Reports of the week:

-

AppMagic: Top Mobile Games by Revenue and Downloads in November 2025

-

Games & Numbers (November 1 – December 5, 2025)

-

AppMagic: Mobile Games Monetization Report – 2025

AppMagic reports revenue after store fees and taxes. Revenue from Android stores in China is not included.

-

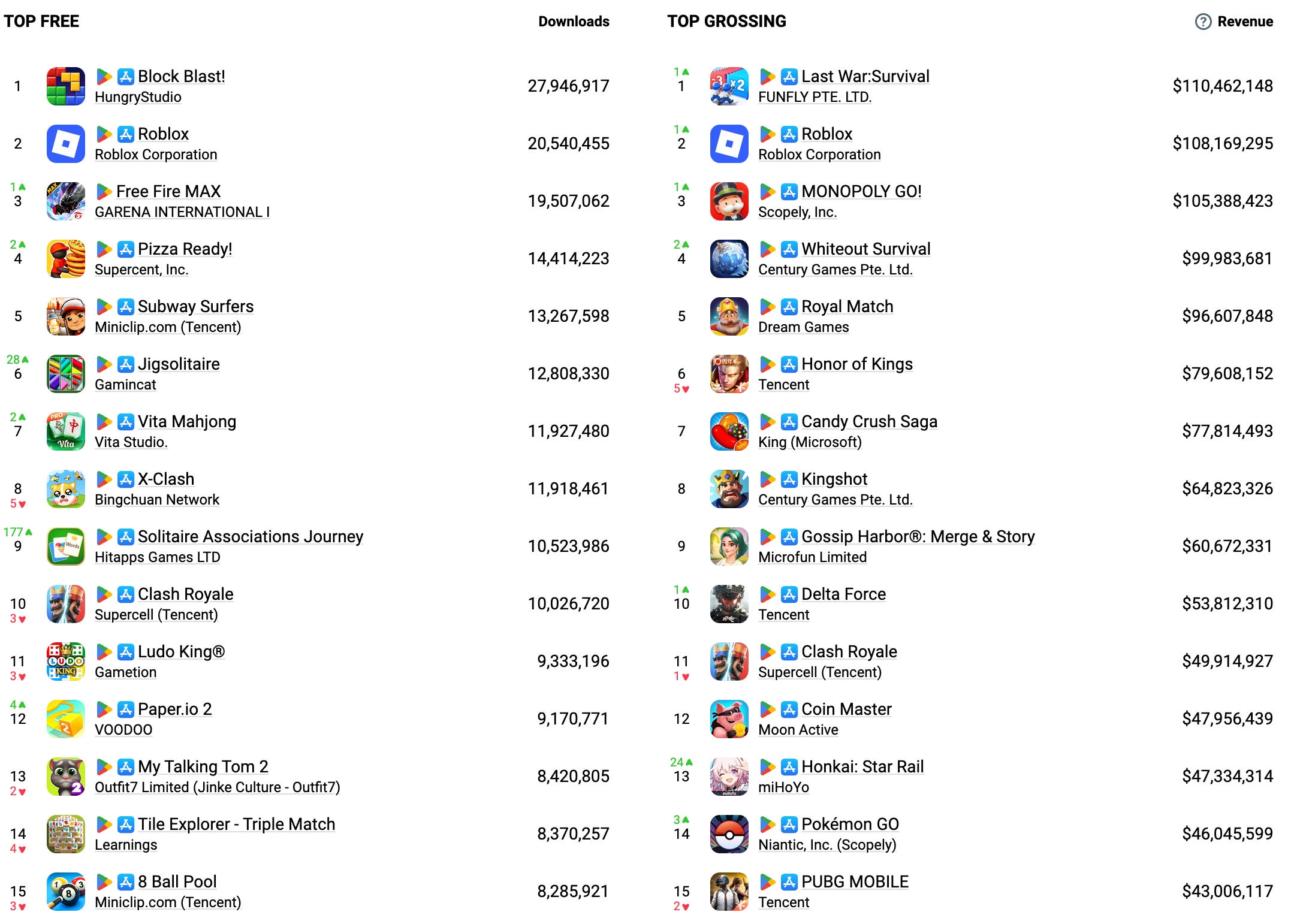

Last War: Survival led the November revenue chart with $110.4 million. Roblox followed with $108.1 million, and Monopoly GO! ranked third with $105.3 million.

-

Honor of Kings saw a significant revenue drop. The game earned $79.6 million in November, a level last seen in September 2019. It will be interesting to see how the development team responds to such a sudden decline.

-

Delta Force continues slowly approaching the global top 10 by revenue. The game generated $53.8 million in November, with 96% of all earnings coming from China.

-

Honkai: Star Rail had an excellent month, earning $47.3 million in November, which is 2.5 times higher than in October. Thanks to this spike, the game climbed to 13th place on the chart.

-

Block Blast! (27.9 million installs), Roblox (20.5 million) and Garena Free Fire Max (19.5 million) were the three most-downloaded games of November.

-

Two new titles entered the top 10: Jigsolitaire with 12.8 million installs (sixth place) and Solitaire Associations Journey with 10.5 million installs (ninth place). Both titles are non-traditional solitaire-style games. Solitaire Associations Journey also earned more than $1.5 million last month.

-

X-Clash, a 4X game that presents itself in all marketing materials as a Save the Dog-style title, reached 11.9 million downloads in November. It remains in the top 10 by downloads and generated $3.6 million in November, nearly triple its October revenue.

Manage thousands of SKUs easily with Xsolla’s Catalog Management – import via JSON or API, apply bulk edits and filters, and set intelligent regional prices and restrictions that match local purchasing power. This flexible pricing boosts sales by up to 13%, ensures consistency across platforms like App Store and Google Play, and cuts your operational costs by up to 50%, maximizing your global revenue.

Make your webshop efficient – with Xsolla!

Mobile Games

Platforms

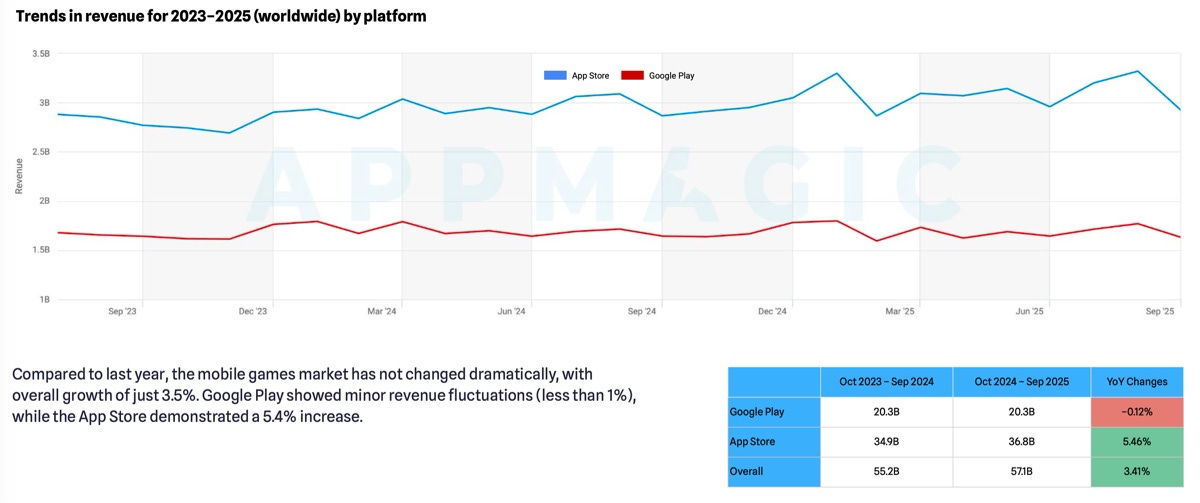

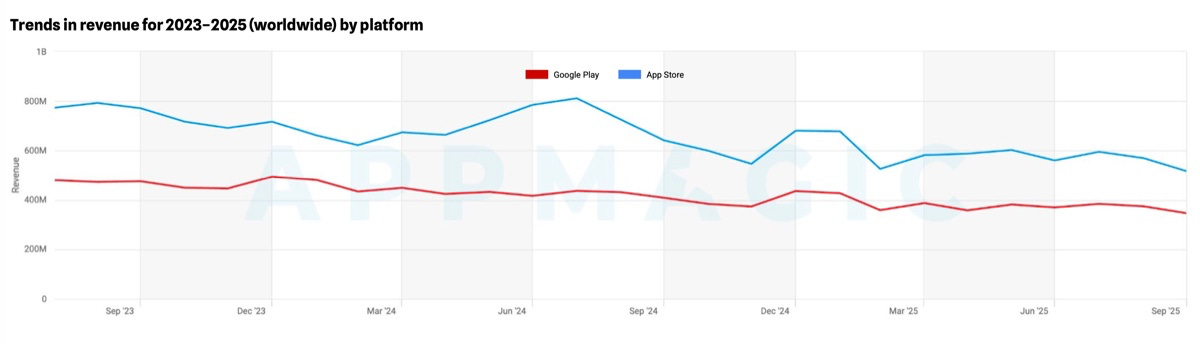

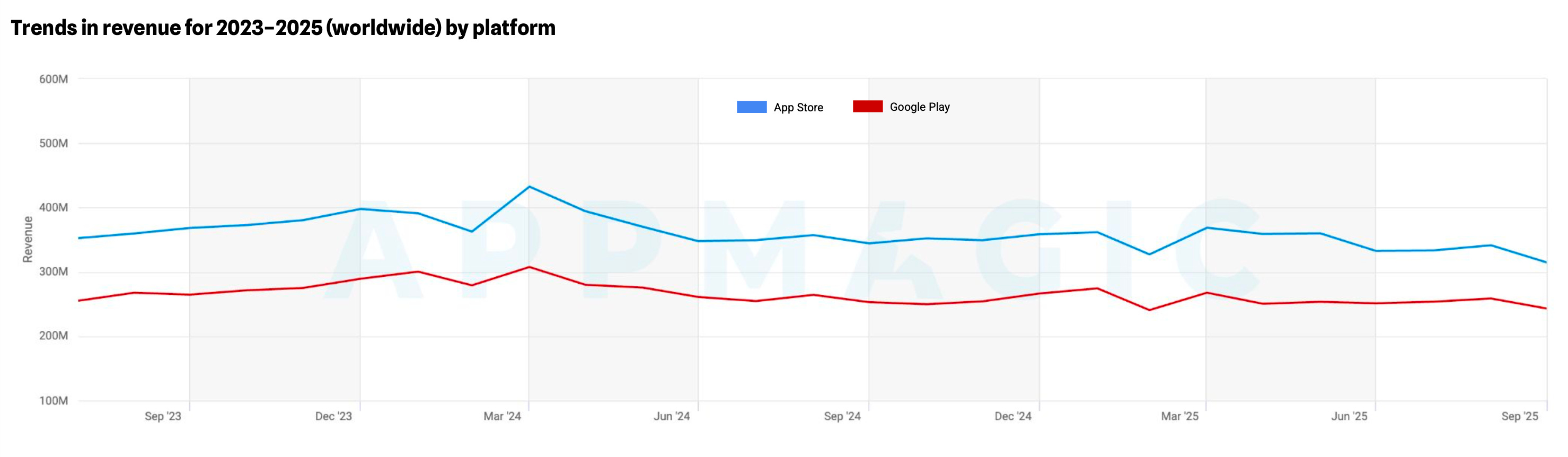

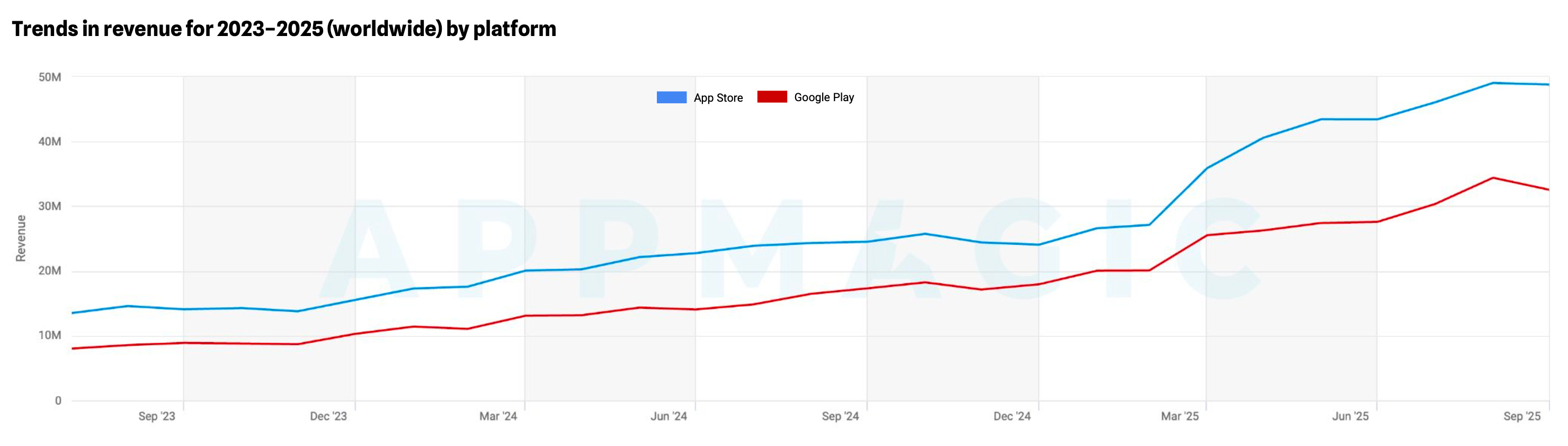

The report is based on AppMagic data for the period 2023–2025 (through October 22, 2025). Numbers cover App Store and Google Play worldwide. Sections on D2C focus only on the United States, and the paying user behavior section covers only the top 10 grossing titles in the US.

