has stalled in gaming, with almost all of the 2025 growth coming from China’s growth, the share of the world market held by Chinese publishers, console platform fees and Roblox. If you back out all of those growth factors, the net growth for Western game publishers and developers is zero.

Profits are down, layoffs were still large and private investments in game companies fell 55% below 2024 numbers. Few new IPs are taking off in games, and even older stalwart IPs are weaker. Game makers canceled scores of titles in the works. The layoffs in 2025 amounted to 9,200, and 44,000 over four years. Hiring has resumed, with 13,000 new openings, but these jobs are concentrated in low-cost markets — not the U.S. A heavy dose of new content development is going to external development partners.

Ball said 2025 content investment as a share of net revenues hit a non-pandemic seven-year low. And among 34 game publishers, the average operating margins for companies outside China were far below pre-pandemic numbers. The margins fell since 2019 even though consumer spending surged 40% during the same time frame.

The battle for time

Time is the key slice of the report that I would like to focus on. It’s the reason why Netflix chairman Reed Hastings once said that his competitors included video games because they were competition for the time of his customers. And it turns out that Netflix has KPop Demon Hunters, with more than 540 million viewers — and gaming does not.

But it turns out that gamers can be as fickle as other consumers. The attention across gaming has focused mostly among older games. Six-plus year old games account for 72% of time spent in 2024 across the PC, PlayStation and Xbox, with one to five-year-old games accounting for 21% of time spent and new releases accounting only for 7%.

On Steam, new releases account for only 14% of time spent compared to older games. Mobile game spending is flat for the past five years as older hits get stronger and user-acquisition costs crowd out discovery of games.

Ball looked at eight countries — the U.S., Japan, South Korea, the United Kingdom, Germany, France, Canada, Italy and the rest of the world. He measured their share of global consumer spend on gaming content in 2019 and the years since and he concluded they are losing the “war for attention.”

Reports from Circana, ESA and Ampere suggest that the share of the U.S. population that plays games has fallen by 2.5 to four points since before the pandemic. There are similar declines in the rest of the countries. This loss of the attention of players means growth only comes rom greater monetization of remaining players; if players don’t spend more, all new investments must be borne by existing players; individual games can only grow by stealing other games’ players, playtime or spend.

Stealing time

Ball found that other industries that exploit interactivity, social play, progress loops and skill mastery are taking time from gaming in order to extract more money from consumers. The aforementioned addiction markets are what you might call “sin” industries, in contrast to the “fun, fulfilling and artistic” industry of gaming. Does it mean that sin is beating out fun? I noted before that I hope the war for attention doesn’t turn into a war for addiction. And they are all chasing the same people.

I quizzed Ball about these points and whether he sees bright sports. I foresee that gaming can win the culture war, even on platforms like YouTube, TikTok, and film and TV — where the conversation is increasingly about games. Fortunately, Balls sees those bright opportunities as well. You’ll see them below, and yet he believes that telling the tough news is what people need to hear so they can still do something about it.

And I also asked him about the averages bury the notion of opportunity, as there are always winners and losers every year in gaming. This year’s winner looks likely to be Grand Theft Auto VI. Will that be enough to lift gaming?

I really enjoyed this great conversation. Here’s an edited transcript of our interview.

GamesBeat: What was the reaction you got? Was there a pattern to it? Did anything strike you as a bigger reaction?

Matthew Ball: I would say there were three core pieces of feedback. Number one, surprise at how stagnant and/or declining many of the core western markets are. There was broad familiarity with a market or two, a general sense of course that revenue wasn’t growing as much as hoped, and there had been some pullback over the last two years. But so many different individuals, publishers, marketers, game devs focus on one or two or three markets. Sometimes that’s the U.S., U.K., and Germany. Other times it’s Japan and South Korea. Seeing it across all of these markets was a surprise, and definitely changed their perspective on what was happening in the market.

I didn’t know that I was going to write a report in 2026, or summarize 2025. Everyone assumed I would, but I hadn’t planned to do so until early in the fall. That was because I found this data that I reported on in the piece that was showing the declining player participation rates in the United States. Then you naturally say, is this survey bias? Is it reporting bias? Is it too noisy to rely on? Then I started taking a look at other markets. Circana, which does the best reporting in the United States, also runs in Canada. The same curve. I started looking at the U.K. and saw a similar trajectory. Videogames Europe and Sparkers run a similar survey across five or six or seven different markets. All of a sudden I started going deeper into this thesis. I started seeing a consistent trend of either stagnant engagement rates or declining participation rates.

