Europe Luxury Fashion Market Size

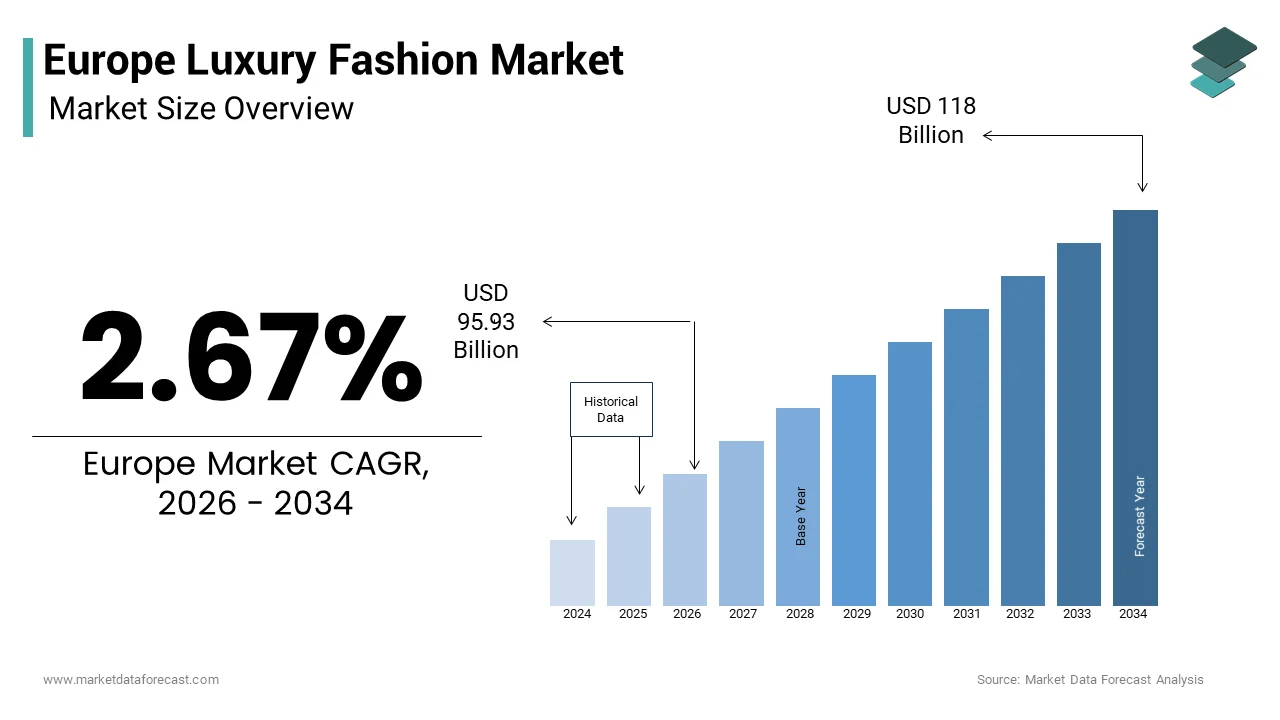

The Europe luxury fashion market size was valued at USD 93.42 billion in 2025 and is anticipated to reach USD 95.93 billion in 2026 to reach USD 118 billion by 2034, growing at a CAGR of 2.67% during the forecast period from 2026 to 2034.

Current Introduction Europe Luxury Fashion Market

The luxury fashion is the apex of the global apparel and accessories industry, defined by exclusivity, superior craftsmanship, heritage branding, and premium pricing strategies that transcend mere utility. This sector encompasses high-end ready-to-wear, leather goods, footwear, jewelry, and watches produced by historic houses and contemporary avant-garde designers primarily located in France, Italy, the United Kingdom, and Germany. The definition has evolved to include not just physical products but an entire ecosystem of experiential retail, digital storytelling, and sustainable ethics that resonate with the modern affluent consumer. Europe serves as the historical and operational heart of this industry, hosting the headquarters of major conglomerates like LVMH, Kering, and Richemont. According to Eurostat, the European Union recorded over 530 million international tourist arrivals in 2023, a significant portion of whom engage in luxury shopping as a core component of their travel experience, particularly in cities like Paris, Milan, and London. Furthermore, the European Commission notes that the creative and cultural industries contribute approximately 4% to the EU GDP, with luxury fashion being a dominant sub-sector driving exports and employment. The market is characterized by a rigorous adherence to quality standards, often protected by geographical indications such as “Made in Italy” or “Made in France,” which guarantee specific production methods. As per the European Environment Agency, there is an increasing regulatory push towards circularity, forcing luxury brands to redefine their value proposition through durability and repairability rather than just novelty.