-

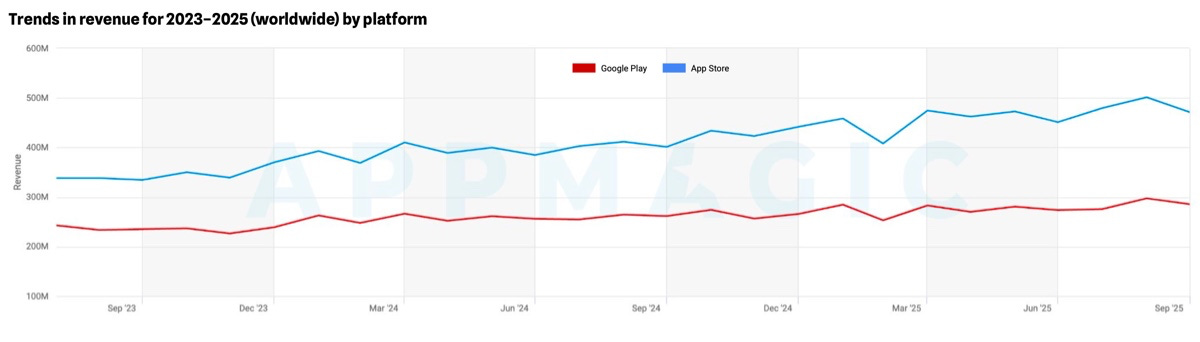

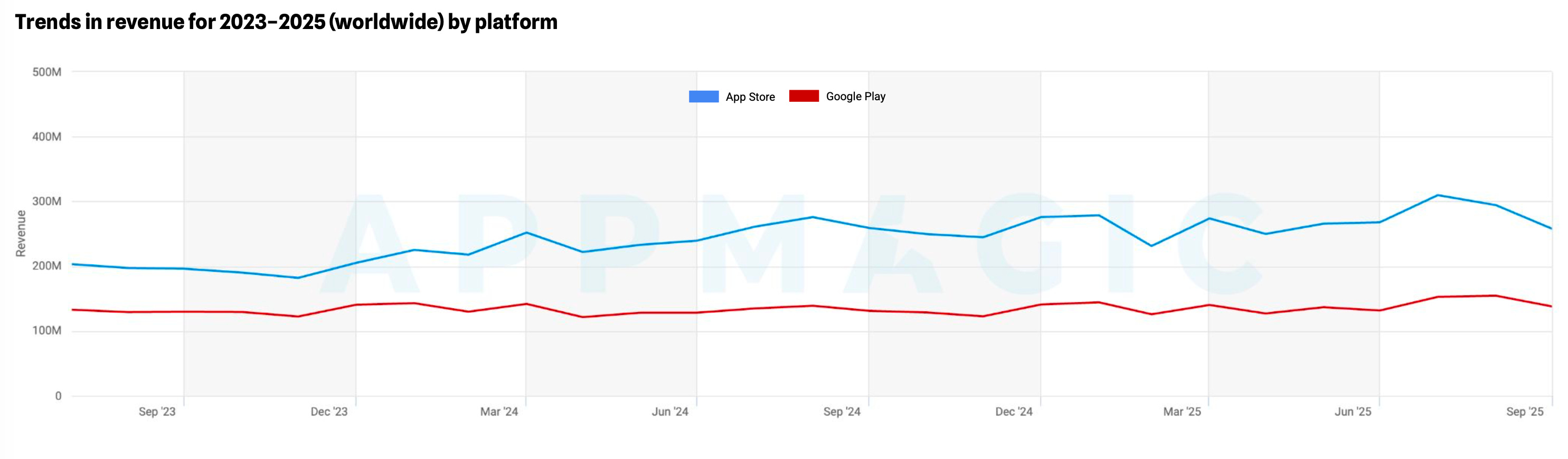

The overall mobile games market grew moderately from $55.2 billion to $57.1 billion, up 3.4% year over year. App Store game revenue increased 5.4%, while Google Play revenue declined 0.12% year over year.

-

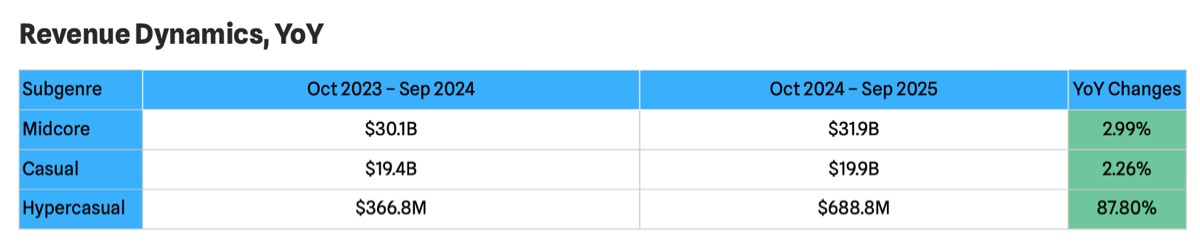

Revenue for midcore titles grew 3% year over year, casual games grew 2.3%, and hypercasual (and apparently hybridcasual) projects showed 88% year-over-year growth, although this is from a low base.

-

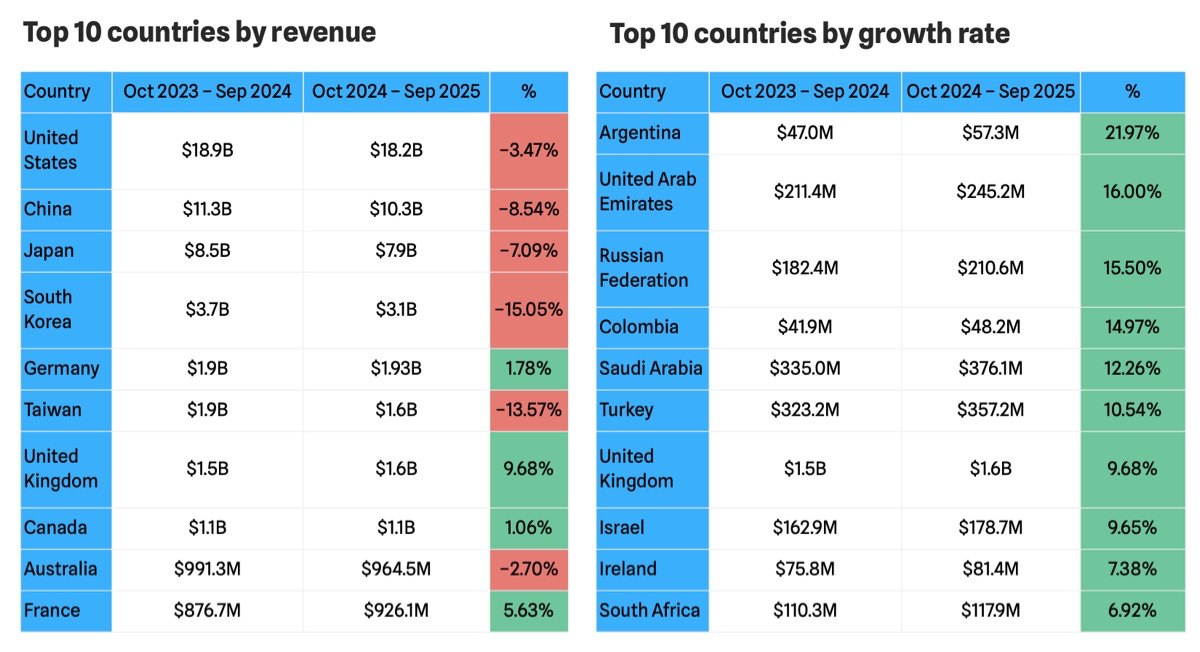

The top 10 countries by revenue barely changed: the United States, China, Japan, South Korea, Germany, Taiwan, the United Kingdom, Canada, Australia, and France. However, the dynamics differ. Only the United Kingdom (+9.68% YoY), France (+5.63% YoY), Germany (+1.78% YoY), and Canada (+1.06% YoY) grew.

-

Among the steepest revenue declines in percentage terms are South Korea (-15.05% YoY), Taiwan (-13.57% YoY), and China (iOS only, -8.54% YoY).

-

The fastest growth is coming from markets with a low starting base and/or volatile currency: Argentina (+22% YoY), UAE (+16% YoY), and Russia (+15.5% YoY).

-

AppMagic notes that by the end of 2025, most large Asian markets saw revenue decline, while European markets grew. Overall, growth is now concentrated mainly in emerging markets.

-

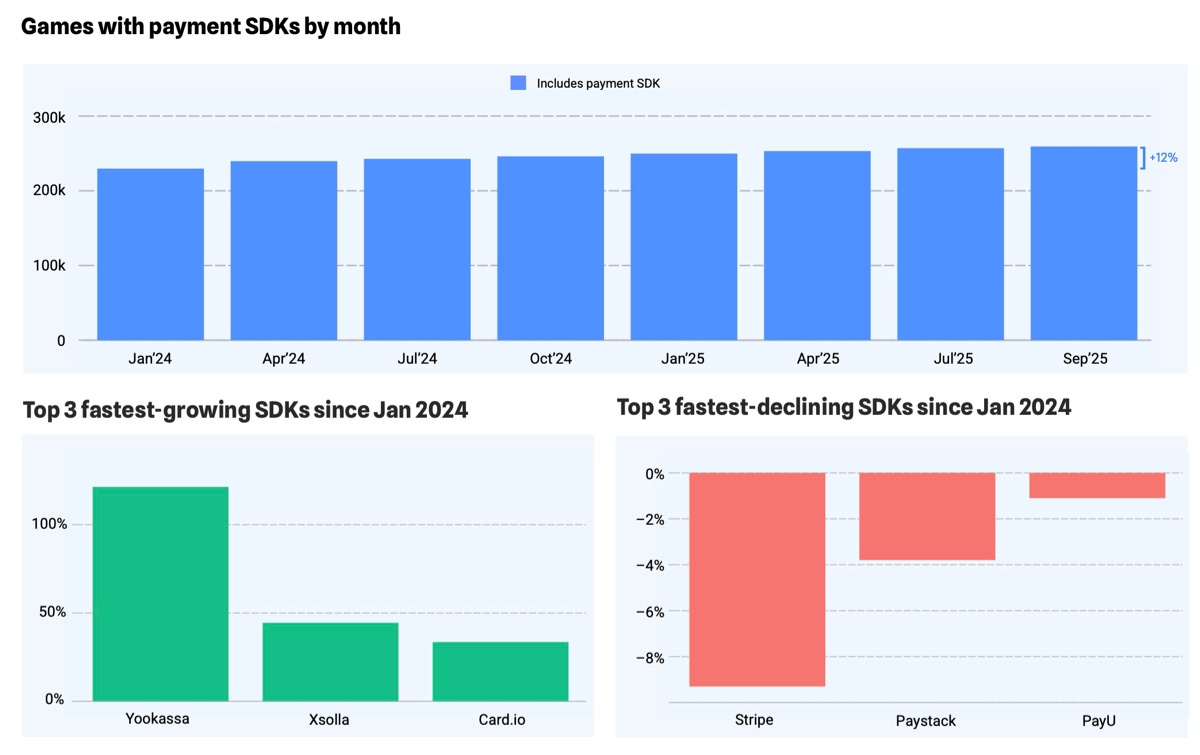

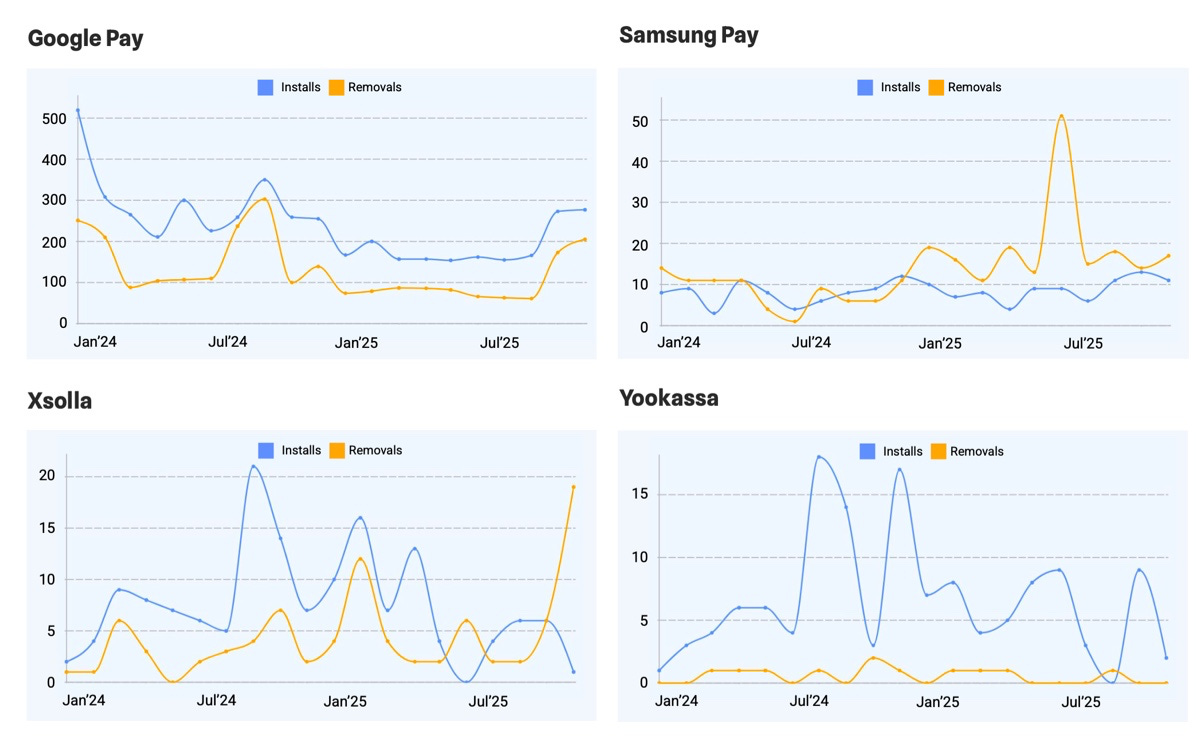

Among the fastest-growing payment SDKs over this period are YooKassa, Xsolla, and Card.io. SDKs that are losing the audience are Stripe, Paystack, and PayU.

-

The graphs show that SDK integration activity peaked in summer 2024 and then stabilized. For Samsung Pay, there is a visible spike in removals in 2025, which AppMagic attributes to the end of updates for Tizen devices rather than a broader trend toward bypassing store fees.

-

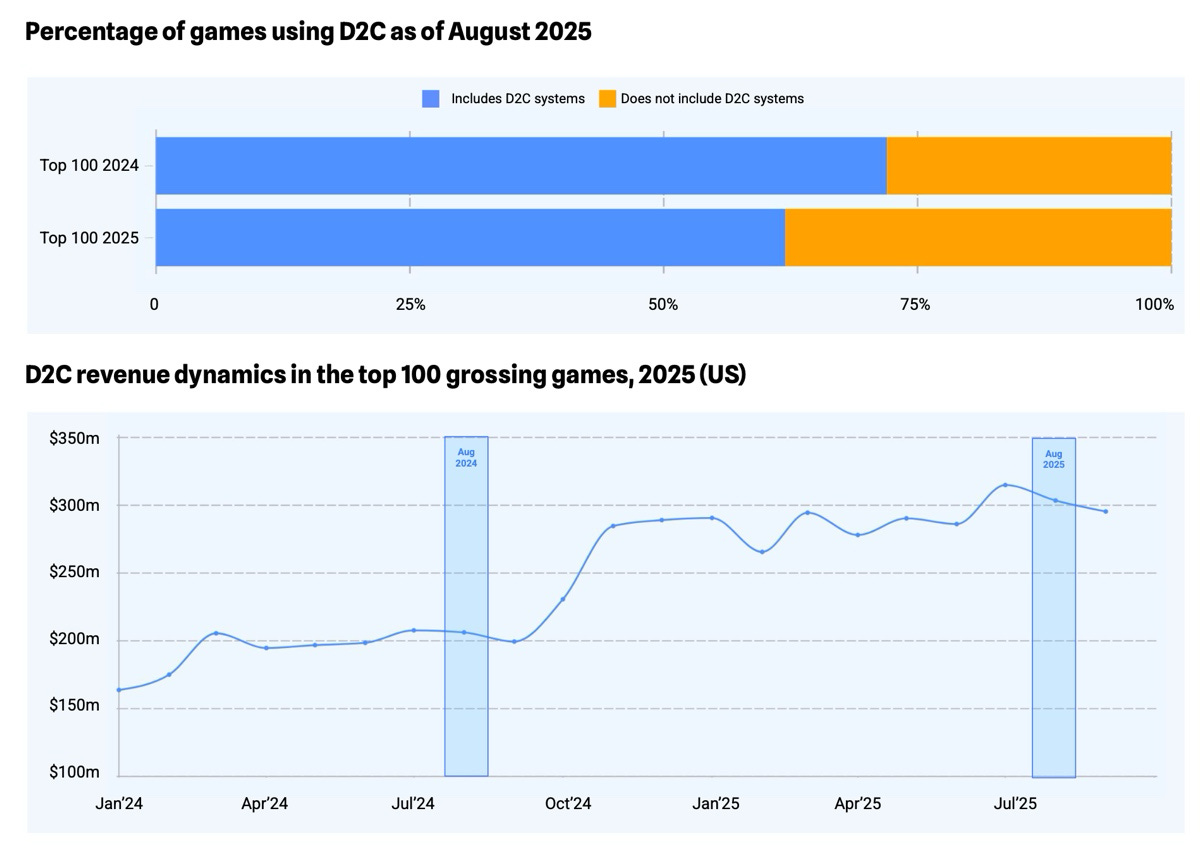

Surprisingly, the share of top-grossing titles using D2C tools decreased. In the 2024 year-end top 100, 72% of titles had D2C solutions. In the top 100 for the first half of 2025, only 62% of titles had them.

