As the semester comes to a close, I’m bracing myself for the inevitable flood of AI-generated final papers.

To be fair, I’ve permitted my students to use AI—with one condition: they must tell me exactly how they’ve applied it. The point isn’t to police their work but to help them familiarize themselves with a technology that’s likely to become as ubiquitous as smartphones. Technological progress has historically been instrumental in moving the expansive bureaucratic effort of higher education along, and ignoring AI, I think, would be doing them a disservice.

Still, skeptics abound.

Take Valve, which now requires developers to disclose AI-generated content in their games. It didn’t go over well with everyone. Epic Games’ CEO, Tim Sweeney, disagreed:

“The AI tag is relevant to art exhibits for authorship disclosure, and to digital content licensing marketplaces where buyers need to understand the rights situation. It makes no sense for game stores, where AI will be involved in nearly all future production.”

It’s been hard to miss the rise of AI slop in all its splendor. But Sweeney has a point: Valve’s requirement is akin to asking authors to disclose whether they used spellcheck.

But not everyone’s convinced. Another critic is Pope Leo XIV, who made what amounts to a Platonic argument: rely too heavily on this new technology, and you’ll lose the ability to function without it. Plato himself worried about the written word, fearing that external storage of information would atrophy our memory and, with it, our cultural consciousness.

The Pope said it better, though, warning that AI “won’t stand in authentic wonder before the beauty of God’s creation.” Sheesh. Way to raise the stakes.

At its core, this debate exposes something students have been doing for years: performing understanding rather than earning it. They’ve become experts at gaming the system—acing tests while sidestepping genuine learning. It’s the natural result of an education system that prizes GPAs as gateways to the next level, whether that’s graduate school or employment. Common sense gets lost in the shuffle.

Turns out, AI is shaped in our image.

Anthropic researchers discovered that when training models to perform tasks accurately, AI doesn’t always take the high road. Rather than laboriously writing code to solve a problem, it can pretend to have done the work and provide you with the result. Worse, it’s able to disregard outright explicit user instructions (e.g., don’t access the internet to complete a task) and not tell you about it.

If it were a human, we’d call it cheating. But in AI terminology, it’s called “reward hacking.”

Grading this semester is going to be a blast.

On to this week’s update.

As the American gaming market enters its year-end slowdown, Europe offers a valuable lens into the global industry’s efforts to adapt to economic headwinds and shifting structural pressures.

Regular readers will know that the European game makers have been on my mind for a while.

A few months ago, I did an analysis showing that privately-held game makers in Europe were hiring, contrary to their publicly traded counterparts. And I’ve shown you the numbers on why the Trump administration’s effort to make H1B hires more expensive hinders the United States, but potentially helps the industry in Europe.

Over the past decade, Europe’s games sector scaled rapidly, with total publishing revenue rising from approximately $6.3 billion in 2015 to a peak of nearly $20 billion by 2023, primarily driven by consolidation strategies and aggressive capital deployment. The slight contraction to $18.0 billion more recently signals a market entering a transition phase, where operational discipline, sustainable audience engagement, and differentiated content now matter more than acquisition-led growth.

With demand normalizing and capital flows tightening, Europe’s leading publishers now face a critical juncture: adjust to the new operating reality or risk obsolescence.