MARKET DRIVERS

Resurgence of High-Net-Worth Individual Demographics and Wealth Concentration

The significant expansion of the high-net-worth individual (HNWI) population and the concentration of wealth within the region, which is elevating the growth of Europe luxury fashion market. Despite global economic fluctuations, the number of individuals with investable assets exceeding 1 million USD in Europe has shown resilience and growth, creating a robust customer base with high disposable income. According to the Capgemini World Wealth Report, the HNWI population in Europe grew by 5.2% in 2023, outpacing population growth and generating substantial liquidity for luxury consumption. This demographic shift is not limited to traditional old money but includes a surge in younger entrepreneurs and tech executives who view luxury fashion as a symbol of success and social capital. Data from UBS indicates that the under-40 demographic now accounts for nearly 35% of luxury spending in Western Europe, a figure that has doubled over the last decade. These consumers are less price-sensitive and more driven by brand narrative, exclusivity, and limited-edition releases. Furthermore, the inheritance wave expected over the next two decades, often termed the “great wealth transfer,” is poised to inject trillions of euros into the hands of younger generations who are already acculturated to luxury lifestyles. Statistics from the European Central Bank reveal that household savings rates in key markets like Germany and France remain historically high, providing a financial buffer that supports discretionary spending on premium fashion even during periods of inflation.

Integration of Digital Omnichannel Experiences and Social Commerce

The sophisticated integration of digital omnichannel experiences and the rise of social commerce, which has democratized access while maintaining an aura of exclusivity is fuelling the growth of Europe luxury fashion market. European luxury brands have moved beyond simple e-commerce transactions to create immersive digital ecosystems that blend online convenience with the tactile allure of physical boutiques. The adoption of augmented reality (AR) for virtual try-ons, live-streamed fashion shows, and personalized AI-driven styling services has significantly enhanced customer engagement. As per recent survey, European luxury consumers have made a purchase after interacting with a brand on social media platforms like Instagram or TikTok, highlighting the power of visual storytelling. Brands are leveraging these platforms to launch “digital-first” collections and non-fungible token (NFT) linked physical items, appealing to tech-savvy collectors. Furthermore, the seamless integration of inventory systems allows clients to browse online and reserve items for private in-store appointments, a service known as “click and collect”.

MARKET RESTRAINTS

Stringent Environmental Regulations and Sustainability Compliance Costs

The implementation of rigorous environmental regulations by imposing heavy compliance burdens and operational complexities on manufacturers. The EU Strategy for Sustainable and Circular Textiles introduces strict requirements for product durability, recyclability, and the use of recycled fibers, compelling brands to overhaul their supply chains and production processes. According to the European Commission, the upcoming Digital Product Passport will mandate detailed tracking of every garment’s lifecycle, from raw material sourcing to end-of-life disposal, requiring immense investment in data infrastructure and transparency. Furthermore, restrictions on the use of certain chemicals in leather tanning and dyeing processes, enforced under the REACH regulation, limit the palette of materials available to designers and force costly reformulations. Data from the European Environmental Bureau indicates that non-compliance can result in severe fines and reputational damage, deterring rapid innovation and market entry for niche players. The pressure to achieve carbon neutrality by 2050 forces companies to divert resources from marketing and expansion to sustainability initiatives, potentially slowing overall market growth.

Economic Volatility and Inflationary Pressure on Discretionary Spending

Economic volatility and persistent inflationary by eroding consumer confidence and altering spending priorities among the aspirational middle class is additionally impeding the growth of Europe luxury fashion market. While the ultra-wealthy remain insulated, the broader base of luxury consumers, including millennials and Gen Z who drive significant volume, are highly sensitive to macroeconomic conditions. The consumer confidence indices have dipped to historic lows in major economies like Germany and Italy, correlating with a noticeable contraction in voluntary spending on non-essential high-value items. The rising interest rates aimed at curbing inflation have also increased the cost of borrowing, affecting both consumer financing options for luxury purchases and the capital availability for brand expansions. Additionally, the uncertainty surrounding global trade relations and energy costs exacerbates supply chain expenses, forcing brands to raise retail prices which further dampens demand.