A word from our sponsor

Launch a fully branded web shop for your game in just one day with Xsolla’s Storefront – powered by AI for lightning-fast, 5-second site generation and simple drag-and-drop customization. Create native, game-like player experiences at any scale, localize instantly into 26 languages, adapt pricing for every region, and apply geo-restriction controls.

Effortlessly A/B test offers and layouts, go live with one click, and track results with built-in analytics for maximum player engagement and revenue growth.

Webshops are fast with Xsolla – join now!

-

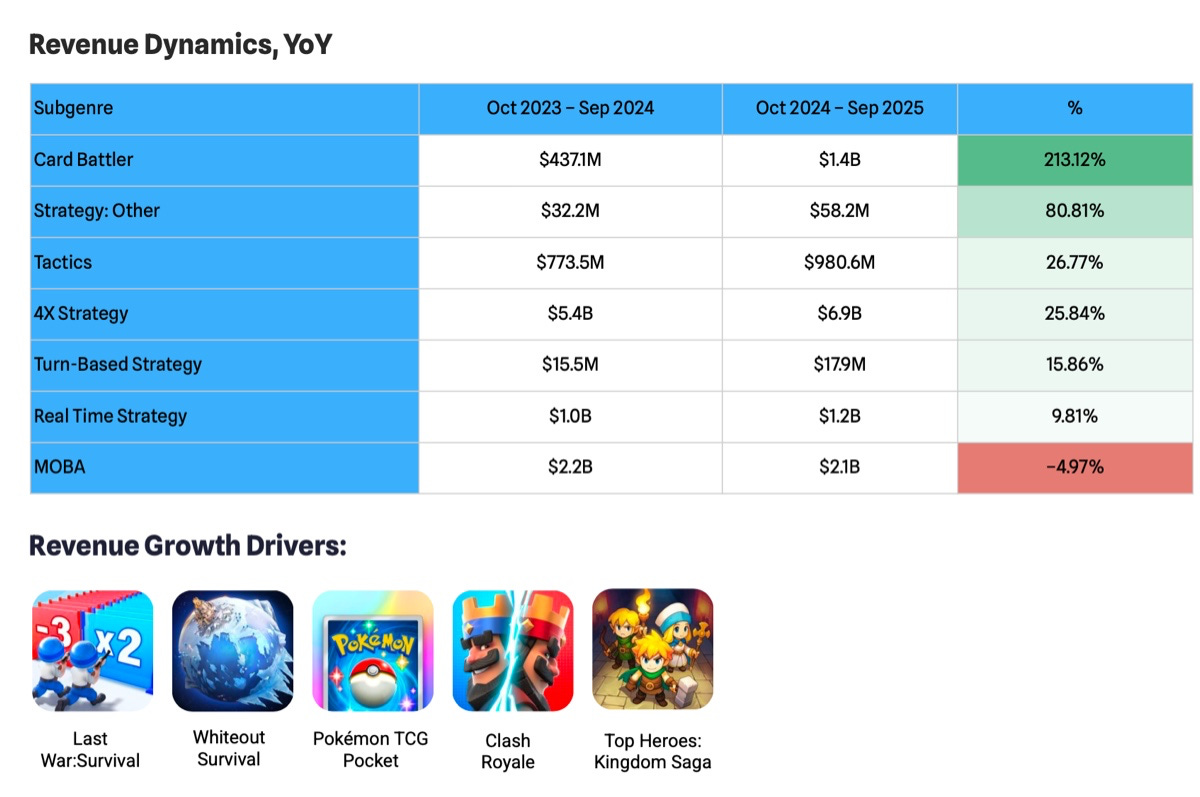

Over the year, strategy revenue grew from $10.8 billion to $13.5 billion (+25.6% YoY). On Google Play, it rose from $3.5 billion to $4.3 billion (+20.8%), and on the App Store from $7.2 billion to $9.3 billion (+27.9%).

-

Card battlers grew 213% year over year, tactical projects 26.77%, and 4X strategies 26%. Only MOBA titles are in negative territory, with revenue down 5% year over year.

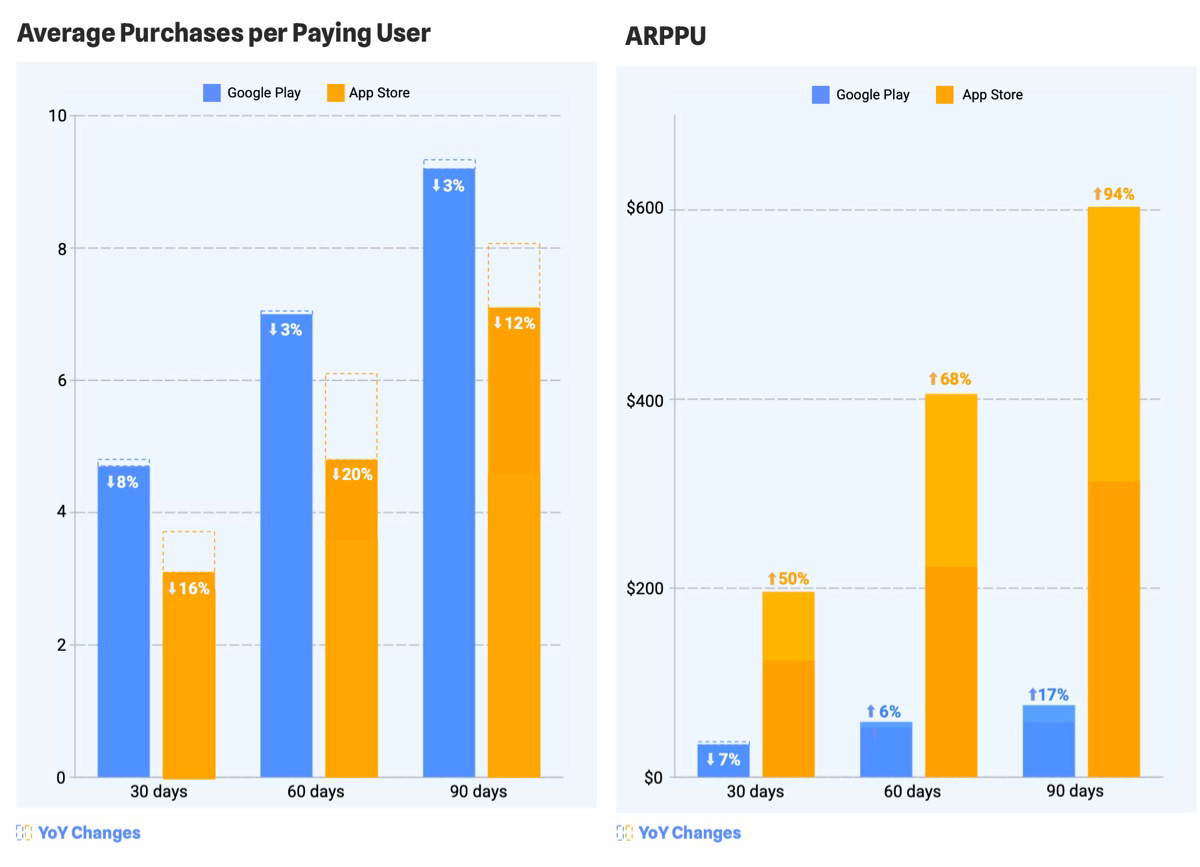

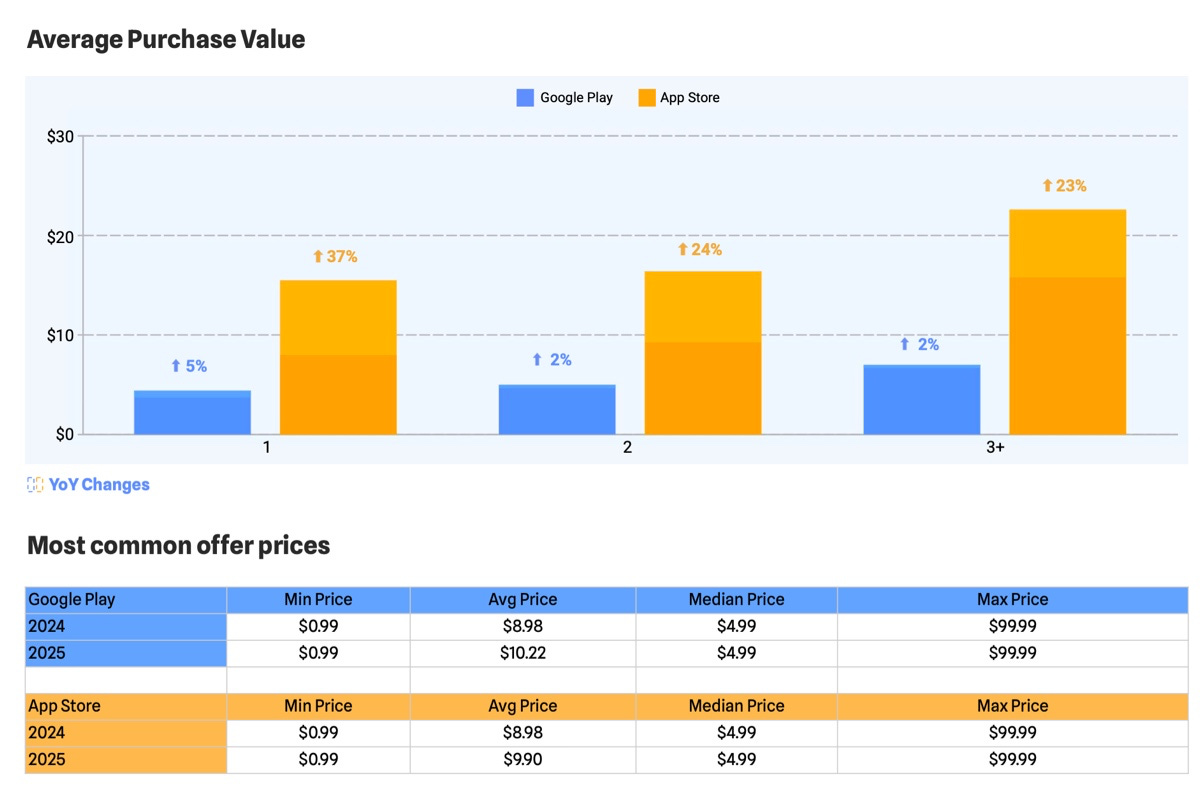

Payment behavior in strategy games (U.S., top 10 grossing)

-

By day 90 of a player’s lifecycle, paying users in strategy games spend twice as much as payers in casino games.

-

Historically, ARPPU in strategy on the App Store has been 4–5 times higher than on Google Play. In 2025, the gap widened to up to 8 times at certain stages of the user lifecycle.