That’s what led me to the second bit. As I produced this report, I was increasingly sure that there was clear evidence explaining the first part, the decline in revenue, and second, the declining participation rates, which is this growing substitution of time, energy, and dollars into newer, emergent quasi-interactive media. At the same time, I expected that there was going to be more pushback on that. Especially in some areas like online sports betting or iGaming. I expected to hear quite a bit of, “Yeah, we see it broadly. Everything is in competition. Restaurants, movies, going for a walk.” But that it wasn’t felt so acutely.

Instead I found a lot of people agreeing with this. Partly because they have sons or daughters, or their customer research teams are in the field, and they look at cohorts of 16-, 18-, 25-year-old men and women in high school or college who, a decade ago, one of their primary uses of spend would be video games. Now it was secondary or tertiary behind these other categories. So the second was that scenario, where I was surprised by the strength of the following.

The third has been–it’s best put within the context of all three reports. I wrote an essay at the start of 2024. I put out a presentation at the start of 2025. Then another at the start of this year. When you go back two or three years ago, there was this “survive until 2025” mentality, followed by “stick it out to 2026.” Those all suggested a temporal challenge, not a structural challenge. Part of what I was trying to write is that it is structural. It’s not longitudinal or temporal. In my conversations since the report came out, there’s very much an agreement there. That has led to much deeper conversations. No, it’s no it’s just about rethinking our slate, our portfolio. It’s not just critically examining our cost structure, our platform strategy. It’s a much more fundamental look at whether we’re in a new era of video gaming, one that faces different forms of competition, and not a new era defined by new technologies per se, or new devices. And if so, what do we have to do as a company?

GamesBeat: The thing I was predicting you would say there–I thought people were going to shoot the messenger and go into a state of denial.

Ball: I will say, I expected–this is really the second point I made to you. I expected there to be controversy that there wasn’t.

GamesBeat: The presentation brought home reality to a lot of people, I think. They may not like the news, but it’s persuasive.

Ball: Honestly, a very fundamental part of the presentation, I discovered it late. That was the pivot around–if the numbers seem so good, why doesn’t anyone feel it? As I shared with you on that slide, part of that was me refining that message even post-release. Trying to find clearer and clearer language, representations, data, and cuts to show that yes, there’s more money coming in the door than ever, but it’s not going to everyone. In fact, it’s not going to many.

That is, I think, one of the reasons why the report is perhaps less controversial than it might have been two to three years ago, prognosticating challenges to come. Now everyone very much feels it. Partly because–there’s this common refrain I hear from publishers and developers and game makers. Many of them are actually humble post-release. They understand when and how their game might have fallen short of what they hoped for. After testing with mass audiences, they have a different, more critical lens. But many of them still believe that it is common to have games that are better than they are popular. Everyone is trying to understand, what does it mean for the next game? What does it mean for the next dollar? What does it mean for a live ops plan that hopes to bring a great game to a great enough game?

GamesBeat: I’ve been watching The Studio, that show. I’ve been imagining, what if this were a video game executive, a video game publisher’s CEO that we were satirizing here, instead of a Hollywood guy? Some of the answers and denials and things like that would be interesting. I did wonder how much data you had to create or dig up. It seems like there’s just not enough data on the game industry. Even though there are lots of market research companies, finding that useful data, how did you go about that?

Ball: The industry is tough. It’s actually funny when you put it in contrast to many others. Isn’t it kind of stunning that all of the major movie exhibition chains and all the major movie studios report their daily box office globally, in most instances? We have an exact streaming count. Billboard will tell you how many times someone played a song every week and over the weekend. The data is scarce here. But most of this was actually very high-level allocations.

I’ll give you one example. We know that from 2021 to 2025, total console consumer spending on content, software, and services was up about a half-billion dollars. But over that same time PlayStation Plus spending grew by $1.2 billion. That’s actually not a very difficult portion of data to get. There’s general consensus across all the major research organizations as to how much money is spent on consoles per year. Sony reports PlayStation Network. This was less a question of how hard it is to get the data. It’s about framing the data the right way.

