What GAO Found

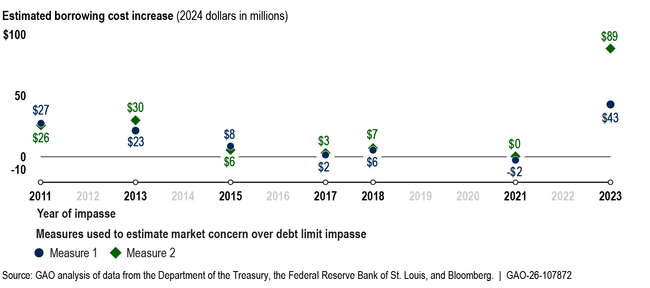

Debt limit impasses impose avoidable costs. As a projected date nears when the U.S. will be unable to meet all its financial obligations—the X date—investors often demand higher yields on new Treasury securities maturing near that date to compensate for the added risk. This increases the government’s borrowing costs. GAO estimates that Treasury securities issued during periods of acute market concern over impasses between 2011 and 2023—the most recent impasses with complete data available at the time of GAO’s analysis—incurred a total of roughly $107 million to $161 million in increased immediate borrowing costs (in 2024 dollars), depending on the measure used to estimate market concern. Impasses also impose additional, hard-to-quantify costs, including long-term costs from reduced investor confidence in the Treasury market.

Estimated Immediate Treasury Borrowing Costs Associated with Debt Limit Impasses

Note: For each impasse, GAO used two distinct measures of market concern to estimate increased borrowing costs. For more details, see fig. 2 in GAO-26-107872.

Debt limit impasses have also reduced the market value of outstanding Treasury securities. Market participants avoided securities maturing near a projected X-date, as those maturing after this date would be the first to default if the impasse were not resolved in time. GAO’s analysis found that these securities lost value relative to comparable ones maturing just before the X-date.

Impasse disruptions to Treasury markets can spread to short-term funding markets and funds closely tied to Treasury securities. In 2011 and 2013, such disruptions included higher borrowing rates and money market fund outflows. These disruptions prompted market participant actions to limit risk and manage future impasse effects. However, other disruptions can occur after impasses are resolved, as fluctuations in the Department of the Treasury’s cash balance create volatility in some markets.

GAO’s prior work has identified longstanding concerns about the debt limit (GAO-25-107089). The current debt limit process creates an unnecessary risk of U.S. default, with potentially devastating consequences for individuals, financial institutions, and the broader economy. The costs and market disruptions documented in this report further underscore the need for debt limit reform.

Why GAO Did This Study

Congress imposes a legal limit on federal borrowing, known as the debt limit. Under the current process, Congress can approve spending increases or tax cuts without also ensuring that Treasury has sufficient borrowing authority to finance these decisions. In recent years, when the federal government has approached the debt limit, prolonged congressional negotiations on increasing or suspending the limit have repeatedly brought it close to being unable to continue paying obligations stemming from past spending and revenue decisions. If Treasury exhausts its borrowing authority and runs out of cash, a default will occur.

In this report, GAO examines how debt limit impasses—where outstanding debt reached the limit and Congress did not immediately raise or suspend it—between 2011 and 2023 affected Treasury’s borrowing costs and U.S. financial markets more broadly.

GAO analyzed financial market data and developed a suite of econometric models to estimate increased borrowing costs attributable to these impasses. GAO also reviewed relevant research, documentation, and laws. In addition, GAO interviewed agency officials and 17 financial market participants, selected to reflect a range of institution types and sizes.