-

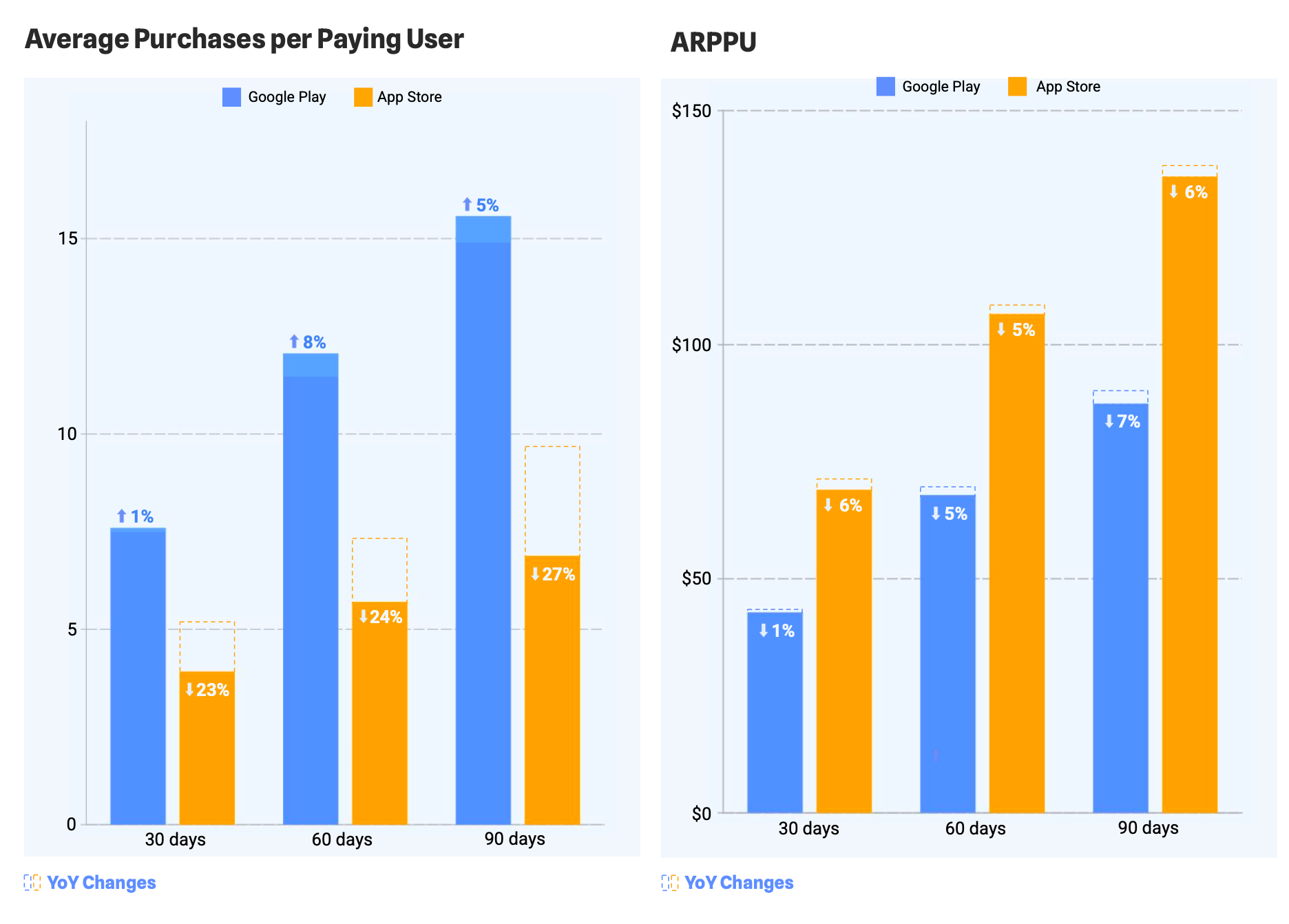

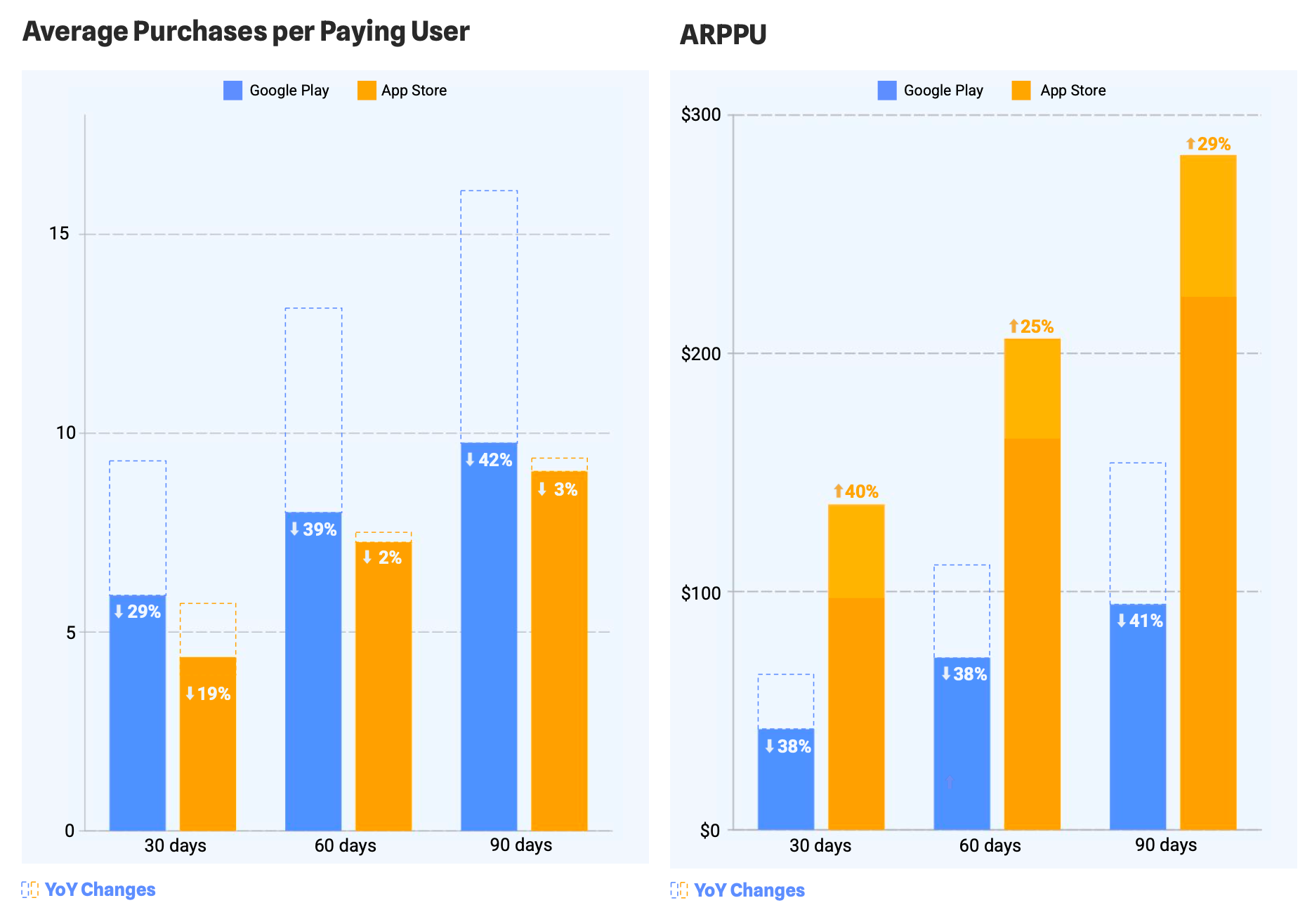

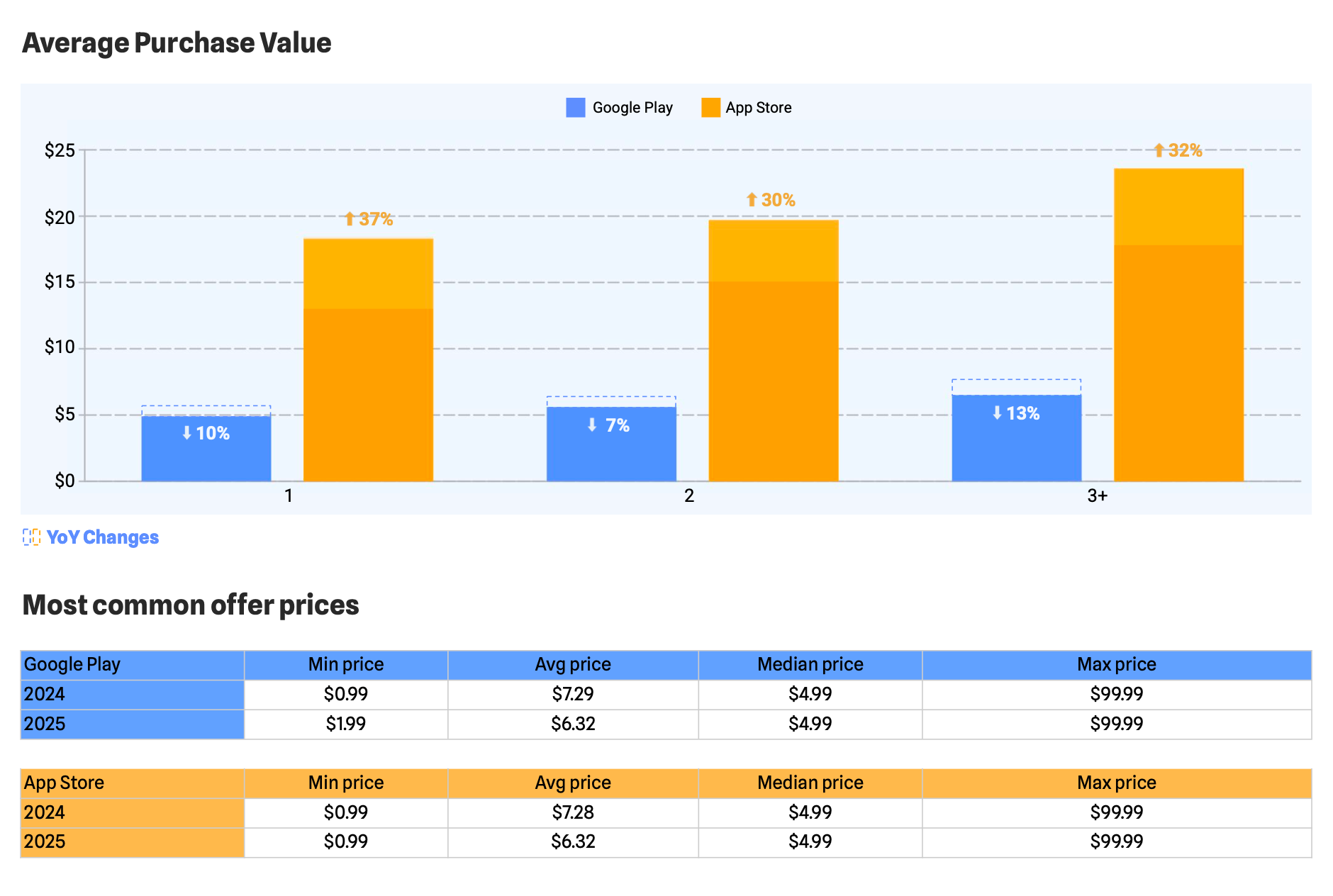

The average number of purchases per paying user is declining on both platforms, with the drop most noticeable on the App Store.

-

ARPPU on iOS, however, has increased significantly. Paying users are buying less often but choosing higher-priced items, and overall genre revenue on iOS has grown strongly. Android also shows growth, but not as large.

-

The average transaction on Google Play is about $7, while on the App Store it often exceeds $15.

-

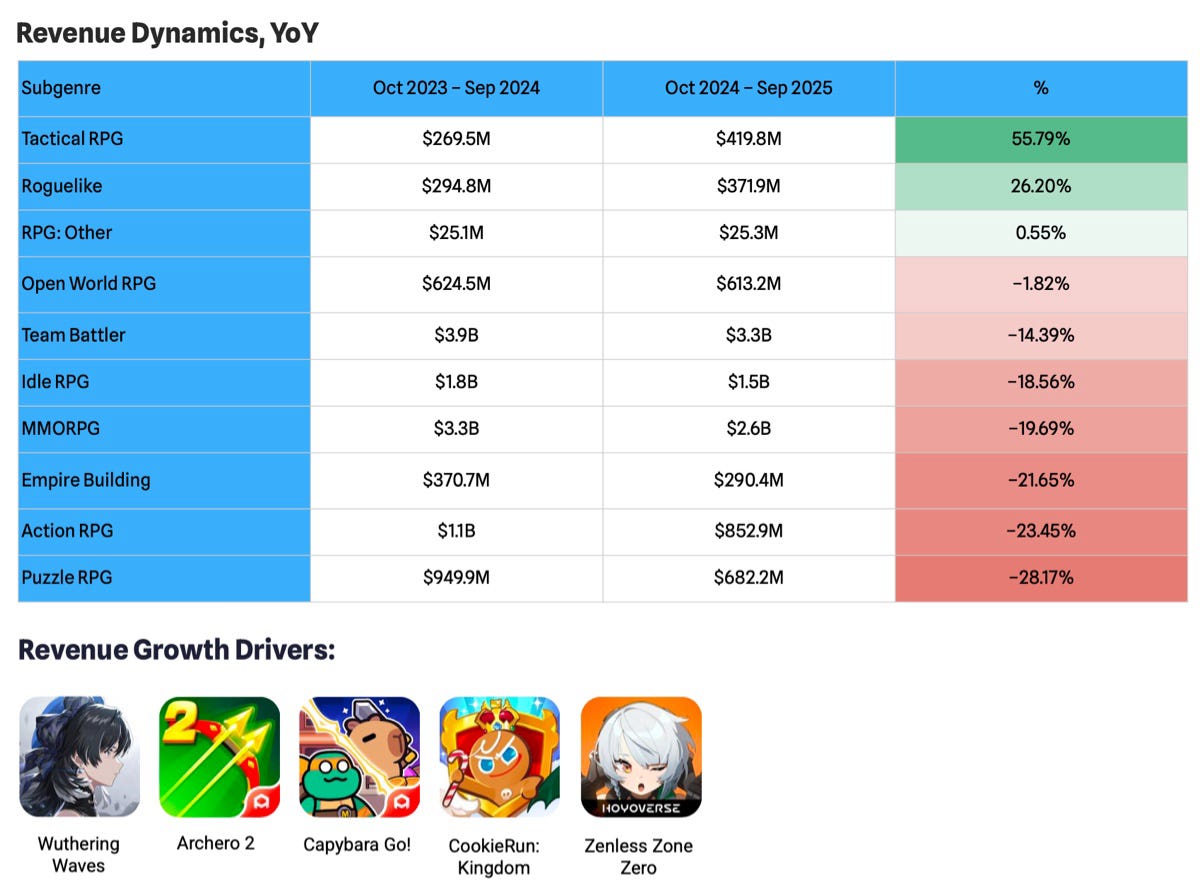

Both platforms declined by similar proportions. RPG revenue on Google Play fell 13.6% (from $5.3 billion to $4.6 billion), and on the App Store it fell 16.4% (from $8.4 billion to $7.0 billion). The genre saw especially sharp revenue declines in Asia over the past year, particularly in China (-25% YoY).

-

Despite the overall negative trend, some subgenres grew. Tactical RPGs increased 56% year over year, and roguelike titles grew 26.2%. All other subgenres are in a negative zone, with Puzzle RPG showing the steepest drop (-28.17% YoY).

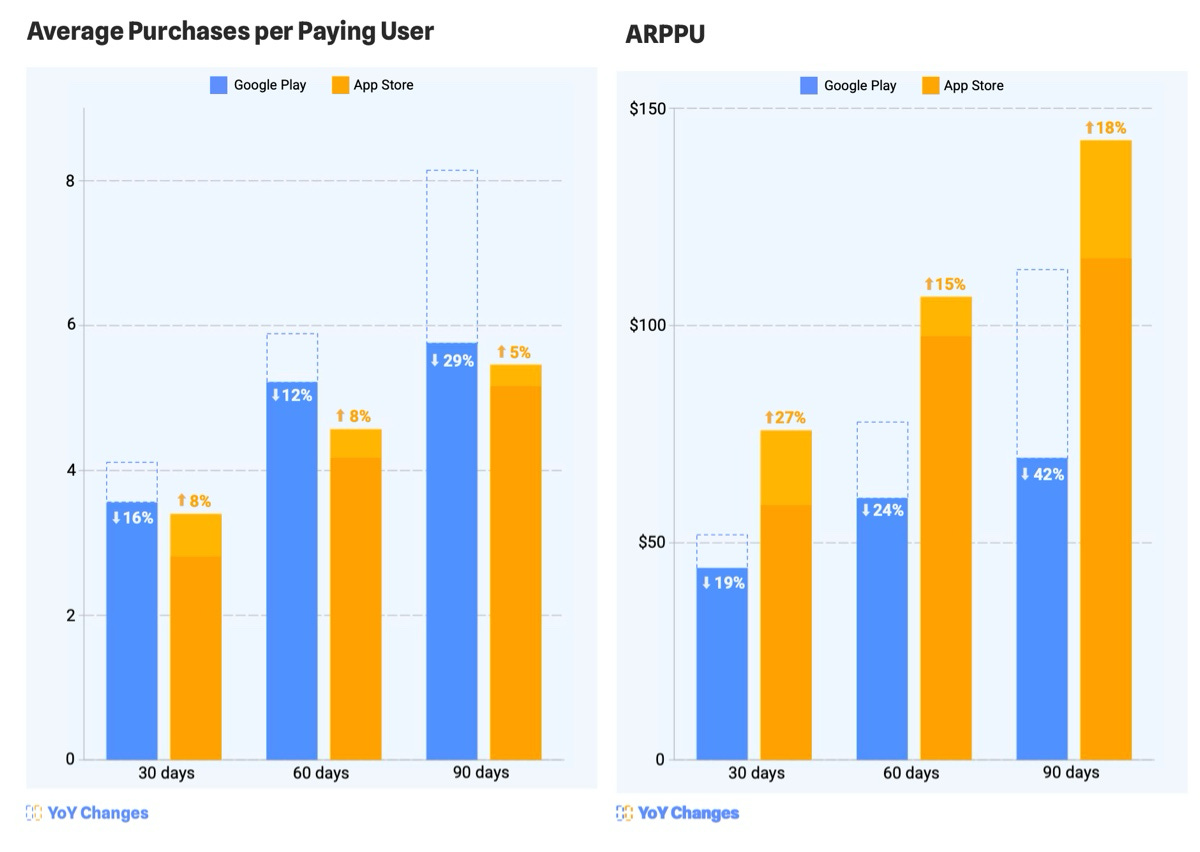

Payment behavior in RPG (U.S., top 10 grossing)

❗️Given the genre’s decline in Asia, U.S. figures may not reflect global revenue trends for RPG.

-

The most noticeable changes occurred on Google Play. The average number of purchases per paying user declined by up to 29% at various stages of the lifecycle. ARPPU by day 90 for paying users on Google Play fell 42% year over year.

-

On the App Store, by contrast, the trend is positive. ARPPU is up (by as much as 27%), and purchase frequency among payers has also increased (by up to 8%).