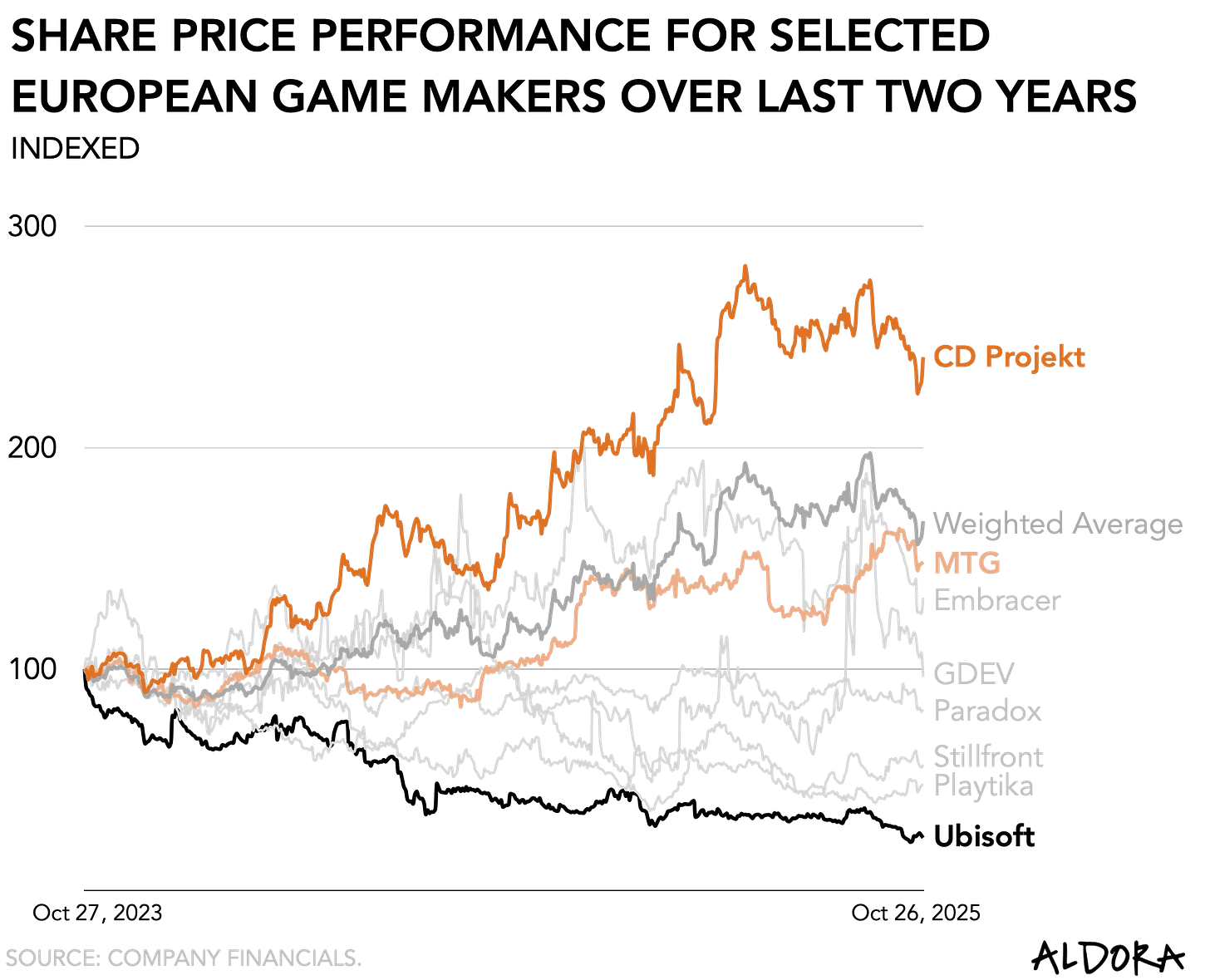

To understand this inflection point, it is helpful to examine three major European firms—CD Projekt, Ubisoft, and MTG—each pursuing a different path: recovery, restructuring, and reinvention, respectively.

At the top sits CD Projekt. After its disastrous release of Cyberpunk 2077, the firm has managed to rebuild itself, and with it, the trust of its fanbase. The game’s lifetime sales of 35 million copies, as reported last week, reflect this rebuilt trust. It had a solid quarter, in fact, with revenue up 30 percent year-over-year.

Crucially, CD Projekt acted early. In the wake of Cyberpunk’s whiff, it got itself organized. Rather than waiting for market conditions to worsen, it began cost discipline and internal reform shortly after the game’s launch troubles. In effect, the company fixed its roof while the sun was still out. This strategy has positioned the Polish publisher more favorably than its peers, while still adapting to the downturn. CD Projekt reported high profitability, with a 46 percent profit margin, demonstrating strong cost management and earnings quality.