One of the primary challenges in the game industry right now is the separation between the headline figures and the distribution of them. When you take a look at Circana, for example, they do consistently report now, fortunately, that consumer spending is up one, two, three percent year over year in most months. But of course most of that tends to be in mobile. In PC and console it’s in platform subscriptions. As a result we know that the remnant is actually declining. That was less a question of how you find the data. It’s more about what’s the right question to ask with it. It was much more difficult, of course, to figure out the right data sets outside of gaming that have the appropriate applicability inside gaming.

GamesBeat: The contrast between 2025’s report and 2026 for you, what are some observations you’d have about that? How different is this report from the one a year earlier?

Ball: The 2025 report was 2024 historical. It ran through the year. What that was basically trying to say is that there is a fundamental challenge in the industry, which is it had a decade of outstanding growth because it was powered by many parallel, convergent, and often compounding new technologies, genres, and business models. The battle royale is the best instantiation of that. That was a new genre by and large. It brought about new monetization models, such as the battle pass. It took advantage of new platform capabilities in cross-play. Of course there were others. Mobile overall is one example. The advent of free-to-play in triple-A was another.

But basically, by 2021, most of those growth engines, as I called them, had exhausted. It was easy to say that this was all post-pandemic pullback, but I made the argument that there was something much more fundamental. Those growth engines are still relevant, but they’re not driving change. All the games that could shift to free-to-play, launch a battle royale and season pass model, had already done so.

The 2026 report is in many ways taking a look at the consequences of that. One way to look at the exhaustion of growth drivers is we’re no longer propelled by that which propelled us in the past. But no industry exists in isolation. If we say, and this tends to be the consensus, that games are not that much better today than they were five years ago, that’s in and of itself a challenge. But many other things are much better.

We can have social discussions around whether or not short-form video is good, whether iGaming, OnlyFans, online sports betting, crypto have a net positive or deleterious effect on society. But those are multiple categories that are much better than they were five years ago. We’ve been watching short-form video for decades, but clearly TikTok, reels, and shorts are a much better way to deliver it. Prediction markets have existed for decades, but it’s new that they’re this popular, that they’re covered by the New York Times, that global discourse is driven by them. Online sports betting has existed in some form for quite some time, lawfully and unlawfully, but it’s new that everyone in certain age brackets more or less does it. The fact that they do it means that it’s all much better.

This report is in some respects saying, “What are the consequences when one industry loses its technological, genre, and business model growth areas?” And substitutes do not.

GamesBeat: Look at the neighbors. I remember the time when I had some insight into taxes. It was in SimCity, when I realized, “Oh, I can raise taxes so I can spend on lots of cool things to build in my city,” and then the taxes got so high that the residents of my city were leaving for other places. The blind spot for me is that I don’t cover the addiction industries. I don’t cover OnlyFans or gambling. I didn’t realize that they were growing while gaming was barely growing or somewhat stagnant. They’ve discovered that the interactivity of gaming is something they can also provide.

Ball: Totally. I would mention one other thing that I think is important. There has been a lot of coverage, especially recently, with more and more games thriving at lower price points of $25, $40, $50, as well as coverage of rising console prices and how that may price out core gamers. It’s without question that economic duress, especially unemployment under 25, is constraining growth in the video game market. That’s without question.

At the same time, what I remind people of is that total disposable income is at or near all-time highs for most cohorts. Consumer spending is at or near all-time highs. Consumer recreational and leisure, entertainment spending is at or near all-time highs. The economy is relevant to the success of any form of discretionary spending. But consumers are not struggling to find new things to pay for. They’re actually not struggling to grow their spend in various leisure categories. It’s that they’re not doing so in video games. In many instances they’re cutting back to instead spend elsewhere.

To reduce this to a purely economic challenge would be to misrepresent that it’s not just about the economic constraints. It’s about the substitution with alternative forms of entertainment.

GamesBeat: Does this make you more discouraged this year, more pessimistic? Or do you find some way to be optimistic despite all this data?

Ball: I think any time there’s greater clarity on the challenges, that’s a reason for optimism. I mentioned earlier that two years ago–three years ago, when I wrote the first report, I was arguing that while there were acute challenges post-pandemic, such as the implementation of IDFA, the general weakness of game slates as a result of a shift to hybrid remote work, as well as supply shortages of consoles–my argument was that those were useful explanations, but they were insufficient excuses for gaming stagnation. Even after last year’s report, I still received a lot of–no, we just need to last another year. The category will rebound.