-

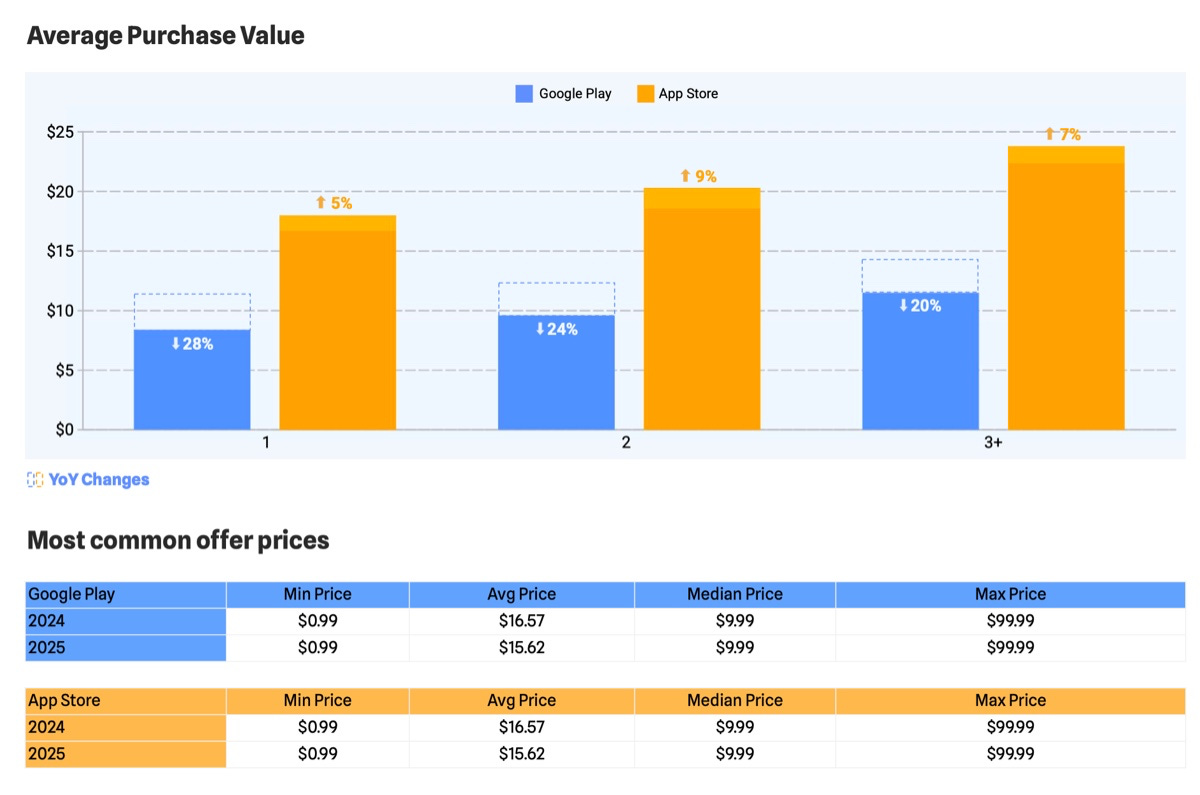

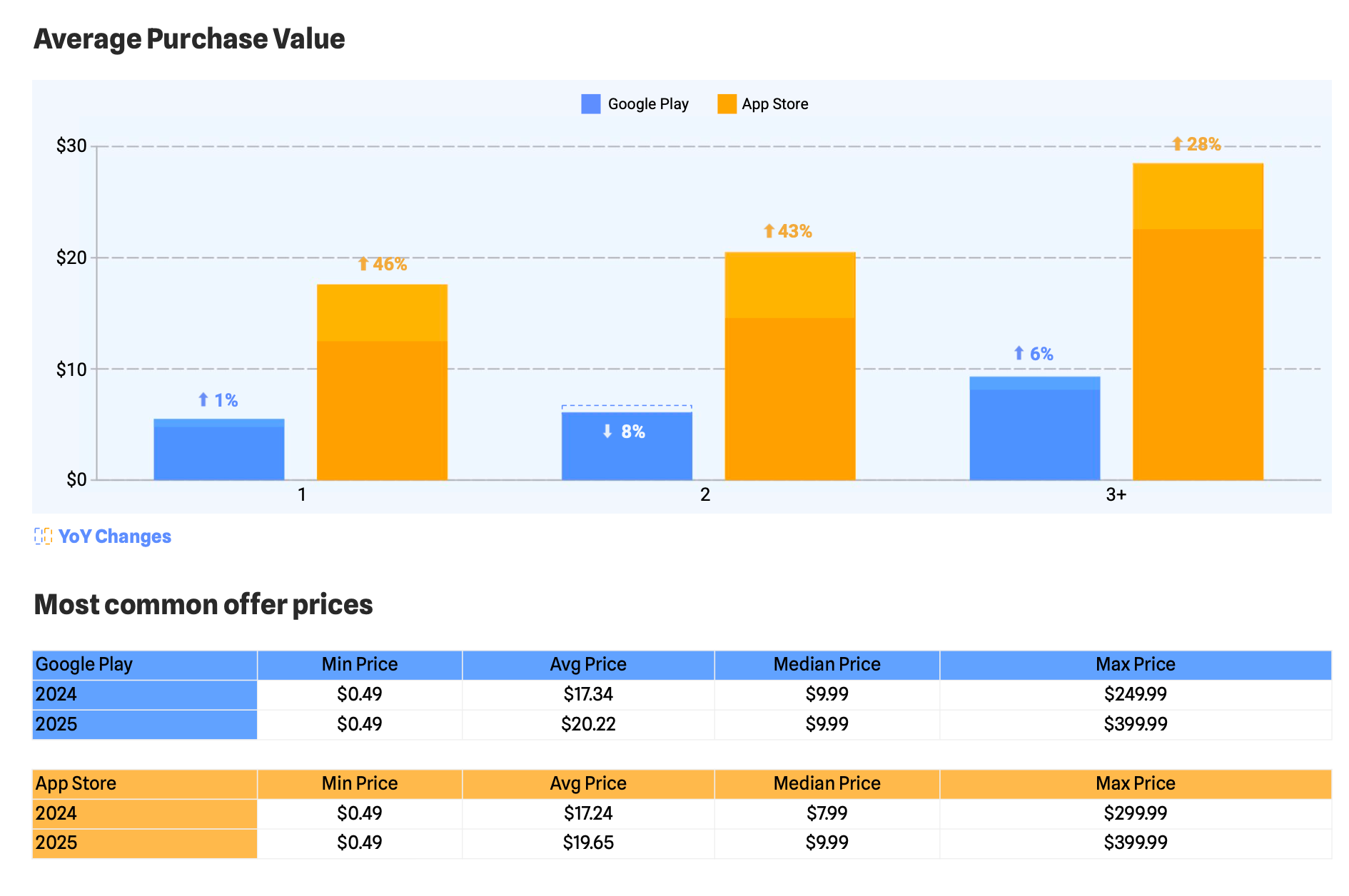

On Google Play, the average size of both first and subsequent purchases declined 20–28% year over year, while on the App Store, it increased.

-

The current average first-purchase price for paying users in the genre is $8.3 on Google Play and $17.9 on the App Store.

-

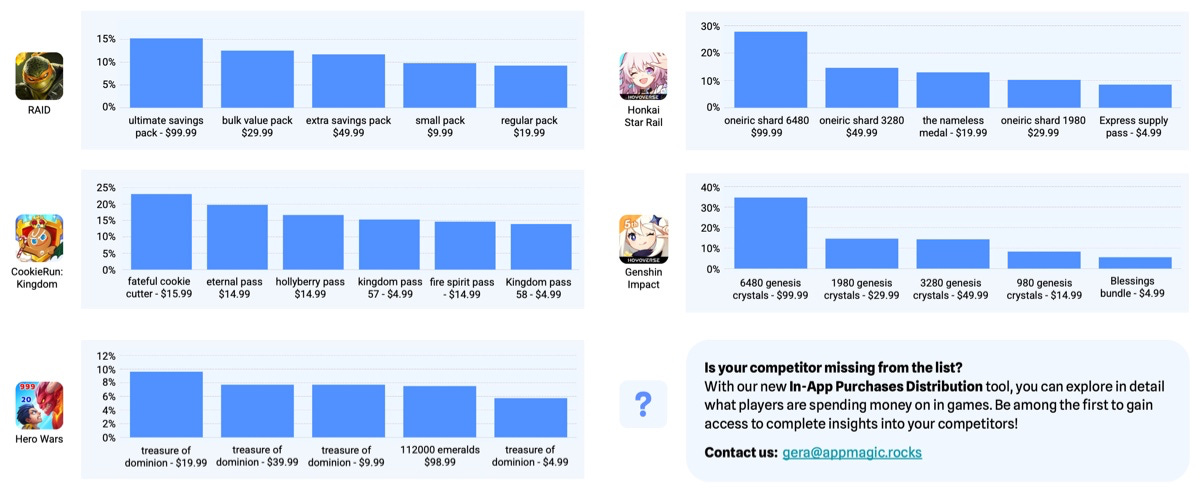

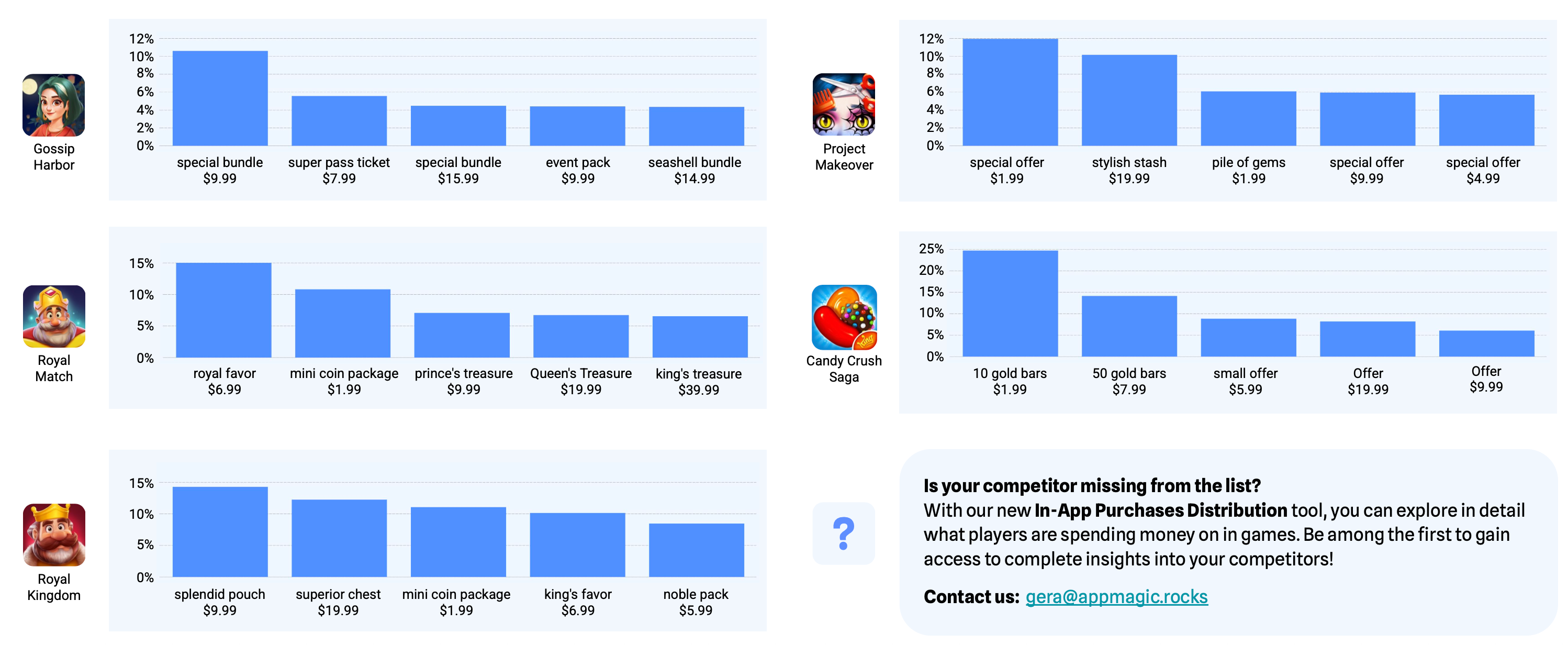

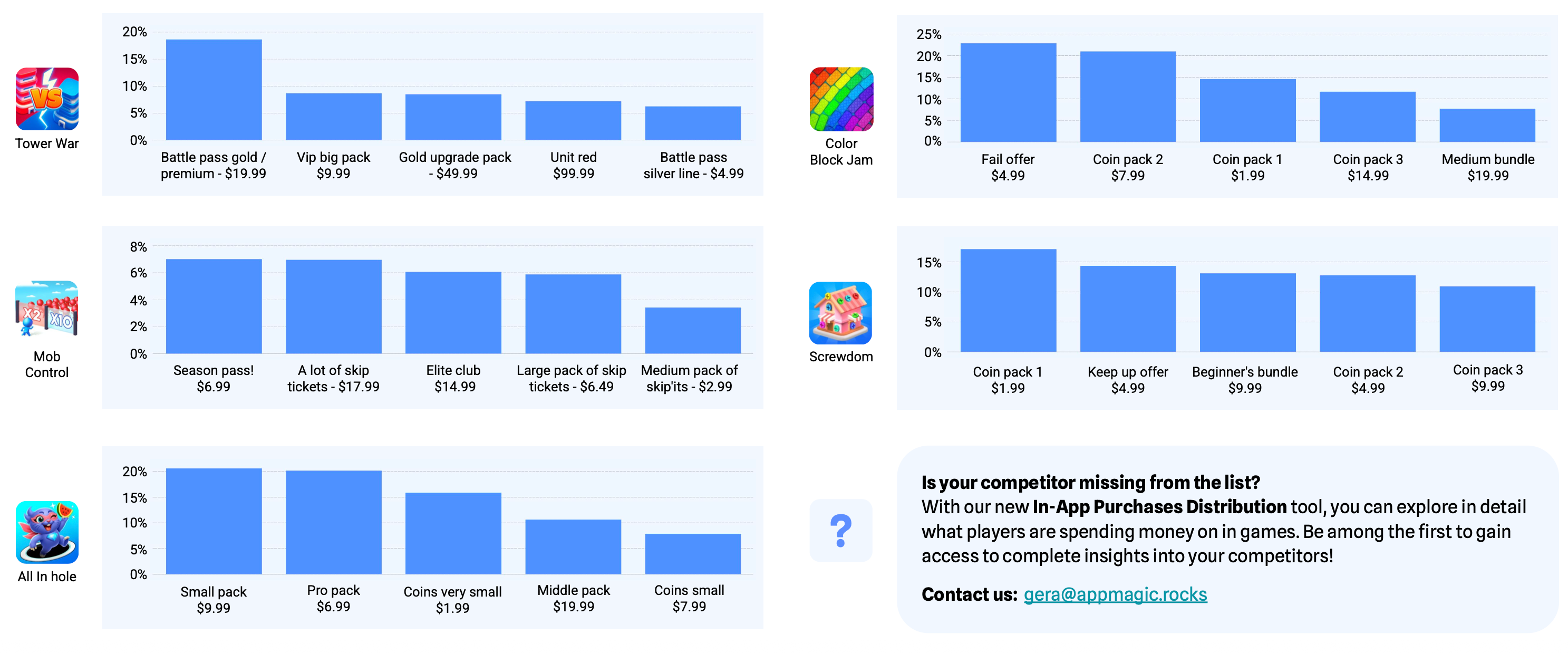

The most successful offers are still hard-currency packs and large bundles (RAID, Hero Wars, Genshin Impact, Honkai: Star Rail actively utilizing this).