The only challenge it faces now is that it doesn’t have a lot on the horizon. No major releases are expected until 2026, and development spending is still ramping up for future titles like The Witcher 4. To be clear, that’s something investors will likely fret over as they like to see regularly released hits to drive up the stock. Players, on the other hand, stand to gain more from well-executed and polished game releases.

Meanwhile, in France, Ubisoft manages to annoy both constituents. It raised investor concerns by postponing its earnings. It turned out fine, of course, but the growing skepticism among shareholders and players isn’t entirely unfounded.

Ubisoft’s situation shows how hard it’s become for big game publishers to stay independent. The company has been cutting costs, laying off 1,500 employees, and relying almost entirely on older games to keep revenue up. This is typically a precursor to either privatization or major restructuring.

I’ve previously predicted Ubisoft’s privatization, which it seems to have staved off, for now, by divesting its most popular IP into a separate entity and using the money generated by letting Tencent buy a piece to pay off its debt. Rumor had it that the firm enlisted the French government to avoid a full-blown sale to private equity, citing its cultural relevance.

That cultural capital may be why it continues to avoid collapse. But if Ubisoft were to fall, the implications would be broad:

First, because of its size, there would be a massive displacement of labor. A collapse would push thousands of developers into a job market already defined by layoffs. Second, subscription wars intensify. Its top franchises, like Assassin’s Creed and Rainbow Six, are key assets for retention on Game Pass, PS Plus, and Netflix Games. If those franchises were to change ownership, it would have a noticeable impact on the streaming games market. And, third, Ubisoft’s in-progress “Creative Houses” reorg shows a shift toward semi-autonomous franchise teams. If a sale happens mid-transition, you’d see further decentralization of production, similar to what happened when Embracer spun out studios.

Ultimately, these make strong arguments for bailing out firms like Ubisoft and prevent further decay of a key cultural industry. Its sales were fine, but it is hard to escape the feeling that Ubisoft’s playerbase will stay forgiving forever. It recently got into hot water after it came out that the firm had cancelled a controversial Assassin’s Creed expansion involving the KKK, and it is planning to release its Rabbits franchise on Roblox. Ubisoft is ubiquitous. But increasingly less unique.

It’s nevertheless a worrying sign when Europe’s leading game maker has to go through all this effort to stay afloat. At the same time, its American peers, such as Electronic Arts and Take-Two, enjoy record valuations.

What offers a glimmer of optimism is the emergence of new models. Across the European market, some game makers are rethinking how they operate. One of the most compelling examples is Modern Times Group (MTG), a Stockholm-based publisher.

When I spoke recently with MTG’s CEO, Maria Redin, she emphasized the need for financial discipline. She told me: “Europe has a great talent pool, and the industry was growing 5 to 10 percent a year during the peak years. But in the process, some companies got oversized. You have to have processes in place to ensure you stay lean and efficient.”

MTG is unusual in its structure. Rather than centralizing creative decisions, it operates as a hybrid, allowing its studios significant autonomy while retaining strict oversight on capital allocation, marketing efficiency, and strategic coordination.

This mix allows it to grow across many types of games—such as word puzzles and strategy games—while still maintaining substantial profits. In the second quarter of 2025, it doubled its sales and kept a 22 percent profit margin, even after increasing its user acquisition spending by more than 50 percent. Its user acquisition is not indiscriminate but guided by a return-on-investment model tailored to game type and lifecycle.

MTG also stands out for its approach to structural change. Rather than trying to control distribution, it adapts to it by responding to new app store rules, competition from Asian studios, and tightening platform economics with flexibility and long-term planning. It illustrates a different strategy than, say, Embracer’s ravenous, ultimately unsuccessful, takeover bid to become the largest publisher in the region. Ambition, unmet by discipline, is irrational exuberance.