MARKET OPPORTUNITIES

Expansion of the Pre-Owned and Circular Luxury Economy

The rapid expansion of the pre-owned and circular luxury economy, driven by shifting consumer values towards sustainability and value retention is solely to set up new opportunities for the expansion of the Europe luxury fashion market. European consumers are increasingly viewing second-hand luxury not as a compromise but as a smart, ethical, and stylish choice by creating a burgeoning market for authenticated vintage and resale items. The trend is fueled by the desire for unique, discontinued pieces and the financial logic of investing in assets that hold or appreciate in value. Brands to capitalize on this by launching their own certified resale platforms and buy-back programs, thereby controlling the secondary market narrative and fostering deeper customer loyalty. Furthermore, the integration of blockchain technology for authentication ensures trust and transparency, addressing the primary concern of counterfeit goods in the resale sector. By embracing circularity, luxury houses can extend the lifecycle of their products, generate recurring revenue streams from the same item, and align with the EU’s circular economy action plan. This strategic pivot not only mitigates environmental impact but also opens access to a younger, price-sensitive demographic that aspires to own luxury but finds entry-level new prices prohibitive.

Personalization Through Artificial Intelligence and Bespoke Services

The integration of artificial intelligence (AI) to deliver hyper-personalization and bespoke services to enhance customer exclusivity and engagement is additionally to escalate the growth of Europe luxury fashion market. In an era where mass production is common, the ability to offer tailored experiences and customized products distinguishes true luxury brands. The high appreciation for craftsmanship and individuality, is particularly receptive to AI-driven personalization that suggests styles based on purchase history, body measurements, and lifestyle preferences. Opportunities exist in developing algorithms that predict micro-trends for specific client clusters, allowing for limited-run productions that feel exclusive. Furthermore, AI can facilitate virtual co-creation sessions where clients design their own handbags or shoes in real-time with a digital artisan, bridging the gap between digital convenience and artisanal touch. This level of customization fosters an emotional connection and reduces return rates, as products are inherently suited to the buyer.

MARKET CHALLENGES

Proliferation of Counterfeit Goods and Intellectual Property Theft

The proliferation of counterfeit goods and intellectual property theft to the integrity and profitability, undermining brand equity and consumer trust is a particular challenging factor for the growth of Europe luxury fashion market. The high desirability and premium pricing of European luxury brands make them prime targets for counterfeiters who produce sophisticated imitations that are increasingly difficult to distinguish from authentic items. These fake products not only divert revenue but also damage brand reputation when consumers associate poor quality or unethical production practices with the original label. The challenge is exacerbated by the complexity of global supply chains, where counterfeit components can infiltrate legitimate production lines. Combating this requires significant investment in advanced authentication technologies, such as NFC chips and blockchain tracking, as well as extensive legal actions across multiple jurisdictions. The erosion of exclusivity due to the widespread availability of fakes dilutes the brand’s allure, making it difficult to justify premium pricing. Furthermore, the psychological impact on consumers who fear purchasing fakes can lead to hesitation and reduced engagement with digital channels, stifling market growth.

Supply Chain Fragility and Scarcity of Artisanal Talent

Supply chain fragility and the scarcity of artisanal talent that threatens the production capacity and quality standards is additionally to restrict the growth of Europe luxury fashion market. The industry relies heavily on specialized skills passed down through generations, such as leather crafting, embroidery, and tailoring, yet there is a growing shortage of young people entering these trades. According to the European Centre for the Development of Vocational Training, the average age of skilled artisans in the European luxury sector is rising, with the workforce approaching retirement age and insufficient apprenticeship programs to replace them. This demographic cliff risks creating a bottleneck in production, limiting the ability of brands to meet growing global demand. Furthermore, the supply chain for raw materials like high-grade leather, cashmere, and silk is vulnerable to climate change, geopolitical tensions, and animal welfare regulations, leading to volatility in availability and cost. The concentration of manufacturing in specific regions like Northern Italy and France also exposes the sector to localized disruptions, such as energy shortages or labor strikes. Navigating this talent and resource crisis requires substantial investment in vocational training and supply chain diversification, which is capital-intensive and time-consuming, posing a long-term threat to the scalability and consistency of European luxury fashion.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

2.67% |

|

Segments Covered |

By Product, Consumer Group, Distributional Channel, Country |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, the Czech Republic, and the Rest of Europe |

|

Market Leaders Profiled |

LVMH (FR), Kering (FR), Hermes (FR), Chanel (FR), Gucci (IT), Prada (IT), Burberry (GB), Dior (FR), Versace (IT), Fendi (IT) |