-

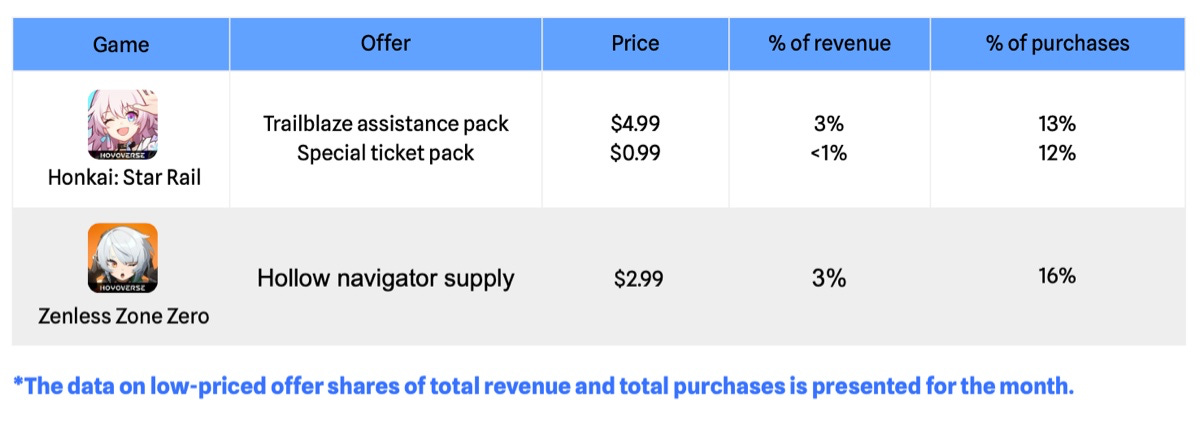

AppMagic notes that some midcore RPGs are experimenting with low-priced offers. During events in Honkai: Star Rail and Zenless Zone Zero, bundles are priced at $0.99–$4.99. In Honkai: Star Rail, individual bundles of this type generated 3% of monthly revenue and 13% of purchases (for $4.99). In ZZZ, a $2.99 bundle generated 3% of revenue and 16% of purchases. This is likely an attempt to convert as many users as possible into payers.

-

Puzzle revenue grew from $7.7 billion to $8.8 billion (+14.7% YoY). Google Play grew 8.9% (from $3.0 billion to $3.3 billion), and App Store puzzle revenue increased 18.5% (from $4.6 billion to $5.5 billion).

-

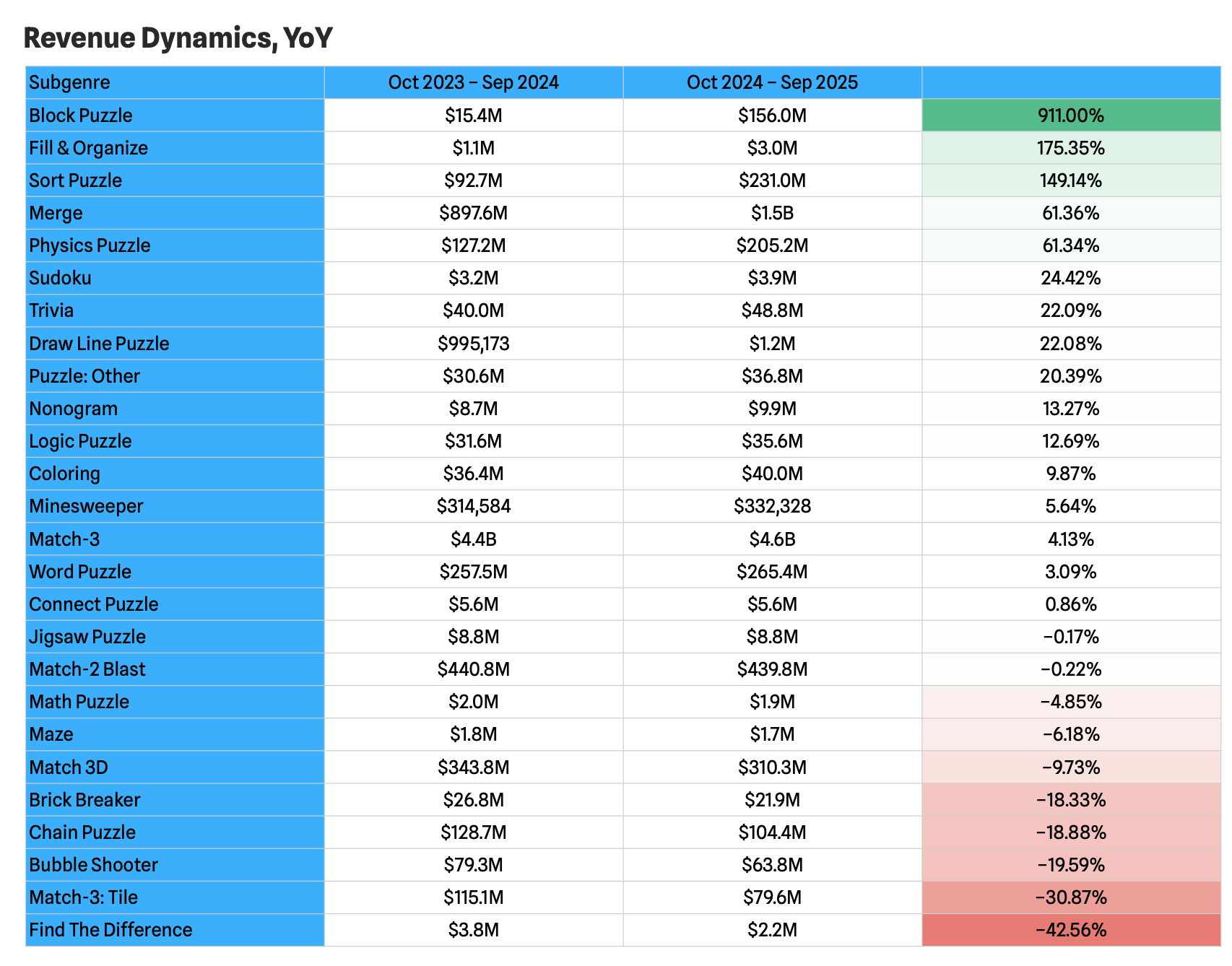

The genre contains a large number of subgenres, more than half of which are growing year over year. The most notable are Block Puzzle (+911% YoY, from $15.4 million to $156 million), Sort Puzzle (+149% YoY, from $1.1 million to $3 million), and Fill & Organize (+175% YoY, from $92.7 million to $231 million).

-

The Match-3 genre grew 4%. Given its large base, that translates into an additional $200 million over the last year (from $4.4 billion to $4.6 billion).

-

The steepest declines in puzzle are in the Find the Difference subgenre (-42.56% YoY, from $3.8 million to $2.2 million), Match-3: Tile (-30.87% YoY, from $115.1 million to $79.6 million), and Bubble Shooter (-19.59% YoY, from $79.3 million to $63.8 million).

Payment behavior in puzzle (U.S., top 10 grossing)

-

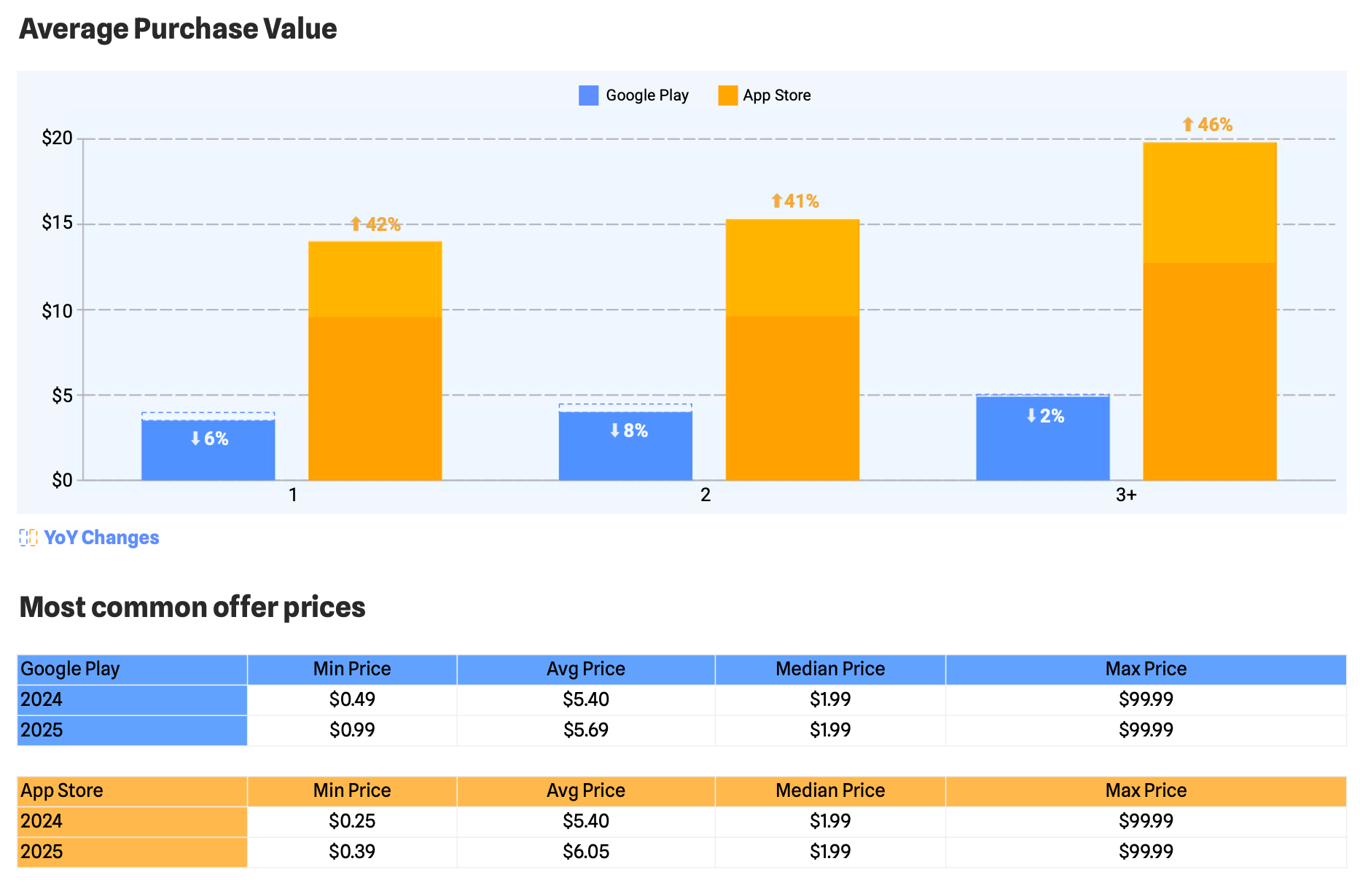

Despite overall market growth, among the top 10 grossing puzzle games, ARPPU declined slightly on both platforms, and on the App Store, the average number of purchases per paying user over 90 days dropped significantly (by as much as 27%).

-

At the same time, the average first purchase price on the App Store grew sharply. The average value of both first and subsequent purchases increased to 46% compared to last year. On Google Play, the average price decreased.

-

High-priced offers above $50 appear in the top revenue contributors far less often than in RPG.

-

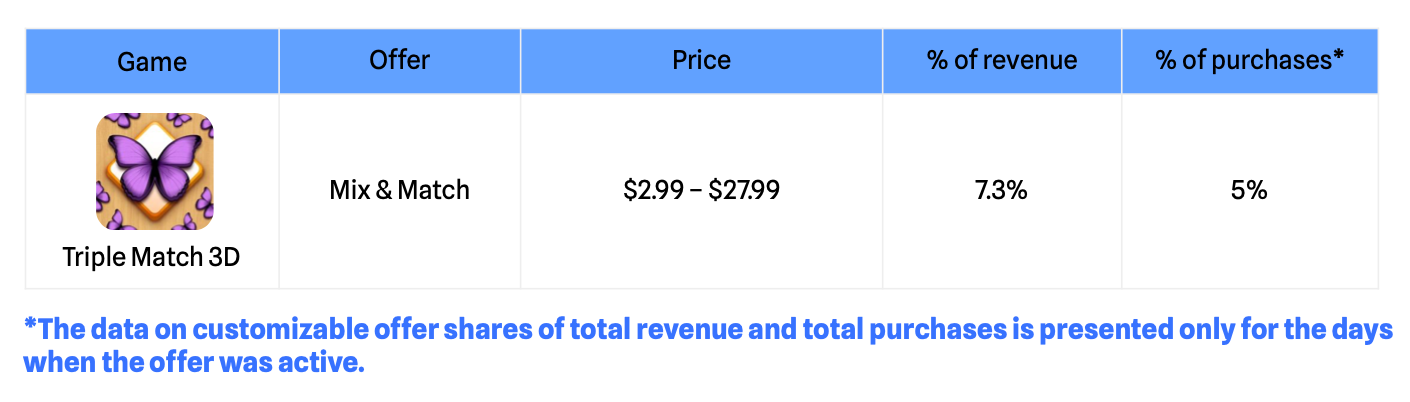

AppMagic highlights a trend toward customizable offers, where players assemble the bundle themselves. Merge Mansion and Merge Cooking have been running such offers episodically, while in Match Masters and Triple Match 3D, customizable offers have become a regular LiveOps element.

-

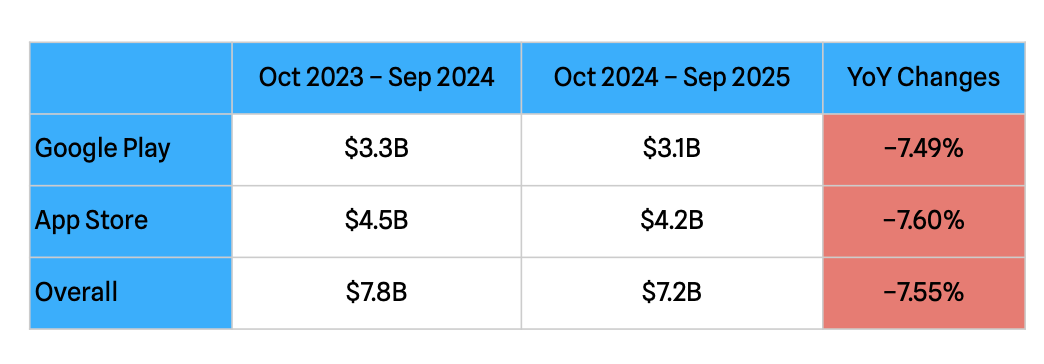

Casino is one of the few large segments in decline, going from $7.8 billion to $7.2 billion (-7.6% YoY). Over the past year, Google Play dropped 7.5% (from $3.3 billion to $3.1 billion), and the App Store fell 7.6% (from $4.5 billion to $4.2 billion).

-

In the United States, genre revenue declined 11%, while in the United Kingdom and Germany it grew slightly (+5% and +10%, respectively).