One core reason for optimism is that I think there’s a universal sense that there are enduring challenges that are structural. The gaming industry needs to re-prioritize, re-assign, and re-think its business models, its plans, and its cost structures in order to find growth, and in many instances seek growth abroad as well as just at home. That’s a reason for optimism. But beyond that, no. Look, I find a lot of it distressing. I’m definitely not someone who believes that the American, and in particular youth, and more so than that–I don’t know. The epidemic of young men spending considerable sums on various forms of gambling is bad. Plain and simple.

I would say that while I didn’t get into this in the report, the report in many ways understates the consequences of these other categories. There’s a brilliant report from MIT that has found that for every dollar that someone loses in online sports betting, there’s roughly $1.99 in net reduction in their wealth. Why? Because they couldn’t afford to lose that dollar. As a result they go into credit card overdraft fees. They have more credit card debt. They have compensatory gambling. They drink more. We see this cataclysmic effect. There was another study showing that within 14 quarters or so, there’s a roughly 40%–not 40 points, but 40% decrease in credit scores. The consequences of these various forms of gambling-based vices really cascades economically.

GamesBeat: There were a few areas where I wanted to challenge the report and see what you had to say. I’ve heard from other folks that when GTA comes out, this is all going to change. The picture is going to look so much brighter. The industry will grow, whatever, 20% because of one game. Does that seem like a realistic hope?

Ball: I think there will be long-term positive impacts from GTA. The console hardware growth is obviously going to be more constrained as a result of DRAM-led price increases. It’s definitely going to be a re-onboarding opportunity for many lapsed gamers. It’s going to bring a lot more attention to the category. That’s all positive. That’s all true.

At the same time, the question is not, “Are some companies doing extraordinarily well in the game industry?” The question is, “How is the median game company doing? How are most game publishers doing?” As I report on, the industry has grown in its top line about 40% since pre-pandemic, but we’ve nevertheless seen total profits are well down. If GTA comes to market and single-handedly grows console by $2-3 billion, but those proceeds all go to Take-Two, that’s just a different version of this year’s report. Yes, the industry added $10 billion and hit an all-time high, but all of that money went to three destinations: the Chinese publisher ecosystem, the console platform services, and Roblox. A year where there’s a fourth category, Take-Two, is better than one with three categories, but it doesn’t change the overall picture. Even if it raises the tide more broadly, if the answer is that in 2027 there was some $400 million split across the entire ecosystem as a fifth bucket, that’s not much better either.

GamesBeat: Part of my response might be, if you’re thinking about entering the industry, making a game, making it your career, you shouldn’t be discouraged by averages. It’s always been an industry of winners and losers. If you have a winning idea, a winning game, you don’t have to worry about averages. In that sense there’s always a reason to find optimism for staying in the industry.

Ball: I would say three things that are important. One, these are aggregate figures, but no one ships games in aggregate. Two, no individual game maker, title, publisher, or creative lead is aided or harmed by plus two or minus two percent growth. It’s just not that relevant for that individual. Three, and this is the most important thing, as much as we can talk about whether or not two or three or four or five percent annual growth would be better than zero or negative one or one, a more important measure to me is whether or not we see one, or ideally all, of the following four things: new studios breaking out, new franchises breaking out, old studios achieving altogether new highs, and old franchises doing the same.

In 2023, in 2024, and in 2025 the market was hard, but each of those four things happened, and they happened repeatedly. The overall figure is primarily driven by a dozen or so major game releases and a handful of major publishers. It is more important to me, and a better measure of health, what happens to the rest. I totally agree with you.

GamesBeat: I’ll try to ask this question succinctly, because it gets to the heart of where I’m hopeful. I think of gaming’s chance to win the culture war–if you become mass culture better than anyone else does, then you win. You don’t have to conquer everyone else because you have the attention, as you framed it. If gaming is counterattacking into some of these areas with transmedia–you look at EA and its larger sports strategy that you wrote about it, or the inroads that games have made into movies. The new Super Mario movie launched yesterday. Games have a presence on things like TikTok and YouTube and Twitch. You see gaming making gains in these areas. Plus, with Roblox, gaming has this chance to catch people at the youngest ages. The addiction industries, by contrast–unless there are prediction markets inside Roblox, that should be the thing that cements gaming as a habit in the next generation. People grow up increasingly immersed in a gaming culture, and that becomes mass culture. As long as that’s the case, to me, gaming can’t lose. What’s your reaction to that argument?

