My name is Brian Blase, founder and president of Paragon Health Institute. From 2017 through 2019, I served as a Special Assistant to the President for Economic Policy at the White House’s National Economic Council, and from 2014 through 2015 I worked for the Senate Republican Policy Committee under then-Chairman John Barrasso. I appreciate the opportunity to testify on this important topic.

Why Health Care and Coverage Are Increasingly Unaffordable

For tens of millions of Americans, neither health care nor health coverage is affordable. And once we account for the taxes and debt required to finance government health programs, health care is not just unaffordable; it is a direct threat to our fiscal future.

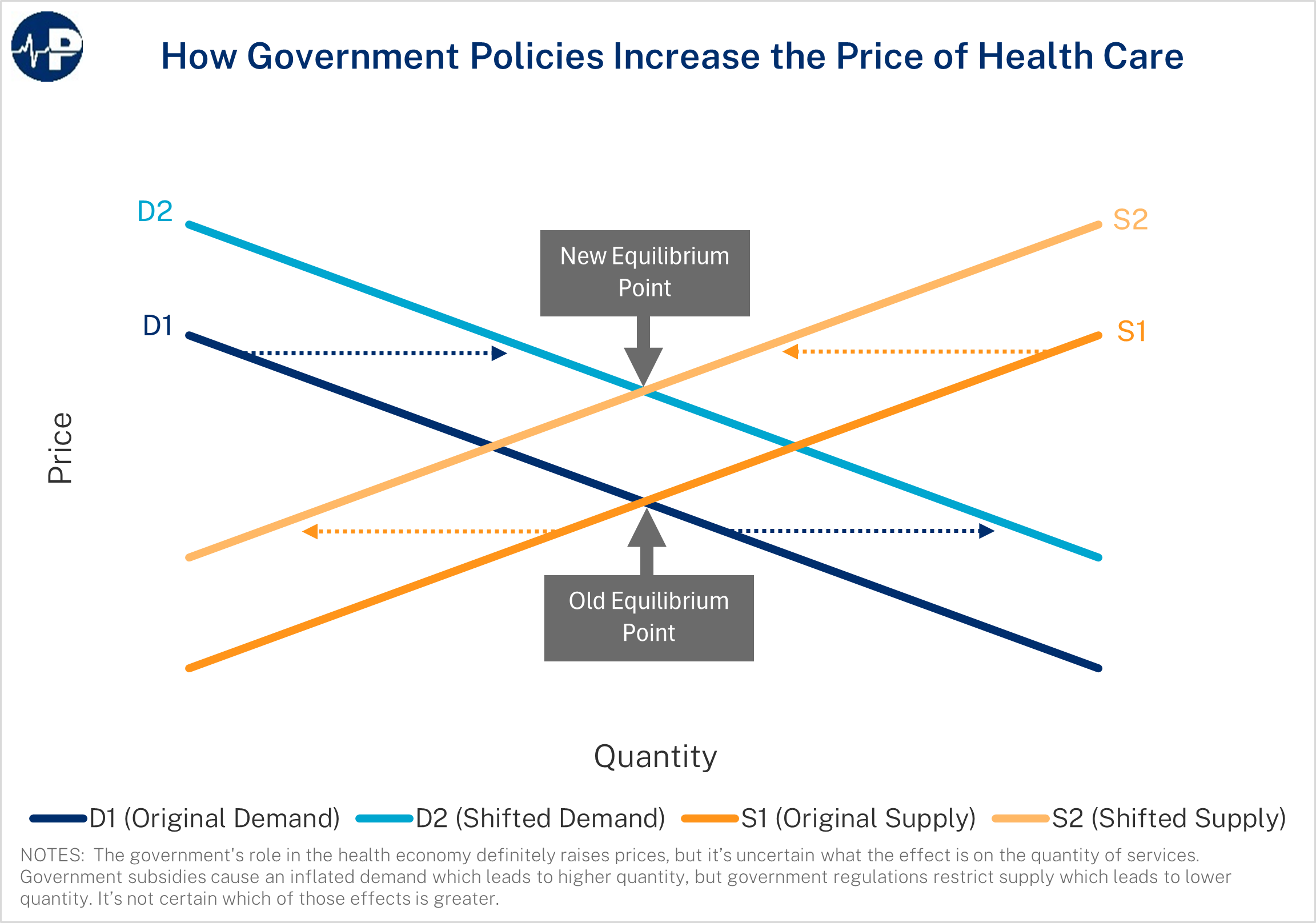

Counterproductive government policies have significantly contributed to high and rising health care prices and spending—both by inflating demand through excessive subsidies and mandates and by restricting supply through regulations that protect incumbent insurers, hospital systems, and provider monopolies. These combined forces drive prices higher and produce rampant inefficiencies throughout the health sector.

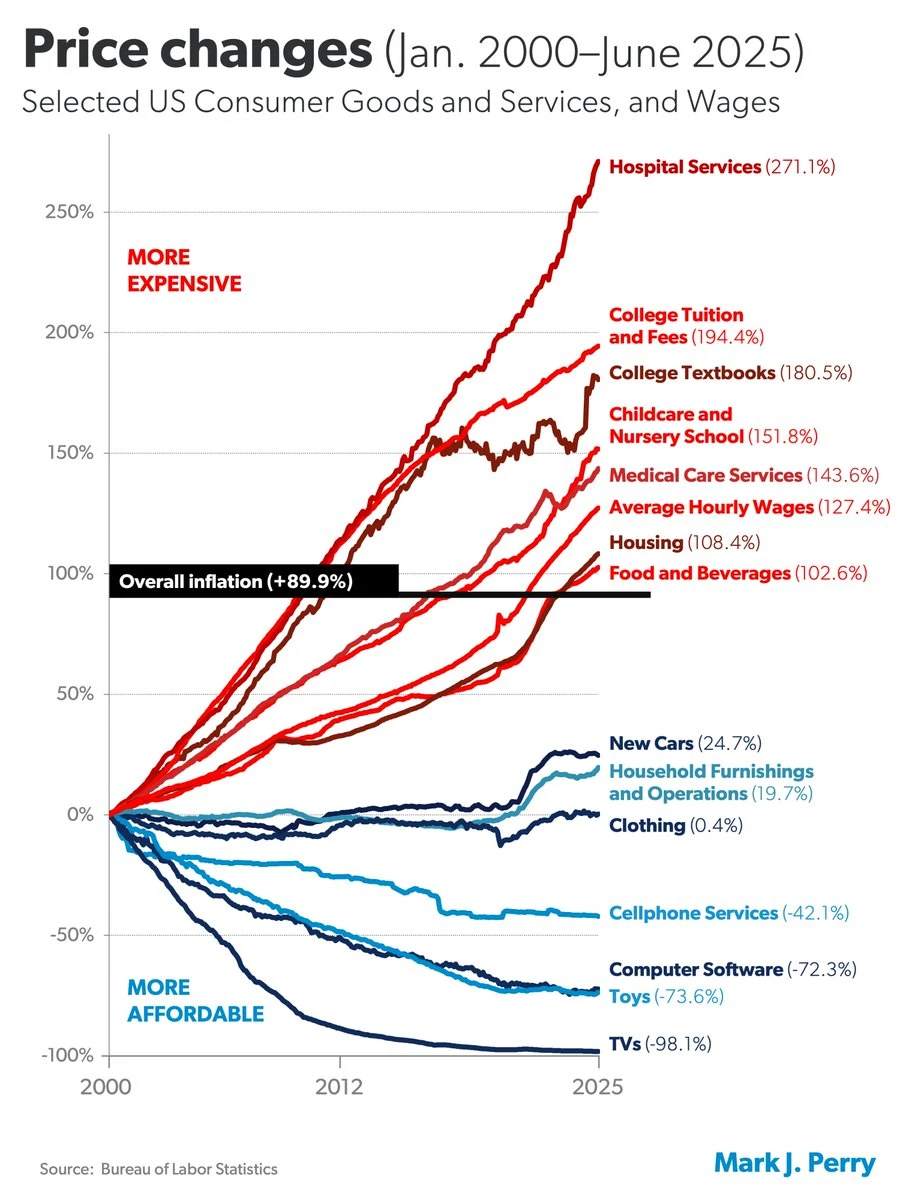

In many sectors of the economy, products and services have improved in quality over time while real prices, after accounting for inflation, have declined (Figure below: “Price Changes.”) Health care is a glaring exception. Rather than delivering higher quality at lower real prices, the hospital sector—now the largest driver of U.S. health spending—has delivered the opposite: steeply rising prices, declining competition, and consolidation that shields providers from market discipline. As the data clearly show, prices for hospital services—the largest component of health care expenditures—have risen three times faster than general inflation since the turn of the century. No major industry has experienced faster price escalation than hospitals.

As health costs have risen, insurance premiums have soared. At the same time, plan deductibles have risen dramatically, too. To understand why costs have risen so sharply, policymakers must look beyond market forces and recognize how federal policy itself—particularly the structure of the Affordable Care Act (ACA)—has directly contributed to higher premiums, narrower networks, and reduced affordability.

In 2024, health care spending was approximately 18 percent of U.S. gross domestic product (GDP), a 38 percent increase from 2000 when it was 13 percent of U.S. GDP. A significant part of this health care spending is waste, with credible estimates suggesting that up to a quarter of health care spending provides people on with little, if any, health benefit.

Despite widespread inefficiencies in the U.S. health sector, there are pockets of excellence. In the past few decades, there have been meaningful advances, such as a decline in cardiac mortality, improvement in cancer survival rates, a cure for Hepatitis C, and new AIDS treatments. Yet health outcomes have stagnated despite the ACA’s new spending and the significant expansion of Medicaid. American life expectancy was lower in 2019 (a pre-pandemic measure) than it was in 2013, before the ACA’s coverage and spending provisions took effect.

Government Policies Drive Higher Prices and Distort the Market

These problems stem not from a lack of government action but from perverse incentives embedded in government programs. There are many policies—at both the federal and state levels—that raise health care prices and costs. In most areas of the economy, high prices signal high value. But in health care, heavy government involvement—driving excessive third-party payment and consolidation—means that high prices often reflect distortions. A major consideration for policymakers in addressing high prices for medical care should be examining how existing government policies contribute to the problem and then focusing on reform.

Federal tax and spending programs inflate health care demand and generate large expenditures that produce little, if any, value. Roughly a quarter of health care spending provides no health benefit—and some of it may even harm patients. Reforms are clearly needed, particularly to our health care entitlement programs.

How Third-Party Payment and Government Regulation Inflate Costs

A primary way that government inflates health care prices and costs is through tax and spending policies. In 2023, government health care spending—including both state and local government spending—was 48 percent of total U.S. health care expenditures.