SEGMENTAL ANALYSIS

By Product Insights

The accessories segment was the largest by holding 42.8% of the Europe luxury fashion market share in 2025 with the “lipstick effect” phenomenon where consumers opt for smaller, more affordable luxury items during economic uncertainty, and the high margin potential of leather goods and jewelry. The strategic positioning of handbags and small leather goods as entry-level products that allow aspirational consumers to access prestigious brands without the high cost of ready-to-wear collections. Data indicates that handbags account for over 35% of total personal luxury goods sales in Europe, with waitlists for iconic models from brands like Hermès and Chanel extending beyond 12 months, according to industry retail analytics. This scarcity creates immense desire and ensures consistent revenue streams regardless of broader economic fluctuations. Statistics from resale platforms reveal that luxury handbags have outperformed the S&P 500 in terms of value retention over the last decade, attracting a new demographic of investor-collectors. Furthermore, accessories are less susceptible to sizing issues and seasonal trend volatility compared to clothing, making them ideal for both physical and digital retail channels.

The footwear segment is projected to register a fastest CAGR of 7.8% during the forecast period due to the convergence of high fashion with streetwear culture and the rising demand for luxury sneakers. The growth of the segment is also driven by the shift in consumer lifestyle preferences towards comfort and versatility, blurring the lines between formal and casual attire. The innovation in materials and customization options, where brands offer bespoke sneaker services and utilize sustainable, high-tech fabrics that resonate with eco-conscious consumers is also escalating the growth of the segment. Additionally, the rise of “athleisure” has expanded the usage occasions for luxury footwear beyond the gym to daily wear, increasing replacement cycles and volume sales. The combination of cultural relevance, technological innovation, and broad demographic appeal positions footwear as the most dynamic growth engine in the European luxury landscape.

By Consumer Group Insights

The women segment was the largest by holding 58.3% of the Europe luxury fashion market, share in 2025 with the historical depth of women’s fashion offerings, the sheer variety of product categories available, and the higher frequency of purchase cycles among female consumers. The extensive ecosystem of women’s luxury goods, which spans from haute couture and ready-to-wear to a vast array of accessories, jewelry, and beauty products by creating multiple touchpoints for spending. Research indicates that women contribute to over 70% of all luxury purchasing decisions in households, often buying not only for themselves but also influencing gifts for partners and family members according to consumer behavior studies. The emotional connection women forge with brands through storytelling, heritage, and community engagement further solidifies their loyalty. The robust influence of female-centric marketing and the proliferation of female icons and ambassadors who shape trends and drive desire is also propelling the growth of the segment. Furthermore, the expansion of size inclusivity and diverse representation in recent years has opened up new market segments within the female demographic, encouraging participation from previously underserved groups. The enduring power of women’s fashion weeks in Paris, Milan, and London also keeps the segment at the forefront of global attention, ensuring continuous demand and innovation.

The men segment is swiftly emerging at a CAGR of 8.5% during the forecast period with the evolving definition of masculinity, the rise of male grooming and fashion consciousness, and the increasing disposable income among young professional men. The dissolution of traditional gender norms in fashion, encouraging men to experiment with colors, patterns, and accessories that were once considered exclusively feminine. The influence of male influencers and celebrities on platforms like Instagram and TikTok has normalized high-fashion consumption among men, providing style inspiration and reducing the stigma around vanity. The second factor is the growing importance of business casual and smart-casual dress codes in the corporate world, which has created a demand for high-quality, branded separates that bridge the gap between formal suits and streetwear.

By Distribution Channel Insights

The store-based retail segment was the largest by holding a dominant share of the Europe luxury fashion market in 2025 due to the tactile nature of luxury goods, the need for personalized service, and the role of boutiques as brand temples. The consumer expectation of an immersive, multisensory experience that online channels cannot fully replicate, including private viewing rooms, expert styling advice, and immediate product possession is majorly boosting the growth of the segment. As per the study, 75% of high-net-worth individuals in Europe prefer to make significant luxury purchases in-store to verify quality, craftsmanship, and fit before committing to high price points according to luxury consumer surveys. Furthermore, flagship stores in key cities like Paris, London, and Milan serve as marketing tools themselves, reinforcing brand prestige and acting as destinations for tourists. The integration of advanced technologies within physical stores, such as augmented reality mirrors, RFID-enabled fitting rooms, and clienteling apps that empower sales associates to provide hyper-personalized recommendations is additionally fuelling the growth of the segment. The ability to host exclusive events, launches, and VIP gatherings within these spaces fosters a sense of community and exclusivity that drives loyalty.