-

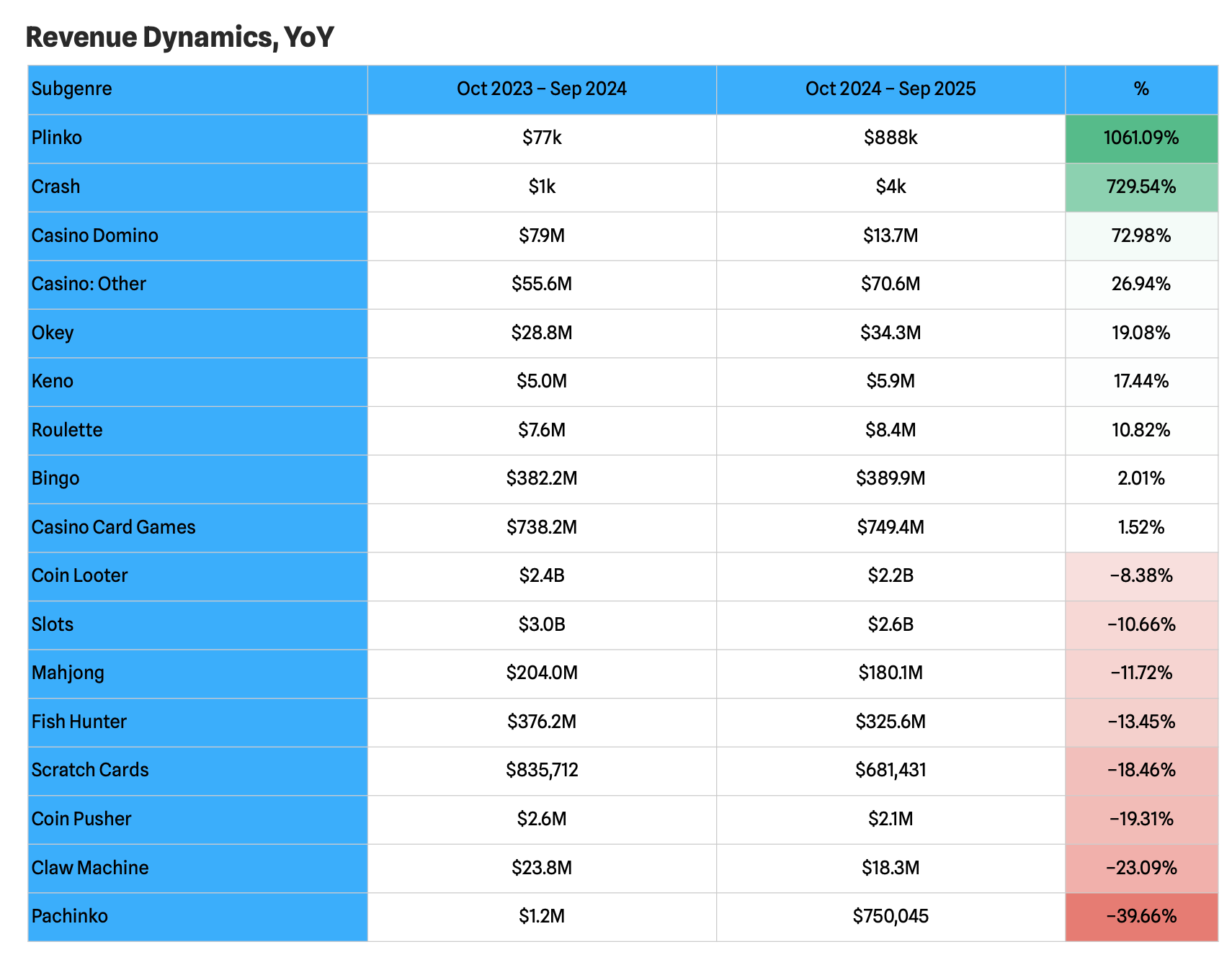

The most notable growing subgenres are bingo (+2.01% YoY, up to $389.9 million) and card-based casino games (+1.52% YoY, up to $749.4 million).

-

In percentage terms, Plinko (+1061% YoY) and crash games (+729.54% YoY) are the leaders, but these subgenres are so small in absolute revenue that their impact is negligible.

-

Coin Looter projects show a fairly noticeable revenue decline (-8.38%), with MONOPOLY GO!’s peak performance having been in the previous year. Slot games fell 10.66% year over year.

Payment behavior in casino (U.S., top 10 grossing)

-

The number of purchases per paying user has dropped significantly on both Android (by up to 42%) and iOS (by up to 19%). On Google Play, ARPPU also decreased (by as much as 41%), while on iOS it increased (by as much as 40%).

-

AppMagic notes that MONOPOLY GO!, for example, shows ARPPU growth on both Google Play and the App Store.

-

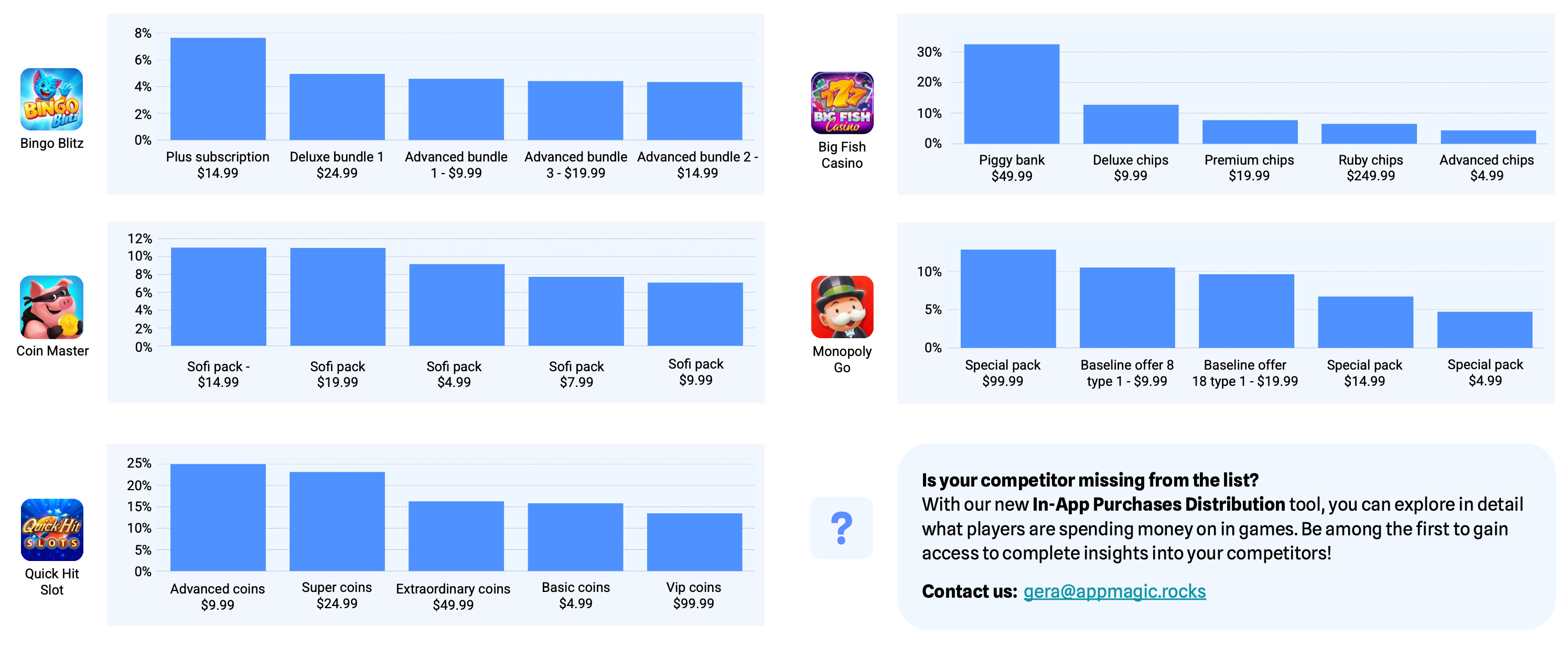

In Bingo Blitz, Big Fish Casino, Coin Master, and other titles, most revenue comes from currency bundles.

❗️In AppMagic’s classification, this category includes, for example, Roblox, Township, and Love and Deepspace. In my view, the category is too broad and does not clearly reflect trends within specific subgenres.

-

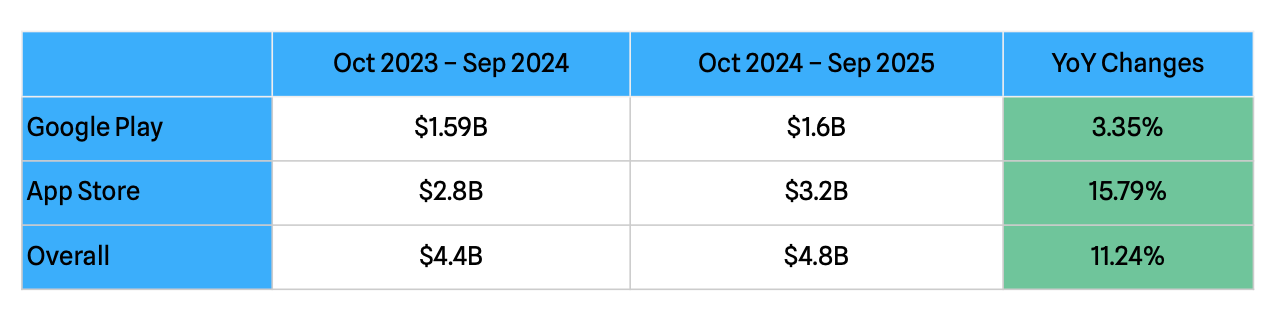

Over the past year, simulator revenue grew from $4.4 billion to $4.8 billion (+11.2% YoY). Google Play increased 3.4% (from $1.59 billion to $1.64 billion), while the App Store grew 15.8% (from $2.8 billion to $3.2 billion).

-

At the beginning of 2024, the genre on Google Play was generating 34% less revenue than on the App Store. By 2025, this gap had widened to 39%.

-

The biggest contribution to genre growth came from sandbox titles (+26.9% YoY, from $1.1 billion to $1.4 billion).

-

In terms of growth rate, work simulators increased 107.12% YoY (from $7 million to $14.5 million), and animal simulators grew 106.19% YoY (from $4 million to $8.3 million).

-

The steepest decline was in fishing simulators (-40.26% YoY, from $70 million to $41.8 million). Among the larger declining subgenres is Idol Training (games about training idols, Asian pop stars), down 8.33% year over year (from $646.8 million to $592.9 million).

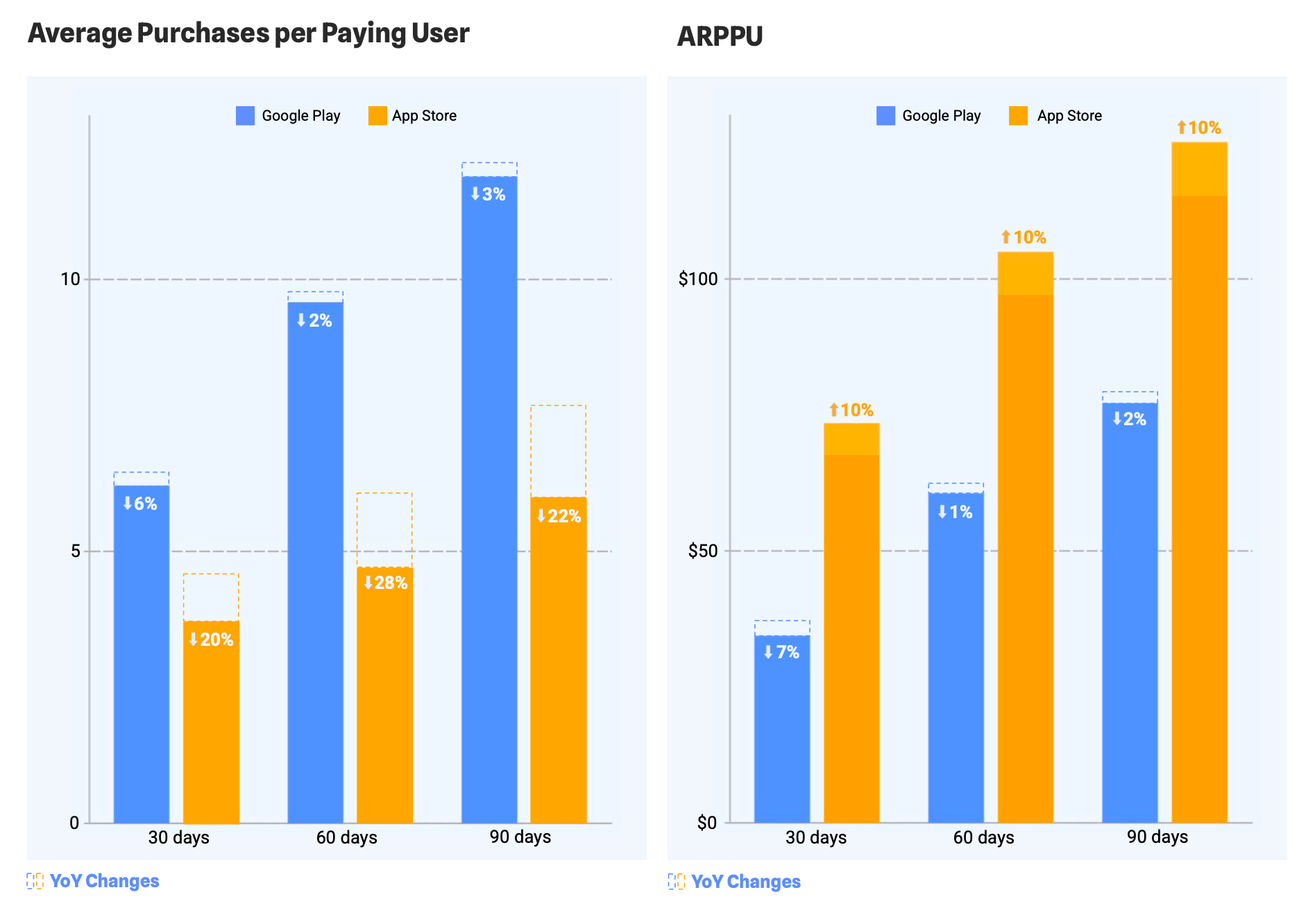

Payment behavior in simulation (U.S., top 10 grossing)

-

Purchase frequency among paying users declined across all platforms, by up to 6% on Google Play and up to 28% on the App Store.

-

ARPPU on Google Play also moved into the negative zone (down as much as 7%), while on the App Store, it increased about 10% across all timeframes.

-

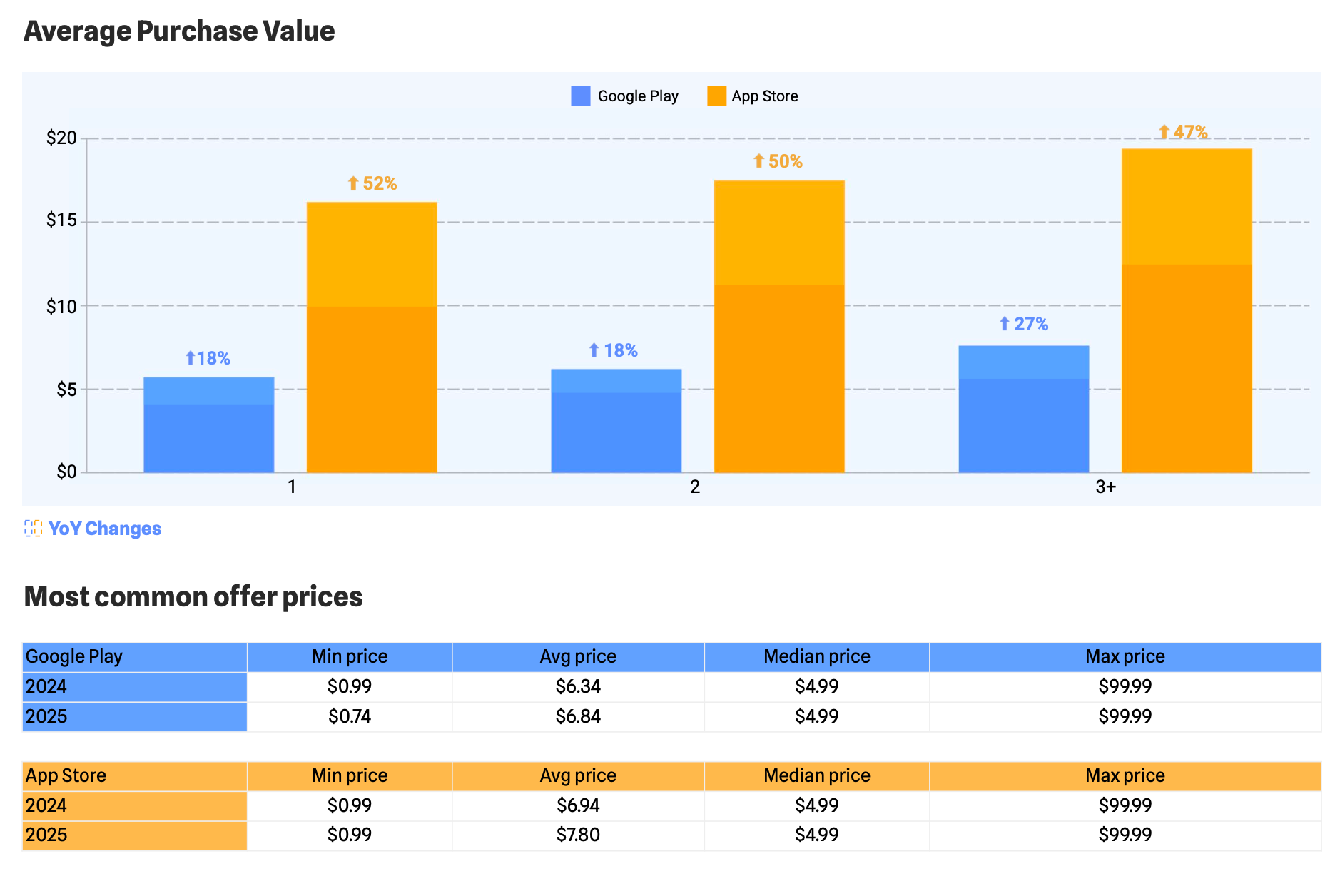

The average price on Google Play rose by 27% over the last year, and on the App Store, by up to 52%.