Federal policy also strongly shapes private sector health care spending. One important policy is the long-standing tax exclusion for employer-sponsored insurance. The exclusion contributes to higher overall health spending by encouraging compensation to flow through health benefits rather than wages and because its value grows as premiums rise. However, these effects are far less pronounced than under the ACA’s subsidies. Unlike the ACA subsidies, the exclusion does not penalize additional work, does not encourage misreporting of income, and does not generate the type of escalating dollar-for-dollar subsidy increases that fuel the ACA’s premium spiral. The White House estimates that the exclusion will reduce federal revenue by $395 billion in 2025—a substantial amount—but it remains considerably less distortionary than the ACA’s subsidies.

The key economic reality is that when government subsidizes something, that thing becomes more expensive. Subsidies increase demand, raise prices, and thus increase total spending in that area. Substantial and open-ended federal subsidies mean most Americans hold comprehensive insurance coverage. This in turn puts upward pressure on health care prices and diminishes the amount of shopping for health coverage and care.

For complete economic analysis, the taxpayer share of the total cost must be considered.

Every subsidy is ultimately financed by other households—through higher taxes or greater debt. More debt represents higher taxes in the future, either through direct taxes or higher inflation. And there is substantial deadweight economic loss from the higher spending. The deadweight loss of taxation represents the value of forgone productive activity. According to assumptions used by the Council of Economic Advisors about deadweight loss, extending the Biden COVID credits would cause about $200 billion of deadweight loss over the next decade.

Although the magnitude of government subsidies for health care increases prices and spending, the design of the subsidies is also problematic. Historically, government programs and tax policy have encouraged third-party payment of health services. Thus, for the vast majority of health care transactions, individuals do not directly spend their own money but instead rely on government programs or their insurance plans, which are generally either directly subsidized or tax-favored. Insurance should protect people from catastrophic expenses—not function as a pre-paid medical subscription for every routine or shoppable service. Yet federal policy pushes precisely that model, severing the link between patients and prices, eroding incentives to economize, and converting everyday spending into bloated third-party transactions.

Lessons from Markets Where Consumers Control Spending

Although inflation in health care services has been substantial, health care services where third-party payment is limited—such as cosmetic and LASIK eye surgery—have seen real price declines as quality has significantly improved. These examples demonstrate what happens when consumers spend their own money and providers compete on price—precisely the opposite of the ACA’s structure. Also, a number of physician practices and medical centers, such as the Oklahoma Surgery Center, do not accept insurance and have much lower average prices.

The Affordable Care Act’s Inflationary Spiral

The ACA promised affordable, high-quality insurance. It failed to deliver. Premiums and deductibles have escalated—often for coverage that excludes the best hospitals and doctors. The law entrenched an inefficient, insurance-dominated health sector with massive subsidies flowing straight from the U.S. Treasury to insurance companies.

As a temporary pandemic measure, the American Rescue Plan Act further increased subsidies for this coverage from 2021 through 2022. It increased taxpayer assistance for exchange plans in two ways. First, it reduced what people with income between 100 and 400 percent of the federal poverty level (FPL) need to pay for a benchmark plan. Second, it lifted the cap on subsidy eligibility at 400 percent of FPL. The Inflation Reduction Act did not introduce any reforms in the market and continued the expanded subsidies—setting them to expire after 2025.

Here are the basic economics:

The ACA’s regulations increased premiums for the vast majority of people.

Subsidies were then needed so people could afford coverage that the government regulations made more expensive.

The underlying regulatory and subsidy structure leads to ever-escalating premiums and prices.

Higher premiums create pressure for still more subsidies, and those additional subsidies only worsen the underlying problems—fueling the very premiums and price escalation they are meant to offset.

If Congress wants to make health care more affordable, it must reform the structure itself, not throw more good taxpayer money after bad. In fact, the surest way to avoid meaningful reform would be to continue the pandemic-era subsidy boosts.

ACA Exacerbated Harmful Health Care Consolidation

In addition to driving premiums up through subsidy design, the ACA reshaped market structure in ways that reduced competition and locked in persistently high prices. The ACA’s regulatory and subsidy architecture helped institutionalize market concentration, reduced competitive discipline, and thereby reinforced rising costs rather than reversing them. According to Joel White’s November 6, 2025, testimony, many county-level exchange markets now have two insurers with at least 70 percent of enrollment, 97 percent of inpatient hospital markets lack meaningful competition, and uncompetitive hospital markets lead hospitals to increase prices 15 to 30 percent. Instead of competition driving costs down, consolidation on both sides created a stable high-price equilibrium in which neither hospitals nor insurers had incentives to reduce prices.

The Specific Damage from the ACA and the Enhanced Subsidies

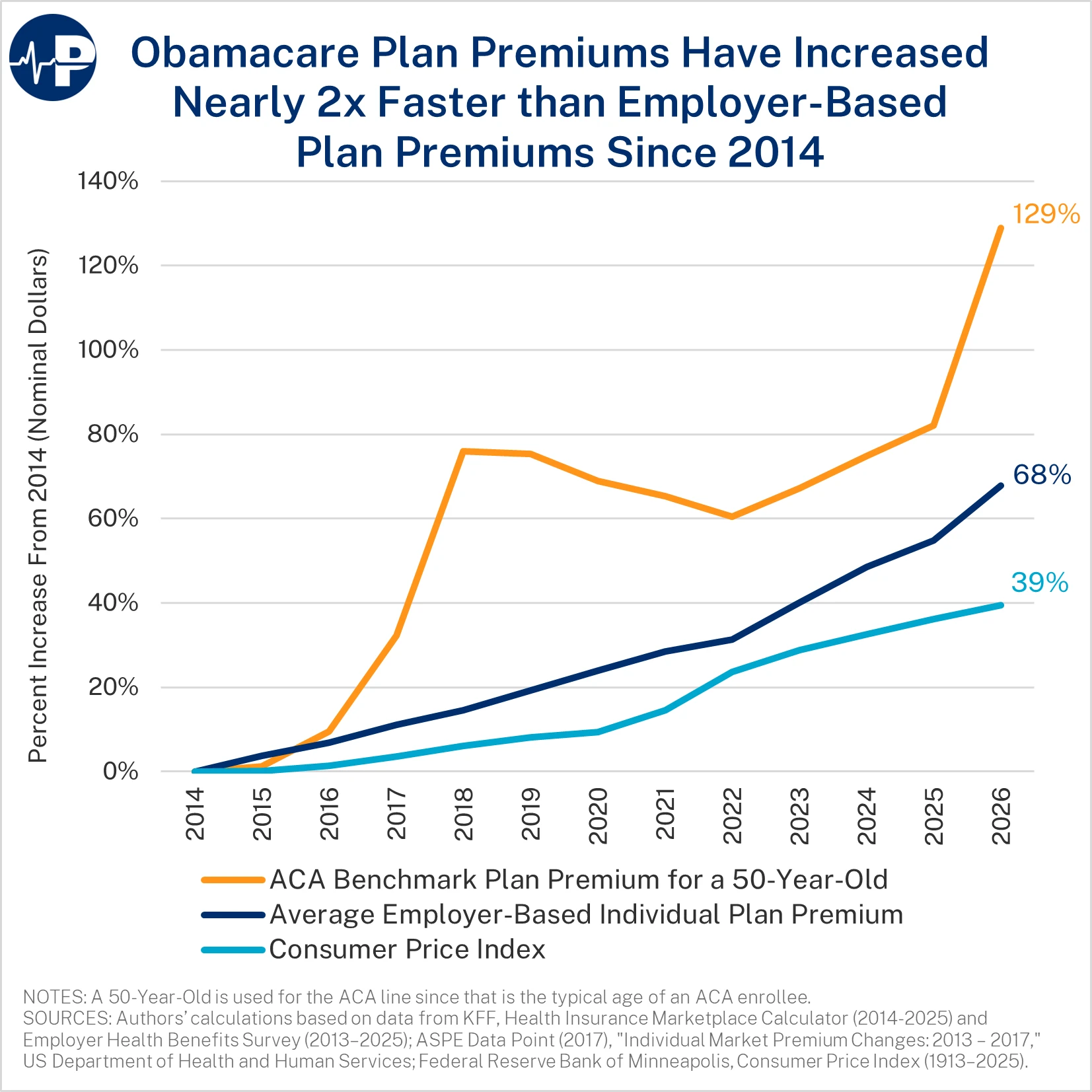

From 2014 to 2026, individual market premiums are up 129 percent, employer-sponsored insurance premiums are up 68 percent, and general inflation is up 39 percent. This is after individual market premiums increased nearly 50 percent from 2013 to 2014.

In 2026, the average deductible for an individual on a bronze plan is $7,476, and the average deductible for an individual on a silver (no CSR) plan is $5,304.

During the annual open enrollment period, applicants estimate their household income for the following year, often with the assistance of brokers or agents. Based on this reported income, the government sends monthly subsidies, dubbed advance premium tax credits, to the insurer offering the plan selected by the applicant. Almost all of the subsidies are direct payments from the Treasury to health insurance companies. In many cases, the insurer receives more money than the enrollee was lawfully entitled to during the year—and the insurer gets to keep the excess payments, with some combination of the federal taxpayer taking the loss and the enrollee being liable for a portion of the excess payment.