Ball: I agree. I think the challenge is that it still sits a little bit in isolation. When we take a look at some of these other categories–online sports betting is the best example. That’s seen massive cultural ascendance as well. There’s now a major sports book branded under the ESPN brand. Sports betting is integrated into the live sports broadcasts. You can’t escape it. We talk about video games being ubiquitous on TikTok, but it’s not literally forced into every experience. Of course many sportscasters talk about betting odds while covering the nation’s most popular content, like the NFL. When you open up the New York Times, conversation around boots on the ground in Iran is partly predicated on what prediction markets say, what the experts are betting on in comparison to that.

I agree with you that we’re seeing a massive cultural ascendance for gaming. That’s clear. The Last of Us, Super Mario, Minecraft, these are among the most significant cultural moments of the last few years. At the same time, those other categories are still growing. The top OnlyFans star, the literal highest-grossing OnlyFans star, is a frequent appearance on the top youth YouTuber channels. It’s mind-boggling. It would be inconceivable 15 years ago that a major porn star would be in children’s and youth YouTube videos as a form of customer acquisition and brand-building. But that’s the nature of social media today.

I agree with you. I think we just see it in those other categories as well.

GamesBeat: When I thought about why gaming has gotten to where it is, it feels like gaming has always offered the best value. If you look at it from that perspective, I wonder if that value is perceived as increasing now or decreasing. I suppose that’s partly dependent on what kind of monetization model you’re using. But where do you see that? If we haven’t raised prices in a long time and inflation has happened, does that mean the value you’re getting from games has increased?

Ball: Without question. A harder to pinpoint reality of the game industry right now is that–part of the reason why profits have gone down and it’s hard to push up pricing is that it’s an incredibly competitive marketplace. In economic terms you would say that it’s so hypercompetitive that consumer surplus has grown and producer surplus has inevitably gone down. In many ways that’s a reflection of the indie and single-A boom. The fact that there are so many studios spending single-digit millions or low double-digit millions with teams of a few people or a few dozen people – supported of course by outsourcing – who now compete with and often outperform megalith studios is a reflection of that.

In effect, you would say that yes, by nearly every measure gaming has become a higher-value category. But that’s of course difficult for the average video game publisher.

GamesBeat: I think back to some earlier reports you’ve done, but also a lot of reporting I’ve done over time. There’s a resistance to technological changes that have happened when they come along in gaming. The players themselves have resisted the metaverse. They resisted blockchain. Now it looks like they’re resisting AI. People are trying to come up with technological advances for the industry to get it out of these problems, but players don’t accept them. This may turn into a disadvantage for gaming if it’s not the first, like it has been in the past, to adopt new technologies.

Ball: There is certainly a consensus opinion that video gaming has become ground zero for gen AI controversy. It’s a challenge with employees far more so than in most creative organizations, because most publishers employ all their creative teams. In Hollywood most of them are contractors. They’re outsourced. They’re not actually working hand in hand. On top of that, consumers are also struggling with the acceptance of gen AI content far more. Every week or two there’s another gen AI song that hits the Billboard Hot 100. We see YouTube is constantly dominated by gen AI content. Of course most of the major social video platforms are as well. We see on Twitter the extent to which it’s reaching. That, plus the strained economics, where the video game industry is under more financial pressure than any other industry, and therefore is in deep need of new cost savings–it’s built up all these tensions to a much greater degree.

That’s one thing, this ground zero challenge. At the same time, we should note that there are many parts of the world that are quickly adopting, or not taking the same issue–across much of Asia generative AI has been deployed en masse into video games with very little issue. Because of the different employee cultures there’s less of an internal issue as well. In mobile it’s far more widely deployed, in part for UA advertising. For the most part – not entirely – it is more concentrated among the major western markets and in PC/console content. Is that a constraint? Yes, but on the other hand, it’s up to the industry to articulate the benefits, to prove it in products, and to make sure that the results of the implementation are widely shared. If consumers benefit and employees benefit, the industry does as well. That’s one of those areas which–whether it was in blockchain and related technologies or VR, that’s rarely been front and center in communications.