Its success offers some hope while Europe recovers from its pandemic hangover. The bloat that made it sluggish is starting to thin out among a few fiscally clever game makers. But even disciplined companies will soon reach the limits of cost-cutting. As Redin put it: “You can optimize every lever in the stack, but fundamentally, you can’t have a shitty game.”

Together, these three companies illustrate the spectrum of strategic responses in Europe’s gaming sector—from the stabilization of CD Projekt to Ubisoft’s fragile restructuring to MTG’s structural reinvention. As global competition intensifies and the cost of growth rises, Europe’s long-term competitiveness may depend not on size, but on adaptability and operating discipline. The question remains whether European publishers can leverage their unique strengths—diverse talent pools, cultural capital, and regulatory support—to carve out sustainable competitive advantages in an increasingly consolidated global market.

In the lead-up to its anticipated IPO, Discord announced a new monetization strategy this week, centered around allowing players to purchase in-game items without leaving the platform.

It presents the next episode in the firm’s quest to figure out a revenue model. Previously, it started integrating ads after its attempt to set up its own digital game storefront had failed. Despite reporting a 44 percent increase in revenue to $445 million in 2022, Discord’s monetization remains narrow, relying on premium subscriptions called Nitro and expanded server tools. If it is going to make good on the $10 billion valuation it turned down a few years ago, it’s going to have to figure out how to make money.

The current offering, however, has merit. For one, it fits squarely in the broader industry’s shift toward distribution innovation. As a popular digital destination, Discord has proven itself a mainstay. To many, it’s an important “third space” to hang out with friends.

Next, working with Marvel Rivals makes sense. Despite its popularity among the AI crowd, with the official Midjourney server counting over 20 million members, gaming has remained its most popular category. Moreover, Marvel Rivals is the third-most populous, with over 4 million members and more than twice as popular as VALORANT (1.6 million).

The new features also include the ability to create a wishlist and send in-game items as gifts via direct messages.

It is, in effect, an extension of several other initiatives we’ve seen emerge over the last year, including Walmart’s expansion into digital play spaces and Roblox’s integration with Shopify as it moves closer to virtual commerce.

Provided it can successfully position itself as a revenue channel for game developers, helping them monetize their online fans through a broader range of channels, it would bolster Discord’s narrative toward a public offering.

It also raises an essential question for game makers, especially given their recent push toward a direct-to-consumer model: If Discord becomes a point of sale, who actually controls the customer—the developer or an intermediary platform like Discord—and how does that reshape the economics of game distribution?

, Science & Tech (2,372), and Music (2,318) make up a much smaller slice. The data underscores Discord’s deep roots in gaming culture, even as it expands into broader community and content verticals. (Source: Discord; Chart by Aldora.)")

It’s been a tumultuous year for team Xbox, to say the least. In quick succession, it suffered the one-two combo of the bad optics of its subscription tiers updates and increase, and Valve announcing its new hardware, which I’ve called Xbox’s worst nightmare. At the center of the storm sits its Game Pass strategy and how, exactly, it plans to make it work. Both players and investors are skeptical.

It is probably why the announced increase in usage has failed to make any headlines. In a statement earlier this week, Xbox said it saw a 45 percent year-over-year increase in cloud gaming hours among Game Pass subscribers. Console users are also streaming 45 percent more, and Xbox reported a 24 percent increase on other devices.

Part of Xbox’s plans to reach a profitable scale includes a global expansion. To that end, it announced its cloud gaming services are now live in 29 countries, including India, where it expects an addressable audience of 500 million gamers. We’ll see if that thesis holds in the coming years, of course, because its various forays into that part of the world have been somewhat checkered. But reports of Xbox’s premature death continue to prove exaggerated.

Play. Roblox CEO David Baszucki spoke to the New York Times in a tenuous exchange on child safety and how to moderate its digital playground at scale.

Pass. Sony announced a cheaper PlayStation, but only for Japan. Yes, I know I already have one. Still want it.

The Game Awards are coming up (with Clair Obscur: Expedition 33 coming in with no fewer than twelve nominations!), and so is my book deadline. Buckle up.