The Structural Failures of the ACA’s Subsidy Design

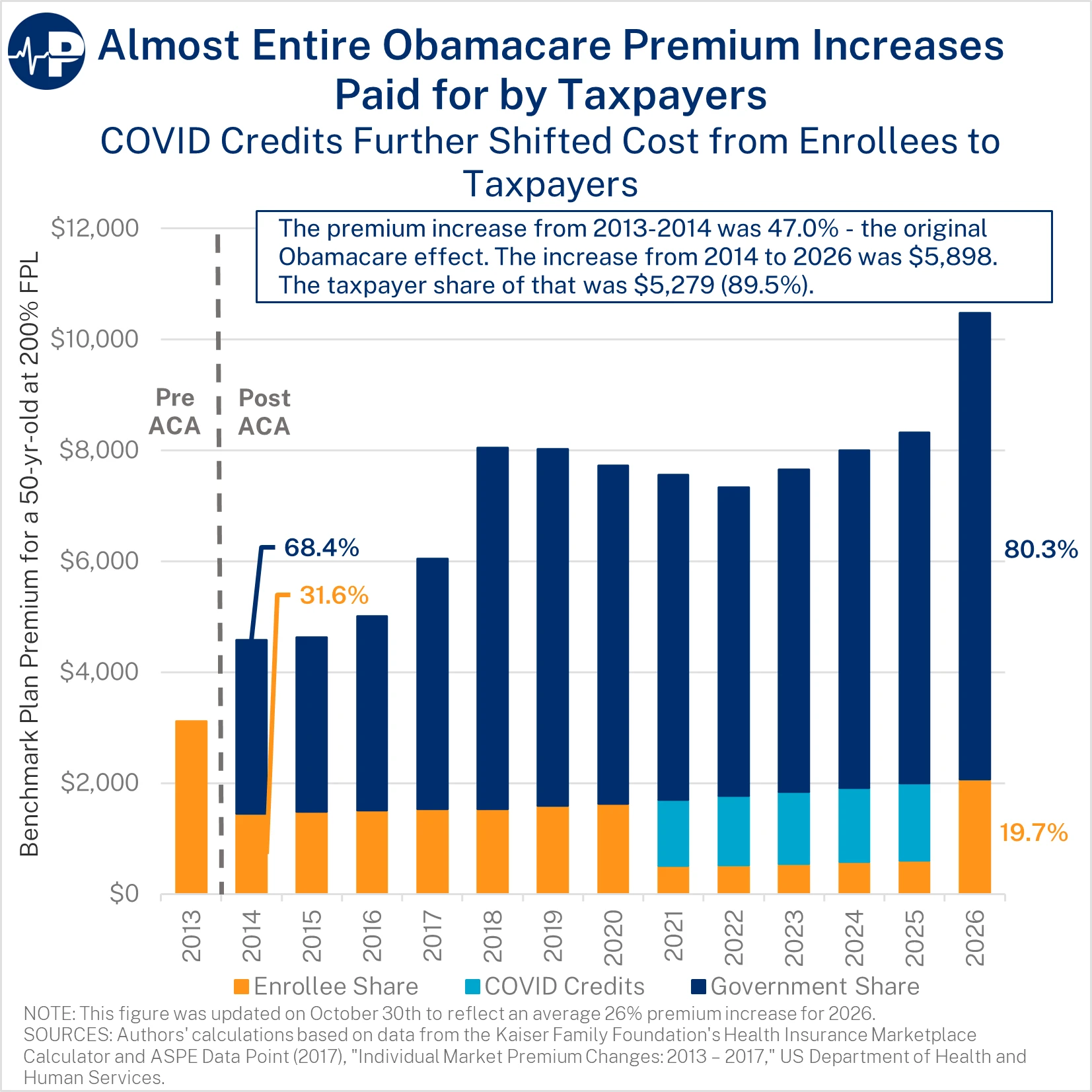

The ACA’s subsidies are ill-designed and inflationary in critical ways. The enrollee’s share of the premium is capped—regardless of the total premium. This structure is inherently different than other federal health programs, such as Medicare Part B and the Federal Employees Health Benefits Program, where enrollees pay a percentage of the premium. As premiums have dramatically increased over time, the federal taxpayer has borne almost the entire increase. The figure below demonstrates the increase in premiums and the split between taxpayer and enrollee from 2014 through 2026 for a 50-year-old enrollee at two times the FPL—about the average enrollee’s age and income.

The federal taxpayer share of the premium increased gradually from 68 percent of the premium in 2014 to nearly 80 percent in 2020. As a result of the COVID credits, the federal taxpayer share of the premium reached 93 percent from 2021 through 2025. Next year, when the COVID credits expire, the federal share will exceed 80 percent. Because enrollees pay only a small slice of the premium, insurers face virtually no price discipline—giving them incentives to inflate costs rather than improve value.

The ACA subsidy structure does not just fail to control costs—it actively rewards insurers for raising them. A recent analysis by the Joint Economic Committee shows that consumers capture only 34 percent of the benefit, with roughly two-thirds captured by insurers through higher premiums and inflated benchmark prices. This occurs because subsidies automatically increase as premiums rise, insulating insurers from competition and enabling them to absorb most of the subsidies rather than pass savings on to enrollees.

The ACA regulations drive higher costs. For example, the ACA’s essential health benefit mandates require all plans to cover the same set of services regardless of what consumers want or need. These rules increase wasteful spending and premiums.

The Insurer-Provider Alliance That Raises Prices

A second critical flaw is the ACA’s medical loss ratio, under which insurers must spend a minimum share of premium revenue on medical claims. In other words, to increase profits, insurers must have higher premiums. In reality, despite the claims of lobbyists, insurers, and health systems, they do not negotiate prices across the table from each other. Rather, they sit on the same side of the table, as both are incentivized to extract more dollars from employers, enrollees, and taxpayers.

The Rise of Improper, Zero-Claim, and Phantom Enrollment

Among the perverse incentives inherent to the enhanced subsidies is their enabling of fraud in the exchanges. The benefit of hindsight reveals that these premiums—particularly their creation of fully subsidized plans—encouraged enrollees, often at the behest of unscrupulous brokers, to improperly enroll in coverage with subsidies they are not entitled to. Many of those improperly enrolled do not even know about their coverage, as they are victims of fraud schemes designed to pocket commissions and subsidies. This is evidenced by the rising percentage of people who do not use their coverage at all, by government enforcement actions, and news stories.

Improper Enrollment Pressures Created by the COVID Credits

Enrollment in the exchanges was well below projections until the COVID-era subsidy boost. From 2015 to 2020, exchange enrollment averaged about 10–11 million people—about 60 percent below what the Congressional Budget Office (CBO) projected in May 2013 in its last analysis before the ACA’s provisions took effect. Enrollment did surge beginning in 2022, but much of the surge was from improper enrollment caused by Biden COVID credits and among people unaware of their coverage—along with a large increase in the number of enrollees who did not use the coverage.

CBO’s most recent ACA subsidy baseline projection is 91 percent above its 2021 projection over the 2026–2033 period. Continuing the COVID credits would result in about $40 billion in higher deficits annually over the next decade. This surge in spending reflects widespread fraud and administrative decisions that prioritized enrollment over eligibility verification.

COVID Credits Created Financial Incentives for Misreporting and Manipulation

COVID-era subsidy boosts resulted in fully subsidized coverage for people claiming income within a category—100 to 150 percent of FPL. In a June 2025 paper that I coauthored, we found the amount of improper enrollment grew substantially between 2024 and 2025 for those claiming income between 100 and 150 percent of FPL. The number of ineligible enrollees rose from an estimated 5.0 million to 6.4 million from 2024 to 2025. In total, 29 states had more sign-ups in this income category than the number of eligible individuals in the population, based on our conservative methodology for determining improper enrollment. In 15 states, there are more than twice as many enrollees in fully subsidized plans than are eligible. The estimated cost to taxpayers from this improper enrollment will likely exceed $27 billion in 2025 alone. Under more expansive assumptions, the number of ineligible enrollees in 2025 could reach as high as 7.1 million.

The enhanced subsidies led to massive fraud. This policy decision created strong financial incentives for applicants and those allegedly acting on their behalf to misstate income and enroll in this income category. In addition to the expanded subsidies, the Biden administration adopted policies that prioritized maximizing enrollment over verifying eligibility.

Fraud, Misrepresentation, and Unauthorized Enrollment Are Widespread

Fraudsters took advantage of these relaxed eligibility checks. Many enrollees were signed up without their knowledge or consent. A recent Bloomberg investigation highlighted how large-scale deception rings take advantage of these perverse incentives, with some enrollees being coached on how to fill out their applications to take advantage of the fully subsidized coverage and some unscrupulous brokers and agents just enrolling people without their consent. Tactics include misleading advertising promising cash benefits as well as unscrupulous lead generators and brokers enrolling people without their knowledge and switching applicants into plans without their consent. One former customer service worker at a large brokerage firm said, “Half the time they didn’t even know they were signing up for insurance.”

Insurers and their intermediaries benefit from this flawed structure. Brokers receive commissions for each enrollment, creating strong financial incentives to maximize sign-ups by any means necessary. And insurers receive monthly payments from the Treasury on behalf of many people unaware of their enrollment or with other coverage, with many of them automatically reenrolled from year to year.

The Centers for Medicare and Medicaid Services (CMS) received more than 200,000 complaints about unauthorized plan switches in 2024 alone. In 2025, the Department of Justice brought charges against insurance executives accused of defrauding taxpayers out of more than $160 million. In addition, a Florida-based brokerage executive pled guilty to a separate $133 million scheme that targeted homeless and mentally ill individuals to improperly enroll them in subsidized ACA plans.

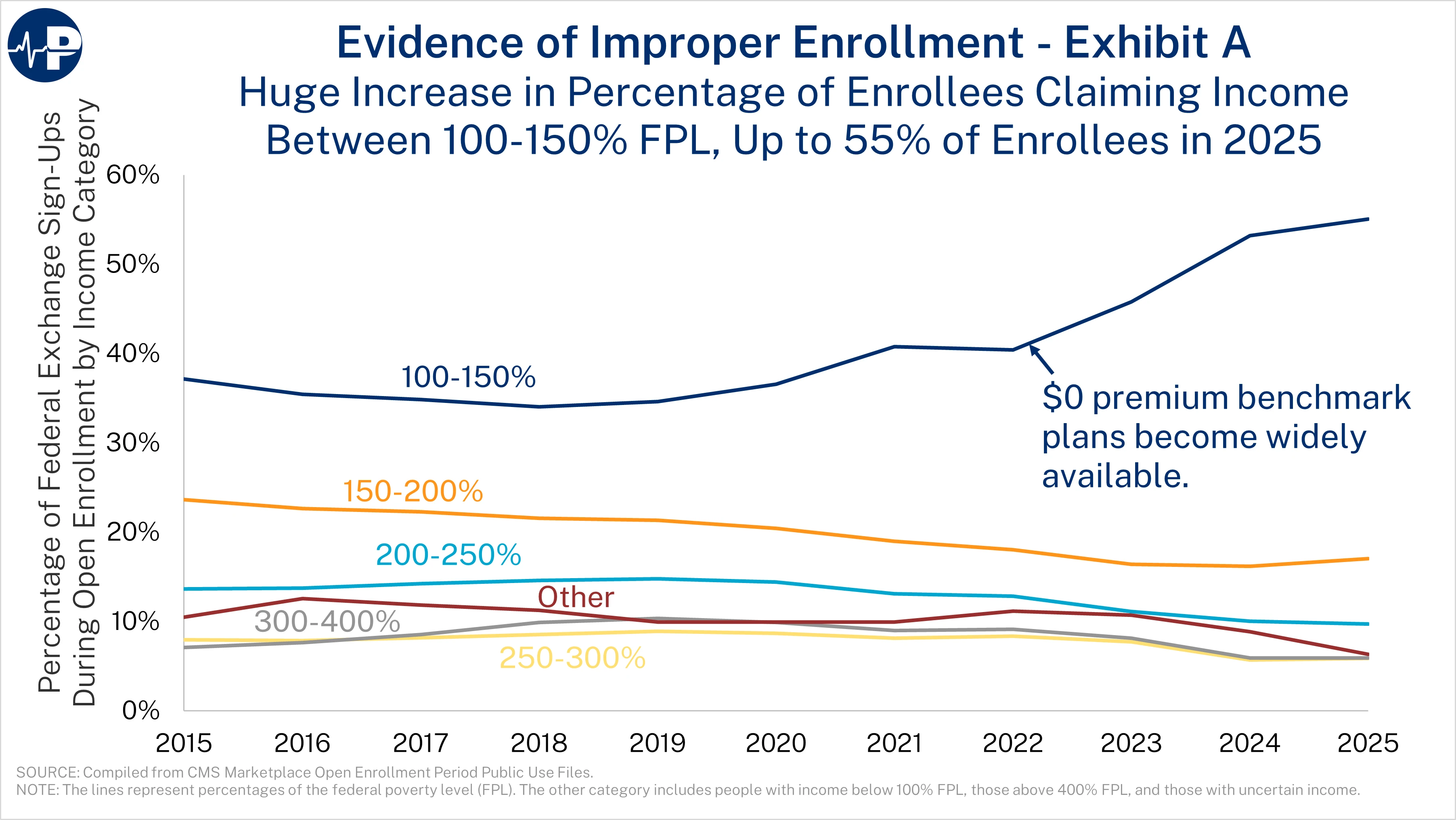

Four figures demonstrate the large scale of improper enrollment. The first figure shows the shift in overall enrollment to the lowest income category in the states that use HealthCare.gov. The first open enrollment period with fully subsidized plans was 2022. By 2025, a stunning 55 percent of people who signed up for coverage during open enrollment reported that their income was between 100 and 150 percent of FPL. This figure shows only the federal exchange sign-ups, because not all states with state-based exchanges reported sign-ups by income grouping prior to 2022. We estimate that 62 percent of individuals reporting income between 100 and 150 percent of FPL in HealthCare.gov states are not actually eligible, meaning that for every two eligible enrollees, there are more than three ineligible enrollees in this category.