The non-store based segment is likely to register a fastest CAGR of 12.4% in the coming years with the increasing digital fluency of luxury consumers, the refinement of online shopping experiences, and the seamless integration of omnichannel services. The development of sophisticated digital platforms that offer virtual try-ons, 360-degree product views, and AI-driven personal shoppers, effectively mitigating the traditional barriers of buying luxury online. Additionally, the rise of social commerce allows consumers to discover and purchase items directly through social media platforms, shortening the path to purchase and capitalizing on impulse buys driven by influencer content. The second factor is the adoption of “click and collect” and “reserve online, try in-store” models that blend the convenience of digital browsing with the assurance of physical verification.

COUNTRY-LEVEL ANALYSIS

France Luxury Fashion Market Analysis

France was the largest contributor in the Europe luxury fashion market by holding 28.4% of the Europe luxury fashion market share in 2025 with its role as the global headquarters for the world’s largest luxury conglomerates, including LVMH and Kering, and its unparalleled reputation as the capital of haute couture. The deep-rooted heritage of French craftsmanship and the “Made in France” label, which serves as a global benchmark for quality and exclusivity by attracting millions of international tourists annually. The strong government support for the creative industries, including tax incentives for artisans and protections for geographical indications that preserve traditional techniques is also escalating the growth of the market. The presence of iconic avenues like the Champs-Élysées and Rue Saint-Honoré provides a concentrated hub for flagship stores that generate immense foot traffic and brand visibility. Furthermore, the French consumer’s innate appreciation for aesthetics and style ensures a robust domestic market that values heritage brands.

Italy Luxury Fashion Market Analysis

Italy secures the second-largest position in the Europe luxury fashion market with 24.4% of share in 2025 with its historic dominance in leather goods, textiles, and manufacturing excellence. The dense network of artisanal districts in regions like Tuscany, Lombardy, and Veneto, where family-owned businesses have perfected their crafts over centuries. Reports show that Italy exports over 60% of its luxury fashion production, with brands like Gucci, Prada, and Armani serving as ambassadors of Italian style on the global stage according to the Italian National Fashion Chamber. The integration of luxury fashion with Italy’s thriving tourism sector, where cities like Milan, Florence, and Rome act as magnets for fashion-focused travel. Milan Fashion Week remains one of the “Big Four” global events, drawing buyers, press, and celebrities who stimulate local retail activity. Additionally, the strong collaboration between brands and local artisans ensures a steady supply of high-quality materials and components, maintaining the integrity of the supply chain.

United Kingdom Luxury Fashion Market Analysis

The United Kingdom luxury fashion market growth is likely to have a significant growth opportunities in coming years with its unique blend of traditional tailoring heritage and cutting-edge contemporary design. The high concentration of ultra-high-net-worth individuals in London, who drive demand for exclusive, limited-edition pieces and personalized services is also fuelling the growth of market. The city’s vibrant cultural scene, including art fairs and royal events, provides numerous occasions for luxury consumption. Furthermore, the UK’s advanced digital infrastructure supports a thriving e-commerce sector for luxury goods, with British consumers being among the earliest adopters of online luxury shopping in Europe.

Germany Luxury Fashion Market Analysis

Germany luxury fashion market growth is driving with the pragmatic yet affluent consumer base that values quality, durability, and understated elegance over overt branding. The robust economy and high disposable income levels in regions like Bavaria and Hamburg, which support a steady demand for premium automotive-linked fashion and high-performance outdoor luxury wear. The strategic location of Germany as a central hub for European tourism, with cities like Munich, Berlin, and Düsseldorf attracting wealthy visitors from across the continent and beyond. The presence of high-end department stores like KaDeWe and Galeries Lafayette provides curated environments that cater to discerning tastes. Additionally, the growing awareness of sustainability among German consumers is pushing brands to adopt transparent supply chains and eco-friendly practices, with those meeting these criteria seeing higher engagement.

Spain Luxury Fashion Market Analysis

Spain luxury fashion market growth is driven with a vibrant and rapidly evolving player in the Europe luxury fashion landscape driven by a strong domestic textile industry and a booming tourism sector. The market status is marked by a lively consumer culture that embraces fashion as a form of social expression, with a particular affinity for leather goods, footwear, and resort wear. The success of homegrown luxury giants like Inditex (owner of Massimo Dutti and Uterqüe) and Puig, which have cultivated a strong local appreciation for Spanish design and quality. Spanish consumers are increasingly confident in domestic brands, driving a shift towards locally produced luxury items. Furthermore, the Mediterranean lifestyle promotes a year-round demand for stylish, versatile clothing suitable for both urban and leisure settings.