-

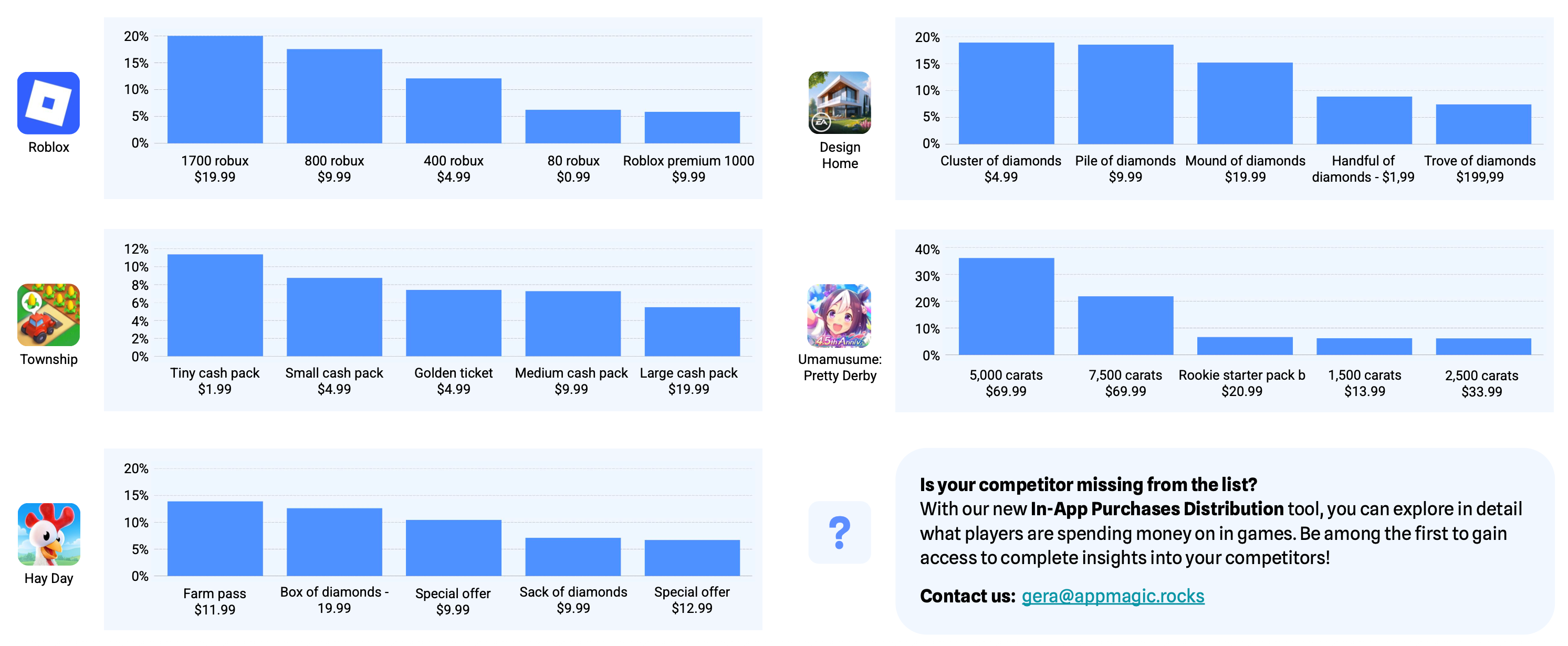

In most simulators, more than 40% of revenue comes from the top five offers, almost all of which are currency bundles.

-

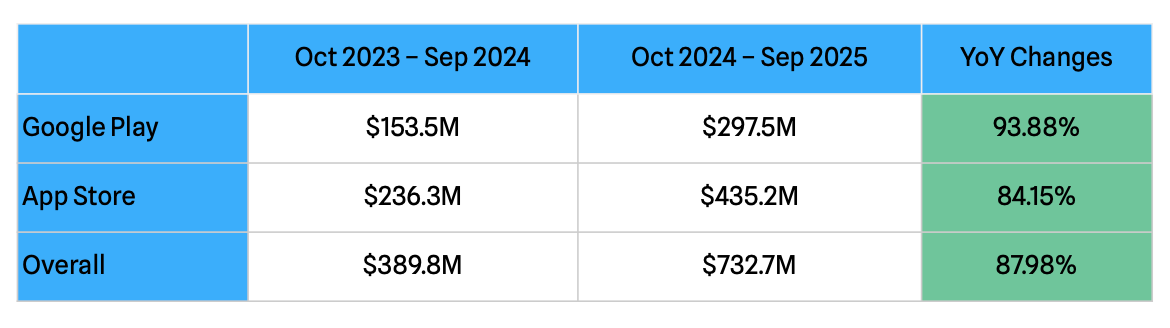

Hybridcasual is the fastest-growing segment. Combined IAP revenue rose from $390 million to $733 million (+88% YoY). Google Play grew 94% (from $153.5 million to $297.5 million), while the App Store increased 84% (from $236.3 million to $435.2 million).

-

Growth is driven by both higher download volumes and increasingly complex gameplay and monetization. AppMagic notes that hybridcasual titles are now appearing in top-grossing charts. There is still no sign of stabilization, suggesting the segment is very much in a growth phase.

-

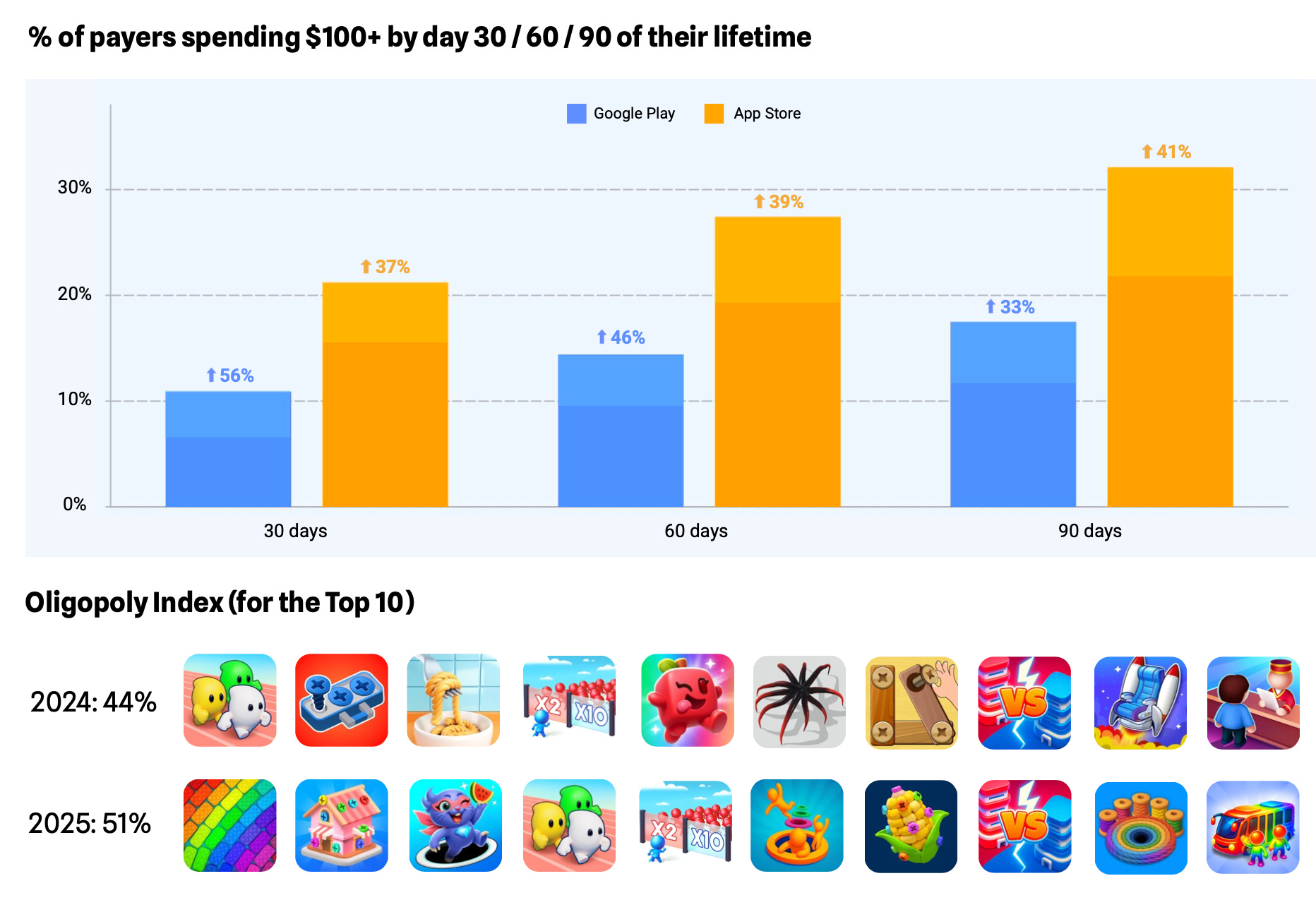

The share of payers who spend more than $100 in these games is increasing. In 2024, by day 90, 22% of paying users on the App Store had spent more than $100. In 2025, that figure rose to 32%. Similar dynamics are visible on Google Play.

-

At the same time, entering the niche is becoming harder, although new projects are still breaking into the top charts.

A word from our sponsor

Launch a fully branded web shop for your game in just one day with Xsolla’s Storefront – powered by AI for lightning-fast, 5-second site generation and simple drag-and-drop customization. Create native, game-like player experiences at any scale, localize instantly into 26 languages, adapt pricing for every region, and apply geo-restriction controls.

Effortlessly A/B test offers and layouts, go live with one click, and track results with built-in analytics for maximum player engagement and revenue growth.

Webshops are fast with Xsolla – join now!

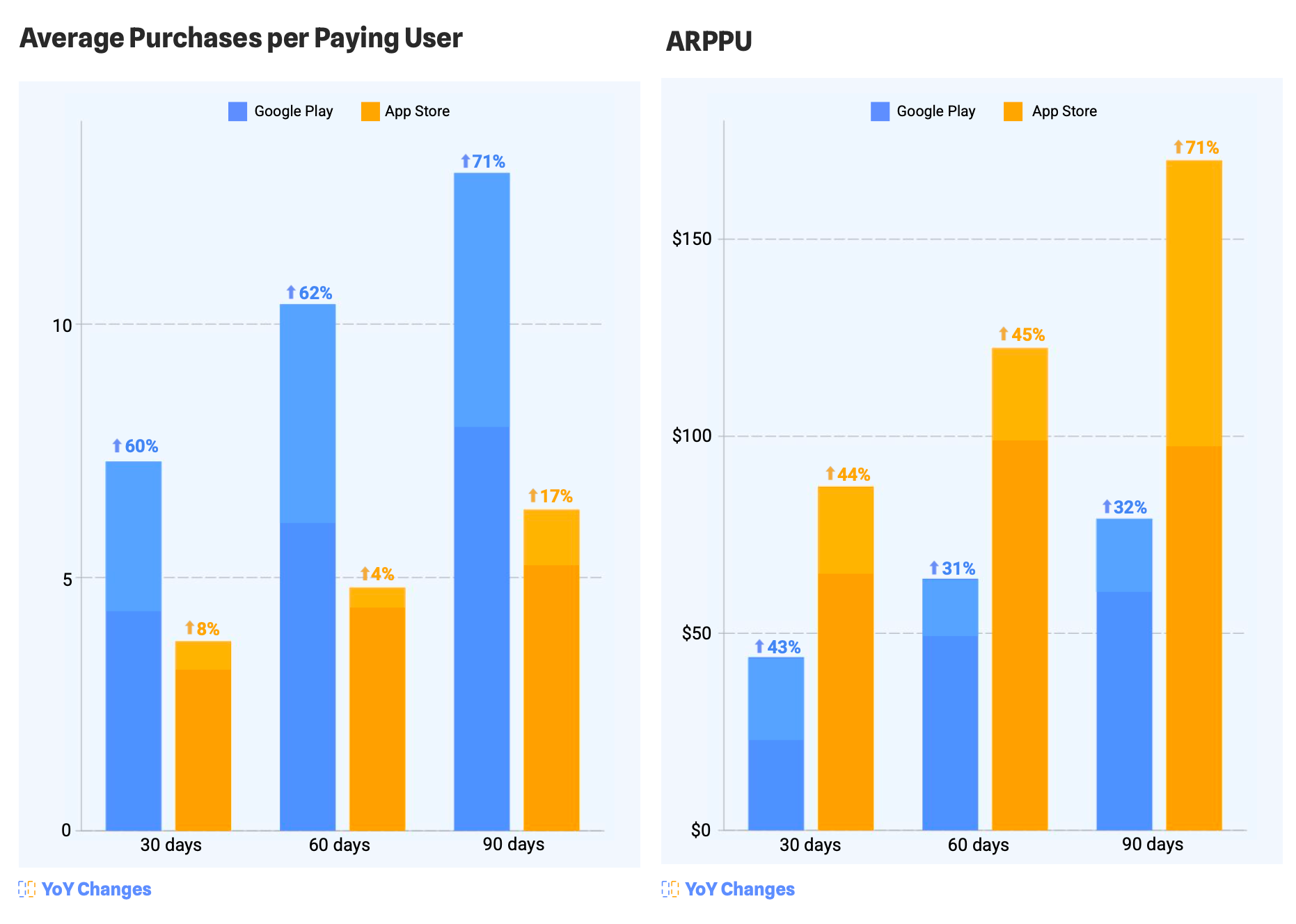

Payment behavior in hybridcasual (U.S., top 10 grossing)

-

All payment metrics among payers are up across all platforms. On Google Play, purchase frequency increased by up to 71%. On the App Store, growth is more modest, up to 17%.

-

ARPPU on the App Store grew by up to 71% at the 90-day mark, and on Google Play by up to 43%.

-

The main revenue sources are low-priced hard-currency bundles and loss offers. Seasonal passes and battle passes are also visible in the revenue mix.

-

Season passes are now a standard of the genre, but their share of total revenue is relatively modest. One of the most successful implementations is in Mob Control, where they account for 11% of total revenue.