Zero-Claim and Phantom Enrollment Has Exploded

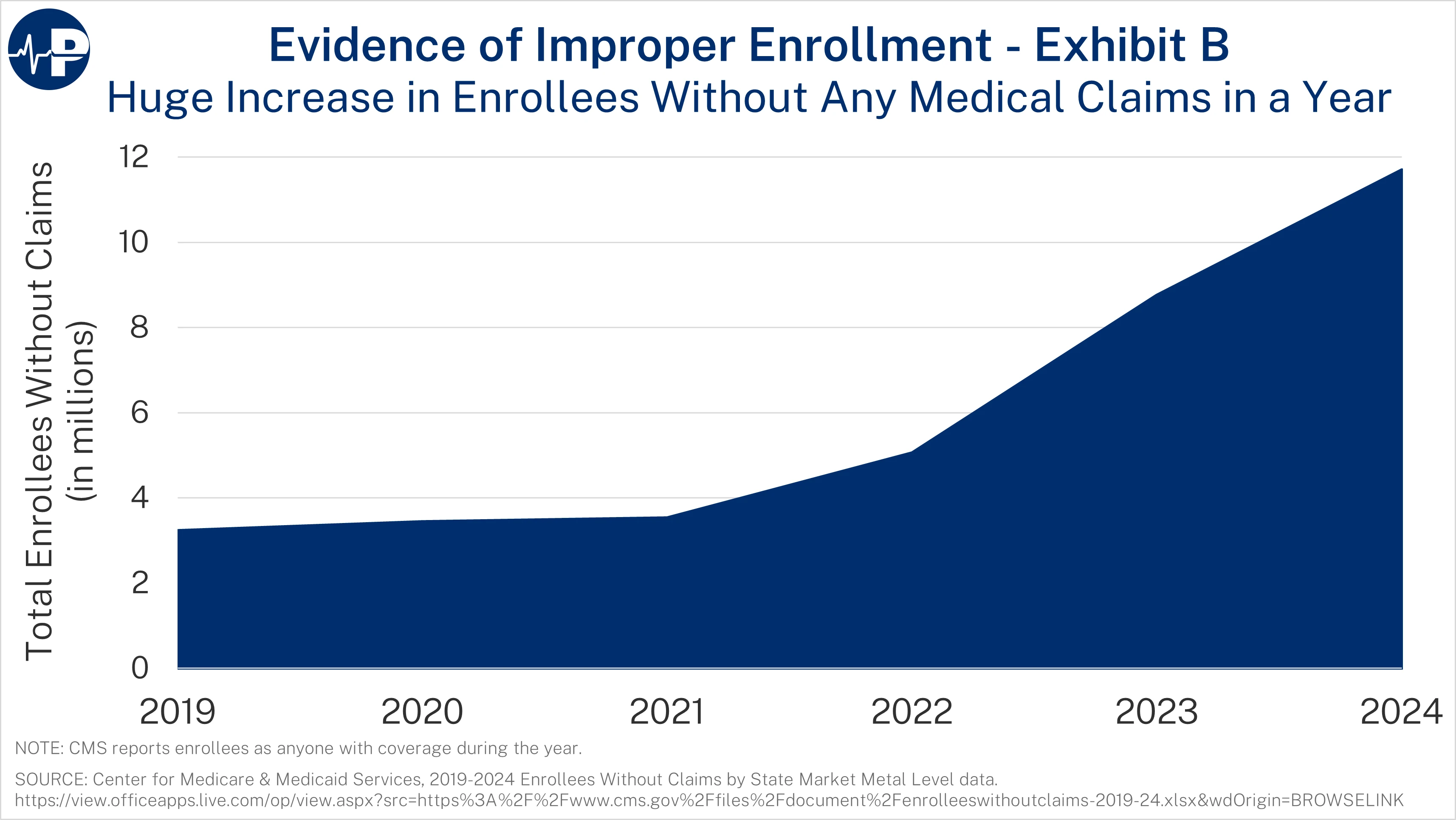

The next figure shows the explosive growth in zero-claim enrollees. From 2021 to 2024, the number of ACA exchange enrollees who did not use their plans for a single service tripled, reaching almost 12 million people. The zero-claim enrollment data include anyone enrolled during the year. Overall, 35 percent of enrollees did not use their plans a single time. A staggering 40 percent of fully subsidized enrollees used no medical services in 2024. These percentages are up from 19 and 20 percent, respectively, in 2021. Many of these zero-claim enrollees are “phantoms”—people who are unaware of their enrollment in the program or have duplicate coverage. Federal taxpayers sent more than $35 billion to insurers for people who did not use their plans a single time. In contrast, only 15 percent of people with private health insurance typically do not use their plans a single time. The fact that nearly 40 percent of fully subsidized enrollees used no services despite access to free preventive care further indicates that much of this enrollment is either improper or phantom rather than a genuine expansion of access.

The large growth in zero-claim enrollees has occurred even as most ACA insurers aggressively advertise that they offer free preventive services, including annual wellness checkups, mammograms, colonoscopies, and immunizations. Although the evidence strongly suggests large-scale improper and phantom enrollment, the alternative explanation is that coverage does not equate to care.

Meanwhile, yet another data study (see figure: “Obamacare enrollment: CMS vs CPS”), this one from Jeremy Nighohossian of the Competitive Enterprise Institute, is also suggestive of a surge of phantom enrollment in the ACA exchanges. According to Nighohossian’s review of federal data, twice as many people were enrolled in exchange plans in 2024 as reported having coverage, a much larger gap than in the years prior to the COVID credits.

Finally, as the next figures shows, in 2024 and 2025, the government did not have race or ethnicity data for more than half of ACA enrollees—a dramatic increase from 2021. This is yet another indication that many enrollees were likely signed up by agents or brokers who did not really know the applicant—obtaining only the minimum amount of information that was needed to get them enrolled in fully subsidized plans.

How the Enhanced Subsidies Harm Work, Productivity, and People with Employer Coverage

According to CBO, the enhanced ACA subsidies in the Inflation Reduction Act increase deficits, boost overall demand, reduce labor supply, and reduce long-run economic output. CBO made clear that the enhanced subsidies reduce labor supply by diminishing the financial returns to work. With fewer people working or working fewer hours, the economy’s productive capacity shrinks, leading to lower long-run output. The COVID credits, by lifting the subsidy cap at four times the FPL, encourage early retirement. It has led to situations such as a retired couple in their mid-50s—who earn $136,000 in pension income from government service—receiving $15,000 in ACA subsidies.

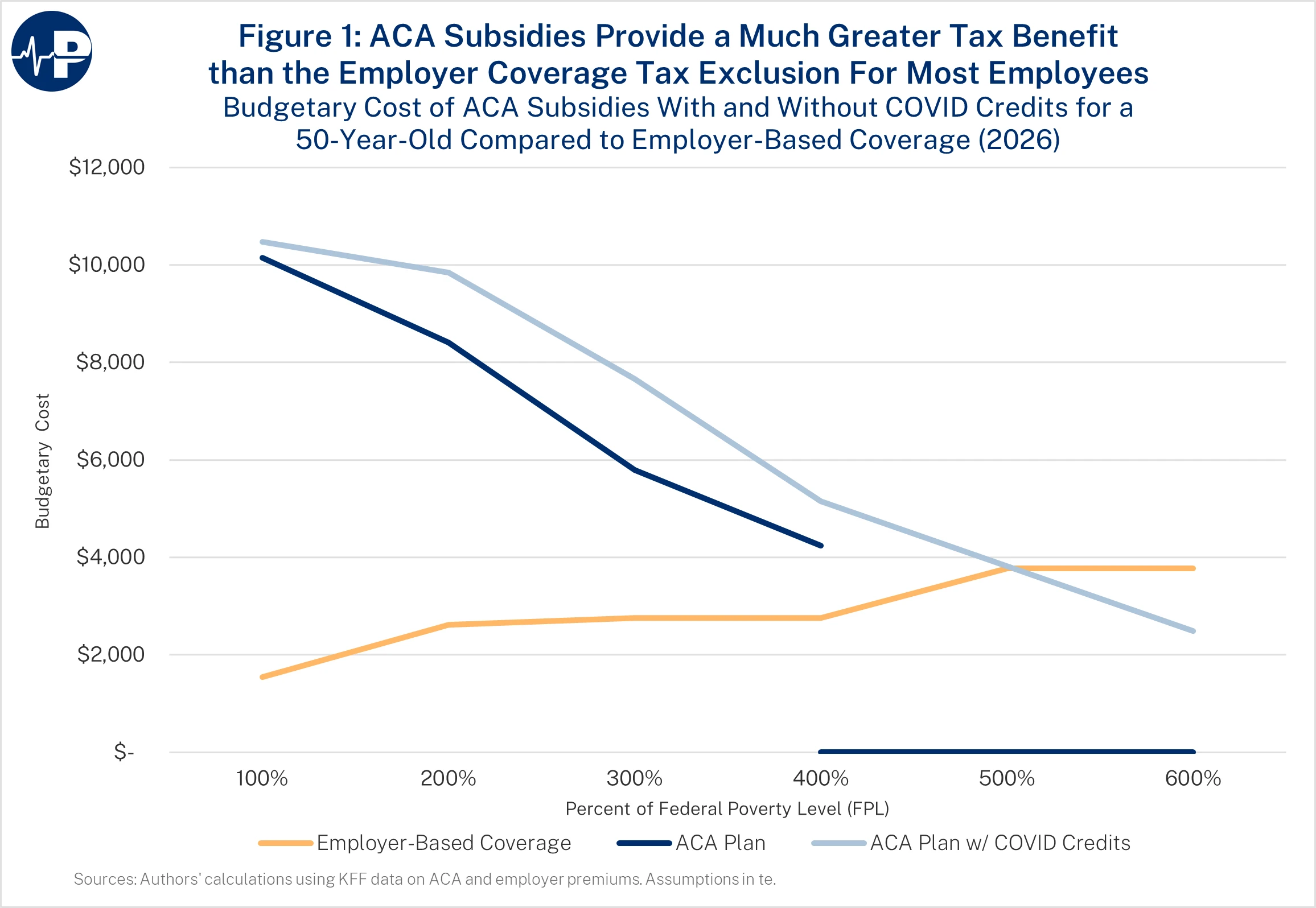

Moreover, the ACA’s subsidy structure, particularly with the COVID add-ons, incentivizes small employers to drop coverage. As the next figure shows, the benefit from receiving coverage from an employer is much lower than the benefit of the ACA subsidy for low- and middle-income enrollees. The tax benefit from receiving coverage through an employer is that the premium is not subject to income and payroll taxes. This subsidy design punishes work and penalizes employer-sponsored coverage (see figure: “ACA Subsidies Provide Much Greater Tax Benefit”). It creates a dramatic wedge between people who earn their benefits through employment and those who qualify for large, unearned tax credits—pressuring small employers to drop coverage and shifting millions into a more expensive federal program.