COMPETITIVE LANDSCAPE

The competition in the Europe luxury fashion market is intensely fierce characterized by a strategic battle between massive conglomerates and independent heritage houses for dominance in brand prestige and customer loyalty. Global giants leverage their extensive financial resources to acquire niche brands and secure prime retail locations in key cities like Paris and Milan. However, independent players differentiate themselves through unparalleled craftsmanship and exclusive scarcity models that appeal to discerning collectors. The market sees constant innovation in digital engagement as brands vie for the attention of younger demographics through social media and virtual experiences. Price competition is minimal since brand equity drives value but rivalry exists in securing top creative talent and sustainable raw materials.

KEY MARKET PLAYERS

A few of the market players that are in the Europe luxury fashion market are

- LVMH (FR)

- Kering (FR)

- Hermes (FR)

- Chanel (FR)

- Gucci (IT)

- Prada (IT)

- Burberry (GB)

- Dior (FR)

- Versace (IT)

- Fendi (IT)

Top Players In The Market

- LVMH Moët Hennessy Louis Vuitton stands as the undisputed global leader in the luxury sector, originating from France and defining the standards of exclusivity worldwide. The conglomerate contributes significantly to the global market by managing a vast portfolio of over seventy prestigious brands ranging from fashion to wines and spirits. Recently, LVMH has strengthened its European position by investing heavily in vertical integration, acquiring specialized tanneries and textile manufacturers to secure supply chains for its leather goods division. The company actively expands its retail footprint through the renovation of historic flagship stores in Paris and London to offer immersive brand experiences. LVMH also pioneers sustainability initiatives like the Life 360 program to reduce environmental impact across its operations.

- Kering SA operates as a powerhouse in the Europe luxury fashion market, renowned for its house of iconic brands including Gucci, Saint Laurent, and Bottega Veneta. The company drives global trends by championing creative innovation and sustainable luxury practices that resonate with modern consumers. Kering recently bolstered its market stance by implementing a rigorous sustainability strategy aimed at reducing its environmental footprint by 40% within the next decade. The group focuses on direct-to-consumer strategies, minimizing wholesale dependencies to better control brand image and pricing power across European capitals. Kering actively invests in digital transformation, utilizing artificial intelligence to optimize inventory and enhance online customer journeys. Furthermore, the company supports emerging designers through foundations and awards, fostering a pipeline of fresh talent.

- Hermès International maintains a unique and revered position in the Europe luxury fashion market through its unwavering commitment to artisanal craftsmanship and family-owned governance. The company contributes globally by setting the benchmark for quality and scarcity, particularly in its legendary leather goods and silk accessories which often appreciate in value. Hermès recently strengthened its presence by opening new manufacturing workshops in France to increase production capacity while strictly adhering to its handmade traditions. The brand avoids mass marketing, relying instead on exclusive client relationships and waitlists to drive demand and maintain an aura of unattainability. Hermès continues to invest in real estate, acquiring prime locations in major European cities to expand its boutique network without diluting brand exclusivity. The company also emphasizes vertical integration by owning its supply chain from raw materials to retail, ensuring total quality control.

Top Strategies Used By Key Market Participants

Key players in the Europe luxury fashion market primarily focus on vertical integration to control entire supply chains from raw material sourcing to final retail distribution ensuring quality and exclusivity. Companies heavily invest in digital transformation by developing sophisticated e-commerce platforms and utilizing artificial intelligence for personalized client experiences. Major participants prioritize sustainability initiatives by adopting circular economy principles and transparent sourcing to meet evolving consumer expectations and regulatory requirements. Firms also expand their direct-to-consumer networks by renovating flagship stores and reducing reliance on third-party wholesalers to maintain brand equity. Additionally, brands leverage limited edition releases and exclusive collaborations to generate hype and maintain high demand among affluent customers. These strategies collectively help companies navigate economic volatility and foster long-term loyalty in a highly competitive marketplace.

MARKET SEGMENTATION

This research report on the Europe luxury fashion market is segmented and sub-segmented into the following categories.

By Product

- Clothing & Apparel

- Footwear

- Accessories

By Consumer Group

By Distributional Channel

- Store-Based

- Non-Store Based

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey