March 24, 2026

As part of its community and economic development function, the Federal Reserve Bank of Atlanta regularly conducts listening sessions, convenings, and one-on-one interviews with social service, economic development, housing, and workforce development intermediaries to better understand the economic conditions of low- and moderate-income (LMI) households. We also engage directly with low- and moderate-income workers and consumers. The goal of our engagement efforts is to better understand barriers and opportunities for economic mobility and financial health. By the end of 2025, participants in these discussions consistently raised two central themes: (1) many low-income workers and job seekers felt discouraged about their ability to secure quality employment in a fragile labor market, and (2) many LMI households appear to have increased financial distress in recent months as expenses strain income.

For many workers and job seekers, concern about the stability of the labor market remains pervasive. While some workers we spoke with expressed confidence that they would be able to find a new position, if necessary, most indicated that the job would likely represent a downgrade in terms of wages, schedule, or benefits or all three. Most workers we interviewed were actively looking for jobs, regardless of employment status. Worker-serving organizations and job seekers alike reported that navigating the labor market has become harder. Many employed workers reported staying in less-than-ideal jobs because of the lack of better options—a phenomenon called ‘job hugging.’

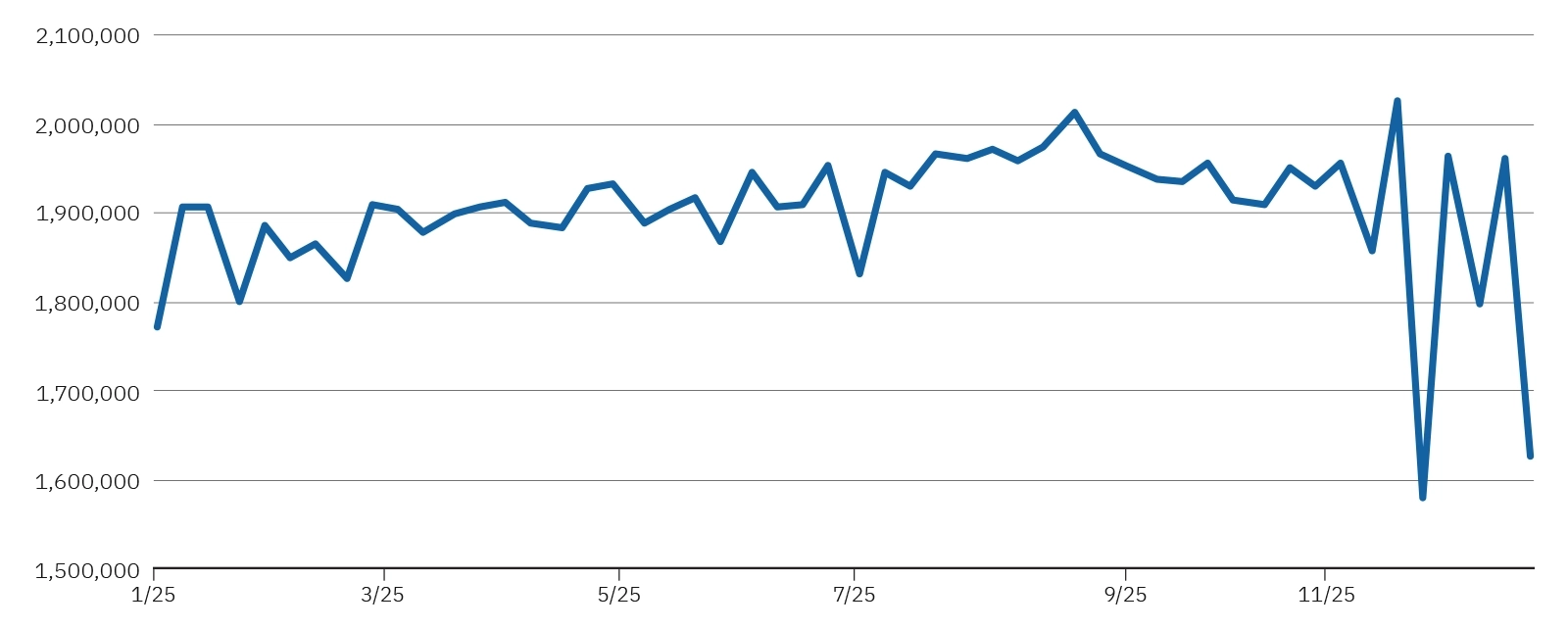

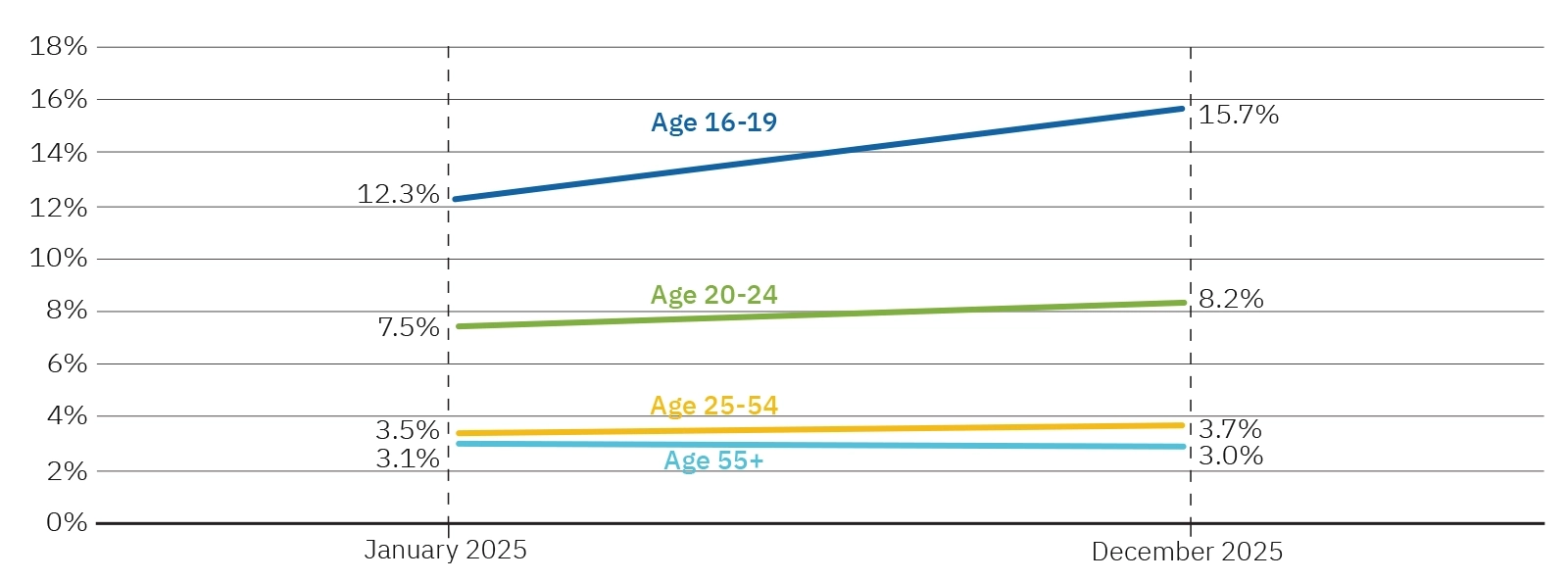

The perceived downturn of the labor market among these workers and job seekers reflects a real, if slight, slow down on the employment front. According to the Federal Reserve Bank of Atlanta’s Unemployment Claims Monitor, seasonally adjusted continued unemployment claims remained close to a post-pandemic high in November (though they have since fallen; see chart 1). Similarly, though the overall unemployment rate remains low relative to historical norms, at 4.4 percent it remains near its highest level since 2021 (see chart 2). The employment picture appears especially discouraging for younger workers. In December, according to data from the Bank’s Labor Report First Look, the unemployment rate for individuals between the ages of 16 and 19 approached 16 percent. Our workforce contacts confirmed this trend, reporting upticks in younger workers looking for employment.

Chart 1: Continued Unemployment Claims, Seasonally Adjusted

Chart 2: Unemployment Rate by Age

While workers, job seekers, and workforce representatives identified uncertainties in the labor market as a source of anxiety, price pressures appear to outweigh employment concerns. Many workers and job seekers reported feeling increasingly pinched by cost increases for a host of household expenses including groceries, energy, healthcare, and insurance. The cost of housing also continues to be a challenge for many individuals. According to the Atlanta Fed’s Home Ownership Affordability Monitor (HOAM), for example, the housing affordably gap remains near historic highs. Workers and job seekers alike reported tapping savings, credit extensions, buy-now pay-later options, and debt servicing to cover bills. Tighter household budgets have also forced many LMI households to cut back or eliminate dining out, use coupons more frequently, buy only in bulk, purchase marked-down food, and aggressively bargain hunt. Given this reality, combined with an unprecedented pause in Supplemental Nutrition Assistance Program (federal food assistance) in November 2025, it is perhaps unsurprising that calls to local 211 helplines connecting people to social assistance have increased in many cities across the Sixth District in recent months, including Atlanta, New Orleans, and Jacksonville.

The Atlanta Fed’s Community and Economic Development team, along with the Regional Economic Information Network, continually engages with workers, consumers, businesses, and social service providers to complement macroeconomic data with first-hand, on-the-ground insights. The Bank also continually publishes timely quantitative information on critical issues such as wage growth, labor force participation, and rental affordability. Ultimately, both qualitative information and quantitative data help us better understand the balance of employment versus price pressures on individuals and households, identify differences in populations across incomes, and highlight potential implications for household consumption patterns.

The views expressed here are those of the author’s and not necessarily those of the Federal Reserve Bank of Atlanta or the Federal Reserve System. Any remaining errors are the author’s responsibility.

The Federal Reserve Bank of Atlanta’s Community and Economic Development function supports the Central Bank’s mandate of stable prices and maximum employment by helping improve the economic opportunity of low- and moderate-income (LMI) individuals and underserved places for a stronger economy for all Americans. Community development is one of the Federal Reserve’s core functions and this responsibility is rooted in its mandates from Congress. Partners Update articles address community and economic development trends, issues, and events. Find more research, use data tools, and sign up for email updates at Community Economic and Development.