Obamacare is a cause of this problem: Notwithstanding the tax break for employer-sponsored benefits, Obamacare treats workers who earn their job-based benefits much more harshly than individuals who claim Obamacare’s unearned tax credits. Recent research from Paragon illustrates this effect.

Take a young family with 35-year-old parents and two children, ages 7 and 10 years. If the family’s income is $64,300 (200 percent of FPL), it will receive an original ACA subsidy of $19,059. The tax break for an employer-based health plan for the family would be only $5,904 (in a state with no income tax). The difference is a $13,155 net government benefit for not receiving coverage at work. However, if Congress extends the Biden COVID credits, the family’s subsidy would be $22,017, and the net government penalty for receiving coverage at work would increase to $16,113.

In addition, millions of people will likely lose workplace coverage. In fact, CBO projects that about 4.1 million people will replace employer-provided insurance or unsubsidized individual market insurance with subsidized exchange coverage if the COVID credits were made permanent.

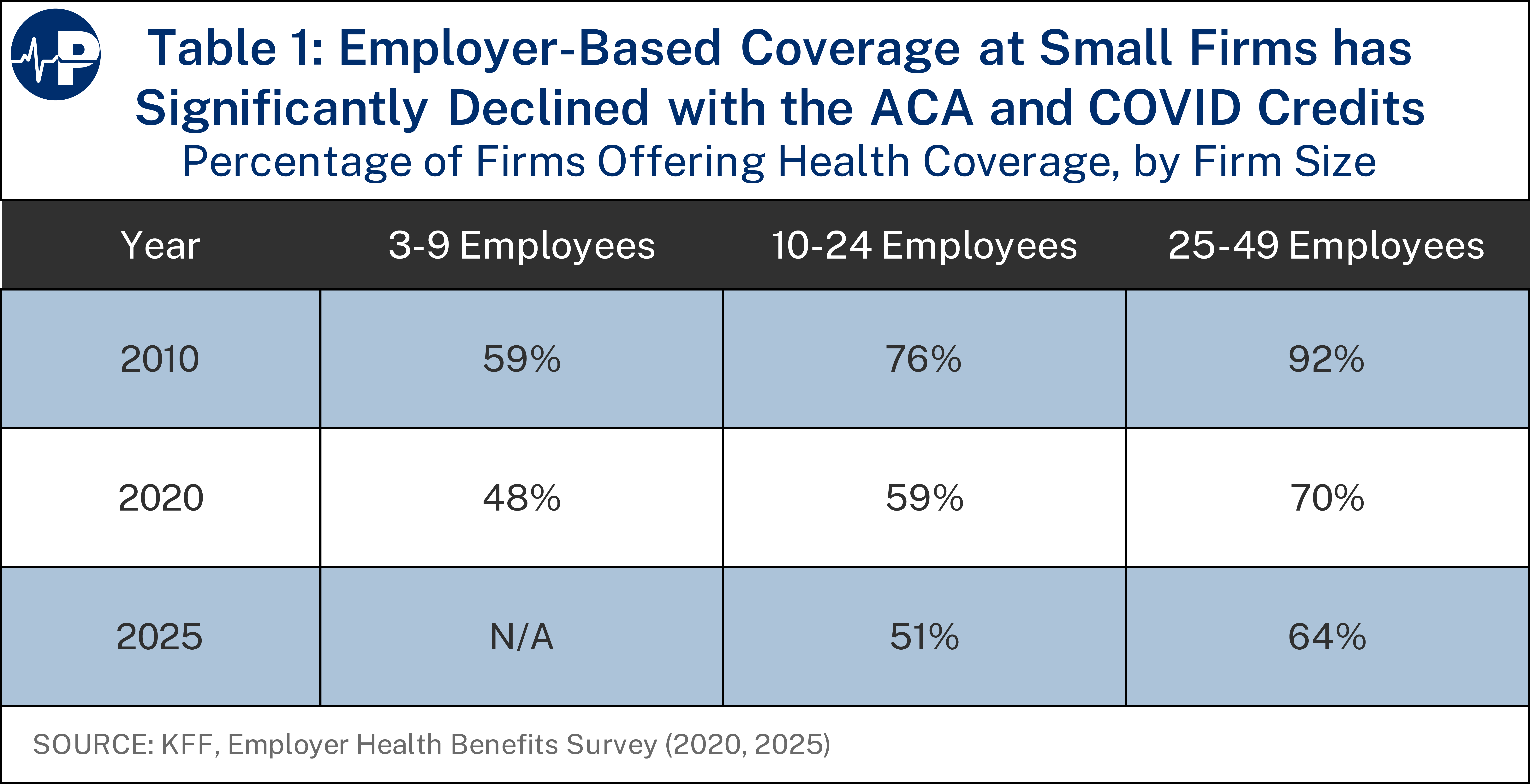

Although almost all large employers have continued to offer coverage, there has been a substantial decline in the percentage of small employers offering health plans. In fact, as the figure below shows, the percentage has dropped by about one-third since 2010. This leads to two concerns: (1) a growing taxpayer burden because of the expense of the ACA subsidies and (2) potentially worse coverage given the narrow networks of ACA plans. From a federal budget perspective, employer-sponsored health insurance is the least expensive option on average—only about one-third of the budgetary cost of the other main types of coverage for the non-elderly. According to CBO, in 2025, the average federal subsidy per enrollee under 65 is $2,553 for employer coverage, compared to a roughly $6,714 cost for Medicaid and Children’s Health Insurance Program (CHIP) enrollees and individual market exchange enrollees.

The ACA also led some state and local governments to drop retiree health coverage, offloading that expense onto the federal taxpayer. Many cities are offloading the cost of retiree health care by shifting retirees under the age of 65 to the exchanges, transferring the financial burden of local and state government obligations to federal taxpayers. If the COVID credits are extended, the offloading of this cost would accelerate.

Large Subsidies Remain, and Most Enrollees Would Pay Low Monthly Amounts

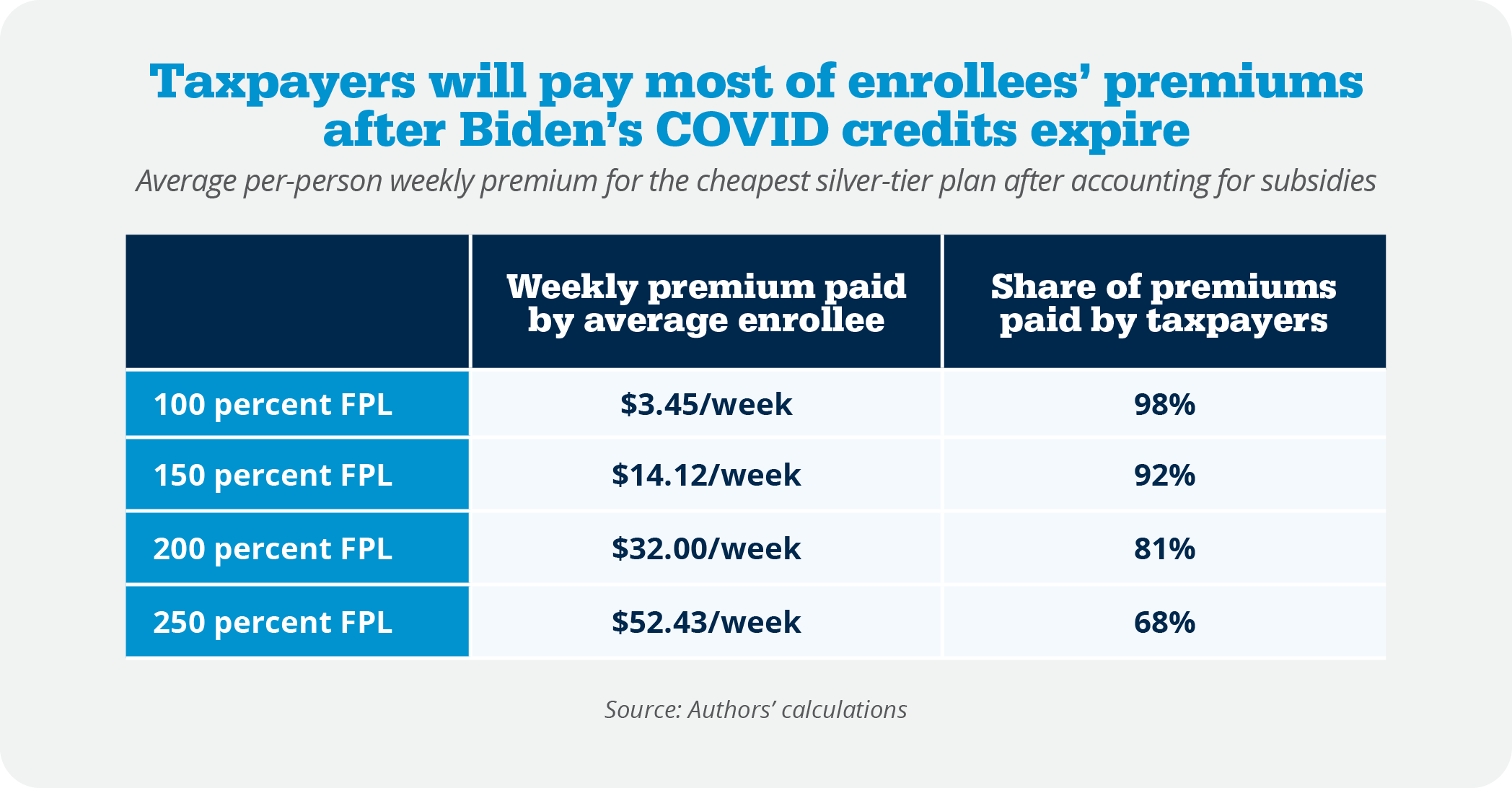

ACA premiums will rise next year because of underlying flaws with the program and growing cost pressures. Only a small portion of the increase is from the expiring COVID credits. As the next figure shows only 3.3 percent of the 2026 premium is from the expiration of the COVID credits.

The underlying ACA subsidy provides enormous protection for more than 93 percent of enrollees from high premiums. Most will pay less than $80 a month for a plan next year, with the federal taxpayers picking up 80 percent of the premium cost and a higher percentage for lower-income enrollees.

The table below shows the weekly premiums that enrollees would pay for the lowest-cost silver plans available to them. In 2025, 45 percent of exchange enrollees claimed income between 100 and 150 percent of FPL. Those enrollees would pay between $4 and $14 a week for silver plans next year. Another 20 percent of enrollees are between 150 and 200 percent of FPL and would need to pay up to $32 per week. Another 10 percent of enrollees are between 200 and 250 percent of FPL and would have to pay up to $52 a week for coverage.

Large ACA Subsidies Now Flow to Affluent Households

In areas of the country where exchange premiums are high, the expansion of the ACA subsidies leads to extremely high taxpayer subsidies for affluent households. For example, the benchmark premium for an exchange plan in Prescott, Arizona, for a family of five with a 60-year-old household head is $52,176 in 2025. A benchmark plan covers 70 percent of a household’s expected health care expenses on average. A $52,000 benchmark premium for a single family reflects a market that has fundamentally failed, not one offering exceptional value.

If that family made $150,000, it would qualify for a subsidy of $39,426.

If that family made $350,000, it would qualify for a subsidy of $22,426.

If that family made $500,000, it would qualify for a subsidy of $9,676.

The family does not lose subsidy eligibility until it earns about $614,000.

Insurers Getting Rich Off Over Subsidized Market

The subsidies go directly to health insurance companies, subsidizing their profits even though enrollees may place low value on the coverage and would prefer different health care and health coverage products. Of the premium revenue that insurers collect for selling exchange plans, more than 83 percent came from the Treasury in 2024. Insurers’ business models now revolve around securing federal subsidies rather than designing plans that consumers value. Insurers’ main client is now the federal government, which essentially ensures their revenue stream and guarantees them a profit. Insurer profits rose sharply during the period when pandemic-era subsidies expanded—not because coverage improved but because federal transfers increased dramatically. Both the design of the ACA’s premium subsidies as well as the ACA’s Medicaid expansion were inflationary and resulted in high payments to health insurance companies. There have been a variety of news stories documenting how these programs that are intended to benefit lower-income Americans have produced windfall profits for health insurance companies.

My Personal Experience with the ACA

In January 2021, my wife and I moved our family to Florida. For the previous 18 months, we had been using temporary continuation of coverage (the analogue to COBRA for federal workers) following my service at the White House. Shortly after arriving, I explored enrolling in an ACA individual market plan. I called several major providers to ask whether they accepted ACA coverage. Most flatly said they did not—several even equated ACA plans with Medicaid, saying their practices did not participate in those narrow networks. Fortunately, the Trump administration had expanded access to short-term, limited-duration plans. The short-term plan option cost roughly one-third the premium of an ACA plan with a similar deductible and offered a broader network of physicians. With five children, it was an obvious decision for us, and the coverage worked well for our family.

When I launched the Paragon Health Institute, we offered an individual coverage health reimbursement arrangement (ICHRA) so employees could use tax-preferred employer contributions to purchase ACA-compliant plans that met their needs. In fact, in the fall of 2020 I had written a paper for the Galen Institute arguing that the best way to maximize consumer control was precisely this model: employers funding a bronze plan and contributing to an employee’s health savings account (HSA). That structure allows people to choose their plans while shifting more resources into HSAs—the most effective tool for empowering consumers to be cost-conscious purchasers of care. Beginning in November 2021, my family enrolled in an ACA-compliant individual market plan through Paragon’s ICHRA.

Since then, I have seen and experienced firsthand the steadily rising premiums, climbing deductibles, and increasingly narrow networks that now characterize the ACA individual market. Like millions of Americans, my family is paying both premiums and deductibles with almost no meaningful return. Even this year, when my daughter broke her arm, nearly all expenses fell below the deductible, leaving us responsible for the full cost. Our current plan’s premium is projected to increase to $33,000 next year, paired with a deductible of nearly $14,000. It is extraordinarily unlikely that my family will incur $47,000 in health costs next year—yet that is the financial exposure the ACA imposes. These trends underscore the deep structural flaws of the ACA.

For the first time, Paragon is seriously considering whether we can continue offering an ICHRA, because individual market plans have become so unattractive. Paragon employees do not receive ACA subsidies or COVID credits, as we offer an ICHRA that precludes employee eligibility for ACA subsidies. As of the date of this testimony, we still do not know what we will do about providing employee coverage next year. This is deeply discouraging. My hope was that ICHRAs would help strengthen the individual market by broadening the risk pool and bringing more private dollars into it. We need a vibrant individual market—both to offer options for people without affordable workplace coverage and to support a consumer-driven alternative to the employer system. Instead, ACA-driven premium and deductible inflation is pushing organizations such as mine to reconsider remaining in that market at all. Paragon will continue offering a health plan, but other firms in this position have decided to drop coverage or will drop coverage—a decision that will be easier if the COVID credits are extended.

Principles for Reforming Federal Health Policy

In reforming federal programs that affect the demand side of the market, policymakers should be guided by five principles:

The policy should not increase federal subsidies for health care or insurance beyond the current law baseline. Excessive subsidies are driving the health care unaffordability crisis.

The policy should improve incentives. Current government policy incentivizes spending with other people’s money and, as a result, drives wasteful spending.

The policy should redirect existing subsidies away from insurers to people, so the health care system is more responsive to people and best meets their preferences.

The policy should expand coverage options for families and small businesses, not limit choices to those preferred by central planners and insurers looking to restrict competition. We need innovation in health care financing approaches to improve incentives for health care providers to be more efficient.

The policy should ensure that Americans are able to use their own money on the health coverage and health care that works best for them.

Policies to Lower ACA Premiums and Expand Patient Control

Affordability Idea No. 1: CSR Appropriation Fixes a Core ACA Distortion

The ACA contained two subsidy programs—one for premiums and one for out-of-pocket payments. The latter was called the cost-sharing reduction (CSR) subsidy. Exchange enrollees who selected silver plans are entitled to a CSR subsidy that reduces their plan deductibles, copayments, and plan out-of-pocket limits. In effect, the CSR subsidy raised the actuarial value (AV) of plans. The CSR subsidy was sent directly from the Treasury to insurers.

The ACA did not include a valid appropriation for the CSR program. A court ruled that the Obama administration made illegal CSR payments to insurers. The Trump administration complied with the courts and stopped the payments. In response, insurers who still had the CSR obligation significantly increased silver plan premiums. This raised the premium subsidy, which is based on the second-lowest-cost silver plan in an area. The termination of CSR payments, and insurers’ response of “silver-loading,” led to an overall increase in ACA subsidies and caused silver premiums for unsubsidized enrollees to soar.

A CSR appropriation would lower silver premiums by about 12 percent and would lower the overall subsidization of the ACA market—and thus deficits—by tens of billions of dollars. Even progressive health policy analysts suggest that a funded CSR program would increase the ACA’s efficiency for a given level of subsidization. A CSR appropriation is a true policy no-brainer that lowers ACA premiums and federal deficits and aligns the ACA with its original design.

Affordability Idea No. 2: The HSA Option Empowers Patients, Not Insurers

Building off a CSR appropriation, I coauthored a Paragon report in 2022 that proposed a reform to the ACA subsidy structure that we call the HSA Option. Rather than taking their CSR subsidy as insurer-controlled reductions in cost-sharing, eligible enrollees could instead choose to receive that subsidy as a deposit into an HSA. This approach puts money directly in patients’ hands and allows them to use the subsidy in the way that best meets their families’ needs.

HSAs expand patient control, improve flexibility, and create incentives to seek value in health care. HSA funds can be used for a far broader range of services than a typical health plan covers—dental, vision, mental health, over-the-counter items, and many services obtained outside narrow ACA networks. The funds roll over year after year, easing family cash flow, helping enrollees manage high deductibles, and better preparing households for future health care needs.

Our analysis, using modeling from Milliman, shows that nearly seven in 10 enrollees with incomes below 200 percent of FPL would benefit financially from selecting the HSA Option, gaining roughly $1,500 per year on average. More than three-quarters of those between 200 and 250 percent of FPL would also benefit, with average gains between $500 and $600.

Most importantly, the HSA Option shifts power away from insurers and back to patients—where it belongs—and allows lower-income Americans to choose the form of subsidy that provides them the greatest value.

Affordability Idea No. 3: Make HSAs More Flexible and Accessible

In a paper I coauthored in May 2024, “Follow the Money: How Tax Policy Shapes Health Care,” we included numerous additional reforms to expand the usability of HSAs. The paper highlights a major reform proposal to allow greater flexibility in AV requirements for health plans tied to HSAs. Currently, many HSA-eligible plans require very high deductibles and limit pre-deductible coverage, which restricts access for individuals with chronic conditions and reduces choice. By decoupling HSA eligibility from rigid deductible thresholds and linking it to a clear AV standard, policymakers could broaden HSA-qualified plan options and strengthen consumer choice. By permitting HSA-eligible plans that meet appropriate AV benchmarks—even if they deviate somewhat from current designs—consumers gain more control over how they use tax-advantaged dollars.

Affordability Idea No. 4: End the Inflationary Subsidy Structure

The inflationary subsidy structure needs reform as well. A key reform would be to fix the inflationary design of the ACA’s premium tax credit by capping the value of the benchmark plan used to calculate subsidies. Today, the federal subsidy is tied to the second-lowest-cost silver plan in each region, and an enrollee’s contribution is capped as a percentage of income. When benchmark premiums rise, federal subsidies rise dollar for dollar—shielding enrollees from costs and rewarding insurers with larger checks from the Treasury. In competitive regions, this problem is smaller, but in areas with limited insurer competition—or in states that impose expensive mandates—the design becomes highly inflationary.

Capping the benchmark at a fixed percentage of the national average premium (we proposed 125 percent of the average premium) would preserve reasonable geographic variation while preventing insurers or states from inflating benchmark premiums to extract larger subsidies.

Expand Coverage Options

There are ways to increase affordable health coverage without new federal spending. Many policies implemented by the previous Trump administration expanded affordable coverage options for employers and families without new federal spending.

These policies include:

- expanded coverage options through short-term limited duration plans and association health plans (AHPs);

- new flexible financing methods through individual coverage health reimbursement arrangements (ICHRAs)—which built off qualified small employer health reimbursement arrangements (QSEHRAs); and

- price transparency policies intended to improve the functioning and efficiency of health care markets.

Affordability Idea No. 5: Short-Term Health Plans Provide Affordable Alternatives

Short-term, limited-duration plans are dramatically more affordable than ACA exchange plans and typically offer far broader provider networks. These plans give families access to real medical choice rather than the narrow-network options that dominate the individual market today. When my family moved to Florida in 2021, we enrolled in a short-term plan, and it was unquestionably a better deal for us—lower premiums, lower deductibles, and far more providers who actually accepted the coverage. For many middle-class families who are ineligible for large ACA subsidies, short-term plans are often the only option that combines affordability with access to a wide network of doctors and hospitals. Short-term plans serve different consumers than ACA plans, and research shows they do not siphon away healthy enrollees and threaten the exchange risk pool.

Paragon’s research shows that expanding access to short-term plans not only benefits consumers directly but also strengthens the overall individual health insurance market. States that allowed short-term plans without restrictive limits between 2018 and 2023 experienced individual-market enrollment growth more than 13 times greater than states that heavily restricted them. Insurer participation in ACA exchanges also increased far more in these states, and premiums grew more slowly. In other words, the data clearly show that short-term plans do not harm the ACA risk pool. If anything, states with freer short-term plan markets saw better ACA market performance. The evidence demonstrates that permitting affordable alternatives improves consumer welfare without destabilizing the exchange market—and, in many cases, helps it function better.

Affordability Idea No. 6: Let Small Employers Form Association Health Plans

Employers—especially small employers—need additional options to provide affordable coverage to their workers. One such option is to permit employers to band together to offer coverage through AHPs. While AHPs have existed for decades, employers needed to have a close nexus in order to join together and offer coverage. For example, dental practices could form an AHP, but a dental practice and an auto mechanic shop in the same town could not.

In June 2018, the Department of Labor (DOL) finalized a rule creating a new pathway for any employer, including sole proprietors, within a state and or common metropolitan area to join together and offer coverage through an AHP. This rule provided smaller employers a way to gain the regulatory advantages and economies of scale that large employers receive when offering health insurance.

As discussed in a Washington Post piece from early 2019, the AHP expansion had a promising start, with most new AHPs launched by regional chambers of commerce. According to the Post, “there are initial signs the plans are offering generous benefits and premiums lower than can be found in the Obamacare marketplaces.” The Post wrote that an analysis of the new plans showed they offered benefits comparable to most workplace plans and did not discriminate against people with preexisting conditions. A study by the Foundation for Government Accountability found that new AHPs produced savings of 29 percent on average. One local chamber of commerce that enrolled hundreds of employers was projected to save policyholders more than $2,000 on average. CBO projected that these new AHPs would cover as many as 4 million people by 2023, half a million of whom would have been uninsured. Unfortunately, a March 2019 decision by a federal judge invalidated this new pathway. Although the Department of Justice appealed this decision and the appellate court heard arguments in November 2019, the court granted the Biden administration’s motion to pause the appeal while the DOL considers further agency action. The Biden administration then rescinded the 2018 rule.

Given the litigation challenges, congressional action may be necessary for businesses to benefit from a new AHP pathway. As projected by CBO, these new AHPs would help hundreds of thousands of businesses and millions of employees obtain more affordable health coverage and would reduce the number of uninsured. This increase in health coverage would involve no new federal spending. Congress should consider legislation that builds on the Trump administration’s 2018 regulation.

Affordability Idea No. 7: Unleash ICHRAs and QSEHRAs

In June 2019, the Department of Health and Human Services (HHS), DOL, and the Treasury issued a rule creating ICHRAs. Like AHPs, the idea behind ICHRAs should be bipartisan. They work within the ACA’s basic framework and could significantly increase individual market enrollment.

As of January 1, 2020, employers have been able to provide tax-preferred contributions through ICHRAs, which their employees can use to purchase the individual market plans that work best for them. Most employers that offer health insurance provide workers with only a single option, so the HRA rule has the potential to significantly increase worker choice and control over their health insurance. Employees are currently limited to purchasing ACA-compliant plans in the individual market, although Congress could permit employees to use their ICHRAs to purchase a broader set of plans.

Assuming there are attractive insurance products to purchase, ICHRAs would help employers attract and retain employees, gain greater predictability over their health costs, and reduce administrative expenses, allowing them to focus more on their core business. The rule should help reverse the decline in the number of small employers that offer coverage to their workers. Moreover, the rule contains significant flexibilities for larger employers to offer coverage to part-time workers or hourly workers.

According to estimates provided in the June 2019 rule, 800,000 employers would be offering ICHRAs by now with more than 11 million people receiving individual market coverage with an ICHRA. The Departments expected the rule to reduce the number of people without health insurance by about 1 million. According to the Department’s analysis, “Most of these newly insured individuals are expected to be low- and moderate-income workers in firms that currently do not offer a traditional group health plan.” Similar to AHPs, the increase in insured people through ICHRAs would involve no new federal spending.

ICHRAs have similarities to QSEHRAs, which Congress enacted on a bipartisan basis in 2016. QSEHRAs permit employers with no more than 50 full-time employees to reimburse individual market premiums. QSEHRAs have some limitations that do not apply to ICHRAs, such as setting an overall limit on the amount the employer can reimburse as well as a prohibition of creating classes of employees to vary benefit offerings. However, QSEHRAs represent a valuable coverage option for many small businesses and their employees.

Congress could codify the 2019 HRA rule to enhance employers’ certainty about the future of defined contribution health insurance. To date, ICHRA uptake has been significantly less than expected, with employers’ understandable focus on weathering the pandemic as well as a general risk aversion to changing employee benefits in a tight labor market. The main deterrents to ICHRA uptake are the general unattractiveness of individual market coverage, particularly the high premiums and deductibles, and the expanded ACA subsidies, which crowd out employer coverage.

Affordability Idea No. 8: Expand Price Transparency to Enable Market Discipline

In 2019, HHS finalized a rule requiring hospitals to post complete price information starting in 2021. In 2020, HHS with DOL and Treasury finalized a separate rule that requires health insurers and health plans to post complete price information starting this year (2026).

Price information can enable individual consumers as well as employers to be better shoppers of health care. Price information is particularly important in health care because it is a large part of the typical family’s budget and because there is significant variation in prices—with prices for the same service often varying by magnitudes, even within the same geographic area.

Although transparency is not the final goal, it is the prerequisite for a functioning market in which patients and employers can reward value rather than blindly pay high, opaque prices.

I analyzed these requirements and their potential impact in a 2019 report. Expanded price transparency should result in five benefits.

First, price transparency will encourage more consumers to shop and obtain lower prices.

Second, price transparency will help employers establish better payment structures. These payment structures include reference pricing models, in which the plan sets a payment rate regardless of which provider delivers the service, and which have been shown to generate significant savings.

Third, price transparency will better enable employers to monitor the effectiveness of their insurers by comparing different rates received by providers across payers and across regions.

Fourth, transparent prices should help employers eliminate counterproductive middlemen and contract with other entities that will incentivize employees to utilize lower-cost providers, including ones outside of their local regions.

Fifth, just as sunlight is often the best disinfectant, price transparency will better enable consumers and the broader public to hold providers accountable when prices reach outrageous levels.

The effectiveness of the price transparency efforts to date has been hindered by uneven compliance and enforcement. Congress could consider putting additional penalties on hospital systems and insurers that fail to comply with the requirements.

Affordability Idea No. 9: Expand Availability of Catastrophic Plans

The ACA arbitrarily restricted catastrophic plans—low-premium, high-deductible options designed to protect against major medical expenses—to people under age 30 or those with hardship exemptions, sharply limiting affordable choices for many adults who prefer this type of coverage. Recent federal guidance expanded eligibility beginning in 2026 by allowing people of any age who are ineligible for CSR subsidies to enroll in catastrophic plans. This modest step restores some choice, but Congress should go further and simply make catastrophic plans available to everyone, regardless of age or subsidy status, so individuals and families can choose the coverage that best fits their needs.

Disappointing Health Benefits from Government Coverage Expansion

While access to affordable health coverage and care are important, it is vital for policymakers to recognize two key facts: First, a large amount of medical spending is wasteful—with some of it even harmful to patients. Second, health insurance expansions, particularly through government programs such as Medicaid, tend to have disappointing results in terms of health improvements.

A significant concern with our high medical spending is that a large share of it—estimated by some researchers to be 25 percent of spending, as mentioned above—does not provide Americans with any benefit. In fact, some of that spending may instead harm our overall health. A 2016 study found that medical errors are the third leading cause of death in the United States, and as many as 250,000 people die each year from errors in hospitals and other health care facilities. Medical tests and treatments all carry some risk. Those that are unnecessary will result, on balance, in harm to patients.

The impact of health insurance on health is not as clear or as positive as commonly believed. At a macro level, despite the significant increase in health coverage beginning in 2014 as a result of the ACA, American life expectancy declined for three straight years from 2014 through 2017. The 2018 Economic Report of the President by the White House’s Council of Economic Advisers (CEA) put it this way:

[T]he evidence shows that health insurance provided through government expansions and the medical care it finances affect health less than is commonly believed. Determinants of health other than insurance and medical care—such as drug abuse, diet and physical activity leading to obesity, and smoking—have a tremendous impact and have exacerbated recent declines in life expectancy, despite the ACA’s increased coverage.

The CEA report evaluated numerous studies, including the two well-known health insurance experiments—the RAND health insurance experiment and Oregon’s Medicaid experiment—in its conclusion that expansions of government coverage produce negligible health benefits. They suggest at least four reasons why health insurance, through government coverage expansions, has a minimal effect on health.

According to the report, “The first three of these reasons—that the uninsured were often able to obtain care before coverage, access problems for patients who gain Medicaid coverage, and mandated insurance benefits that have a minimal impact on health—are particularly salient when examining the results of the ACA coverage expansion.”

The fourth reason raised by CEA is that “public coverage may have limited or possibly negative effects on health because of its long-run impact on innovation. Many governments, particularly in Europe, have paired large coverage expansions with the imposition of price and spending controls. These centralized controls may have an adverse impact on medical innovation and make healthcare less effective and more costly to obtain in the future.”

The lack of clear health benefits from the expansion of Medicaid, which I detailed in a report released in the spring of 2020, should raise policymakers’ concerns about additional subsidies that simply expand government spending on the current structure. I concluded that large coverage expansions disappoint for several reasons: The uninsured receive nearly 80 percent as much care as similar insured people, potentially superior private coverage is crowded out, and expansion has indirect effects on others such as longer wait times for care.

Other Government Policies That Are Inflationary

Medicaid Money Laundering and State-Directed Payments

State-directed payments (SDPs) are a growing and inflationary component of the Medicaid program. Under SDPs, states order Medicaid managed care plans to make extremely high payments to providers. In essence, states use legalized money-laundering schemes to obtain federal money without any actual state contributions to then provide corporate welfare for the politically powerful. The most recent analysis from the Medicaid and CHIP Payment Access Commission estimates that SDPs cost $110.2 billion in an 18-month period from February 2023 through August 2024. This was a 60 percent increase over the prior period—an explosive upward trajectory. As of this year, at least 30 states use SDPs.

SDPs create perverse incentives that limit access and increase costs for health care services in several ways. SDPs encourage consolidation by disproportionately benefiting large health systems, enabling them to buy up smaller providers. This reduced competition creates scarcity that, in turn, allows large providers to command higher prices.

The Biden administration issued a regulation that permits SDPs so that the total Medicaid payment can equal average commercial rates. Average commercial rates are more than 2.5 times Medicare rates nationally, meaning that Medicaid is now a much better payer than Medicare in many states. Moreover, by tying Medicaid rates to commercial rates, there is an incentive to increase those rates in order to raise government payments through Medicaid. Thus, the inflationary spiral harms both taxpayers and people with private plans. The Working Families Tax Cut Act limited payment rates through SDPs to at, or about, Medicare rates beginning in 2028—taking a giant step toward reducing corporate welfare in Medicaid.

Medicare Site of Service Payment Differentials

Medicare often pays different rates for the same procedure depending on where that procedure is performed. Payment rates can vary depending on if the patient is treated in a hospital, an ambulatory surgical center, or a physician’s office. For example, in 2016, Medicare paid on average 60 percent as much to an ambulatory surgical center and 45 percent as much to a physician’s office as it paid to a hospital outpatient department (HOPD) for the same procedure. Site-specific payment policies also apply to an off-campus HOPD, which is often not located on the same grounds as the main hospital. Various policy actions from both Congress and CMS over the past decade have sought to reduce site-specific differentials. If site-neutral payment policies were applied to most services for all off-campus and on-campus HOPDs, CBO projects savings of $157 billion over 10 years.

Site-specific payments steer patients to more expensive settings, increasing spending and distorting the market. In Medicare, these differentials increase Part B premiums and cost-sharing for beneficiaries, as well as costs to the taxpayer. In addition, site-specific payments increase costs across the health system. Private payers frequently adopt rates based on Medicare’s payment policies, so these differentials push up payments in the commercial market, too.

Site-specific payments also undermine the competitive landscape and choices of care available to patients. Because off-campus HOPDs receive higher hospital payment rates, site-specific payments encourage hospitals to buy independent, free-standing physician offices and convert them into off-campus HOPDs—a move that increases consolidation and ultimately raises prices and spending. Site-neutral payment reforms have enjoyed bipartisan support, as evidenced by the panel hosted by Paragon last year featuring scholars from the American Enterprise Institute, the Brookings Institution, the Center for American Progress, and former HHS secretaries Kathleen Sebelius and Alex Azar with uniform views on the wisdom of moving to site-neutral payments in Medicare.

340B

The 340B Drug Pricing Program is the second-largest drug-pricing program in the country behind Medicare Part D and will eclipse Part D in a few years based on the current trajectory. The program requires pharmaceutical manufacturers to offer discounts on qualifying outpatient drugs to specified “safety-net” hospitals and other federal health entities (namely federally qualified health centers, among others) in exchange for being allowed to participate in Medicare and Medicaid. Due to severe program opacity, the size of individual discounts is not publicly known, though estimates range from 22.5 to 50 percent of a drug’s average sales price. In 2023, total 340B spending had grown to over $66.3 billion annually, equivalent to 14.7 percent of annual prescription drug spending in the United States.

The 340B program directly contributes to higher health care spending. CBO has found that 340B has increased government and private sector drug spending as well as incentivized health care consolidation. Because 340B allows all sub-entities of participating hospitals (known as “child sites”) to receive 340B discounts, hospitals have strong incentives to buy up independent physician offices to capture their patients and divert resources into new off-campus HOPDs and other child sites in wealthier areas. One study found that a higher concentration of 340B participants in a market is associated with higher ACA premiums and more than $2 billion in additional annual federal ACA subsidy spending. The program results in the use of higher-priced drugs, greater drug volume, and lower biosimilar uptake. The program is intended to help hospitals that are true safety nets for the needy, but the structure of the program directs most aid to wealthier entities and communities.

Physician-Owned Hospitals Limitation

The ACA imposed major restrictions on physician-owned hospitals (POHs) by amending the Stark Law to bar new POHs from participating in Medicare. Existing physician-owned facilities were allowed to continue but were barred from expanding their capacity without a complex exception process. These ACA changes effectively froze the growth of POHs. Prior to the ACA, they had been expanding and specializing rapidly—accounting for more than 200 facilities nationwide. Proponents of the restriction, including the American Hospital Association, argued that physician ownership created conflicts of interest, encouraging overutilization of services (known as “self-referral”). The Physician Hospitals of America contend that these facilities delivered higher-quality care at lower costs due to aligned incentives and operational efficiency.

The ACA’s restrictions on POHs drive higher health care prices by limiting competition and preserving market dominance for large, non-physician-owned hospital systems. POHs have historically operated with Medicare costs 1 to 20 percent lower per case than their peers due to streamlined administration, lower overhead, and stronger incentives to avoid unnecessary procedures. This lack of competitive pressure reduces incentives for efficiency across the system.

For example, a 2020 study in Health Affairs found that patients treated in physician-owned medical practices incurred 5.8 to 6.3 percent lower annual spending compared to those in hospital-owned practices, with competitive spillover effects encouraging neighboring facilities to reduce unnecessary services and overhead.

Growth in Complexity

Annual federal health spending now exceeds $1.9 trillion across Medicare, Medicaid, and the ACA exchanges. This spending is more than twice national defense, and with it has come waves of regulations directing that spending and attempting to ensure that it is used as intended. At the same time, thousands of pages of regulations seek to engineer outcomes, using payment rates to incentivize providers and patients to take certain actions. Private insurers often follow this lead, even though they should have more incentives for cost control using utilization management and anti-fraud practices. With government spending comes extensive regulation—and complexity that forces providers to spend more time on paperwork instead of patients and to hire administrators instead of clinicians.

Spending on health care administration totals approximately $1 trillion a year and represents roughly 17 percent of total national health expenditures. Not only does increased complexity result in greater direct spending; it also influences spending indirectly by its impact on consolidation. Although larger providers can generally dedicate resources to handle the burdens of administrative complexity, smaller providers struggle to keep up. The burden on small providers has fallen hardest on independent physicians, who have resorted to selling their practices to larger health systems. Between 2007 and 2017, the percentage of physician practices owned by hospitals or health systems grew more than 20 percentage points. As of 2024, nearly half of physicians are employed by other entities—mostly hospitals and health systems—rather than being independently employed, an increase from less than 30 percent in 2012. This increased consolidation has resulted in higher prices for patients. One study found that a 10 percent increase in hospital system market share is associated with a $880–$1,880 higher negotiated rate per admission.

Certificate of Need Laws

Certificate of need (CON) laws are state-level policies that were originally intended to curb health care costs. Yet they have the opposite effect by preventing competition and discouraging innovation. CON laws require providers to justify to regulators the need for investments in new technology, services, or facilities. These laws were originally encouraged by a federal policy that threatened states with funding cuts if they lacked CON requirements—a policy that has since been repealed. However, 38 states and Washington, D.C., continue to enforce CON or CON-like laws.

It is estimated that CON laws raise the per capita cost of health care services by 10.5 percent. CON laws most often apply to nursing homes, psychiatric services, and hospitals—the areas facing the greatest shortages. Costs for services in these areas continue to rise as demand, particularly in rural communities, outpaces supply. CON laws also promote consolidation by denying new services where they already exist through other providers. This is exacerbated by the employees of incumbent providers who often sit on CON boards and deny applications from would-be competitors. This entrenches monopolies and their market power over prices in those areas. Recognizing the ill effects of CON, the Rural Health Transformation Program—authorized through the Working Families Tax Cuts Act—provides a key federal incentive for states to repeal their CON laws in order to receive increased funding to invest in their communities.

Scope of Practice Limitations

State scope-of-practice limits for non-physician medical professionals often place arbitrary barriers on practitioners who could serve underserved communities. Physicians are constrained by private credentialing boards and professional organizations. By contrast, non-physicians face many similar credentialing requirements but are often subject to stricter limits despite being trained to do more. Many states have taken recent steps to roll back portions of their scope-of-practice limitations in order to better meet the needs of their residents, particularly in rural areas.

Scope-of-practice laws raise costs by creating shortages, duplicating services, and reinforcing provider monopolies. Requiring patients to see physicians for treatments that nurse practitioners, physician assistants, or pharmacists are trained to provide forces them into higher-cost care settings. Scope-of-practice laws also lead to duplicative payments when an initial evaluation by a non-physician must be followed by a second visit with a physician solely to satisfy regulatory rules. Beyond limiting access, these policies are anti-competitive, preserving physicians’ control over services that would otherwise face competition and enabling higher prices without corresponding improvements in care.

Conclusion: Reform Requires Incentives, Not More Spending

Renowned health economist and Harvard Business School professor Regina Herzlinger has written that “choice supports competition, competition fuels innovation, and innovation is the only way to make things better and cheaper.” Unfortunately, government policies—despite good intentions—often stifle choice, competition, and innovation in health care. Furthermore, these programs and policies produce incentives that lead to waste rather than value in our health care expenditures:

Government mandates have pushed up the price of insurance. The high price of insurance necessitates large subsidies so people can afford the coverage.

Government restricts people from buying coverage that works best for them and prevents small employers from joining together to gain the same advantages that large employers obtain in their coverage.

Government contributes to higher health care prices and overall inflation with poorly designed subsidies.

More subsidies are not a remedy for unaffordable health care—they are the accelerant that fuels higher premiums and deeper market dysfunction. Expanding subsidies entrenches a system in which premiums rise faster, competition weakens further, and taxpayers finance an ever-growing transfer to insurers. The only path to genuine affordability is structural reform that restores price discipline, aligns incentives, and shifts power from insurers to patients.

The ACA’s poorly designed subsidy structure has funneled hundreds of billions of dollars to insurers while doing little to improve health outcomes. A sustainable solution requires letting the temporary COVID-era enhanced subsidies expire, appropriating CSRs, replacing the inflationary benchmark formula, and giving lower-income families the option to receive their cost-sharing subsidies as deposits into HSAs. These reforms would redirect dollars away from insurers and toward patients, strengthen market discipline, and meaningfully improve affordability without increasing federal spending.

Fortunately, by reforming existing government programs and pursuing policies that promote choice and competition in health care, policymakers can expand access to affordable health coverage without new government spending.

The following policies, if fully implemented, would help millions of families and reduce the number of uninsured by a projected 2 million people—all without any new federal spending:

AHPs offer significant savings to small employers for high-quality coverage.

ICHRAs allow employers to provide health coverage in ways that some employees may prefer.

Short-term health plans represent more affordable and attractive coverage for some individuals and families.

In addition to the expansion of coverage opportunities, new price transparency rules that are properly implemented can improve the functioning of health care markets and expand opportunities for consumers and employers to maximize value from their expenditures.

Lastly, policymakers should avoid centralized regulatory or price controls that would diminish health care innovation. Rather, policymakers should create a climate conducive to innovation in which entrepreneurs are best serving patient needs.

Thank you for the opportunity to testify before the committee today, and I look forward to your questions.