Larry Fink is the most powerful person in the financial markets, and that status is granted to him by BlackRock. As chairman and CEO of the world’s largest asset manager, he manages $14 trillion – the sum of all the assets owned by the firm’s individual and institutional investors. His business card opens any door. Political leaders, central bankers, regulators and businesspeople all want to hear from “the man behind the curtain,” as the business writer William D. Cohan called Fink in a comparison that references The Wizard of Oz. Indeed, his influence is highly coveted: unseen, yet pervasive. Fink, 73, was in Madrid last week, as part of a European tour. After meeting with clients at the Hotel Santo Mauro, the California-born financier gave an exclusive interview to EL PAÍS at the private Monteverdi club.

Question. The war in Iran has disrupted the entire economic landscape. What consequences do you think it will have for global growth and financial assets?

Answer. That’s a very hard question to answer. It will depend on how long the conflict lasts. Now, if the war ends, will it mean that Iran will cease to be a country that exports hostility and spreads instability throughout the region? Or will it continue to fund Hamas, Hezbollah and the Houthis? There are different outcomes that could have a profound impact on the global economy.

Q. And which scenario do you think is most likely?

A. If the outcome is that we have a more secure region and Iran opens to the world, the future valuation of oil will be much reduced from where it is today. But if Iran is still a hostile country, that’s a very different outcome. Maybe oil will be above where it is today. And so, to me, I can’t answer what the outcome of the war will be… but I’m an optimist, so I do believe that we’ll find a solution and that Iran can be part of the world community. When the export of energy [to the West] is allowed, then you could have lower prices. One of the leaders of one of the Gulf countries told me last week that, in 1979, Iran was much wealthier than Qatar, Saudi Arabia or the UAE. The regime has done a terrible job for its citizens. Hopefully, we can have an outcome [in which we see] a rebuilding of Iran for its citizens and for the world.

Q. Listening to you, it would seem that all the blame falls on Iran… but the United States and Israel initiated the attack. They must bear some responsibility for the solution, surely?

A. Yes. And the United States is taking responsibility. That’s why it has presented a plan to achieve peace.

Q. The war broke out at a time of record highs for the stock markets, with many companies trading at very high prices. Are you afraid that a prolonged conflict will cause the market to crash?

A. If the war drags on for a year, energy prices will rise even further and the global economy will enter a recession. And, in that case, stock markets would fall sharply, but that’s not a valuation issue. That’s a change of circumstances.

Q. Isn’t that too optimistic?

A. No. Revenues and profits are growing. Over time, do I believe markets are going to be higher? Yes. I know you need to sell newspapers. But focusing on today and tomorrow – instead of focusing on the next 10 years is really bad for most of the population of the world. If you were in Spain 20 years ago and you put your money in the Spanish stock market, you’d be two times wealthier than if you had kept your money in a bank account. But everybody’s talking about fear. And so, people hold on to too much money. What does it mean when a trillion euros are sitting in bank accounts? When you keep your money in a bank account, you don’t believe in your country. Just focusing on today is really bad for the health of the community. How do we make people more prosperous? It’s not about if the war lasts one or two more months or whatever.

Q. Many citizens would surely love to think 10 years ahead, as you suggest, but they’re too busy just trying to make ends meet.

A. Yes, there’s a segment that’s worrying about their paycheck every month, but you can’t tell me that the rise of the middle class hasn’t happened. I’m not here to deny that there are segments of society here in Spain, or in the United States, that are really struggling. That’s a fact. But 25 years ago, there might have been a higher share of the population that was struggling. If you look at the world today versus the world 30 years ago, the world is much more prosperous. But we don’t talk about the positives. We only talk about negatives. That’s why I’m an optimist, because most people are negative… and most people are wrong.

Q. First, it was the trade war. Then, the kidnapping of Nicolás Maduro. There have been threats made against Greenland, there’s a crisis within NATO… and now, we have the war in the Middle East. Is the United States the biggest destabilizing factor for the global economy?

A. I’m not going to answer that. I’m not here to talk about politics.

Q. Are American business leaders and executives afraid to talk about their country’s policies?

A. I don’t want to continue the interview talking about politics. There are many other topics to discuss.

Fink founded BlackRock in 1988 with eight partners. Today, it’s a giant with a market capitalization of $151 billion. The son of a shoemaker and a teacher, he holds a degree in Political Science from UCLA. He insists that he’s not a politician, but much of the asset manager’s power cannot be understood without considering BlackRock’s intricate web of intersecting public and private interests.

After the collapse of Lehman Brothers in 2008, the U.S. Treasury asked BlackRock for help managing the toxic assets that belonged to the nationalized entities. Years later, during the European debt crisis, the Greek government also hired the firm’s services.

In 2020, at the height of the Covid pandemic, the Federal Reserve turned to BlackRock, requesting that the company manage its bond-buying program. And today, this all-powerful entity is playing a significant role in Ukraine. Last January, the country’s president, Volodymyr Zelenskiy, held a conversation with Larry Fink, U.S. Treasury Secretary Scott Bessent and Donald Trump’s son-in-law Jared Kushner, which he made public. The agenda? To consider Ukraine’s future once the Russian invasion ends.

Q. Can you give us more details about your meeting with Zelenskiy?

A. We’ve been working with the Ukrainian government for the last three years, preparing for peace and organizing a platform in which governments and individuals – in the form of grants and private capital – can safely invest in the rebuilding of Ukraine. We need to make sure that, when we rebuild Ukraine, we do so in a way that ensures prosperity. There’s a long history of corruption in this country. And so, we need to rebuild Ukraine with the concept of eliminating as much corruption as possible. We don’t need more new oligarchs: we need to be building Ukraine for its people. Our mission is to create a prosperity fund, in which we can navigate and work with the Ukrainians on where the money should be directed. We’ve been doing this now for over three years, pro bono. We’re doing this to bring Ukraine back. Can you imagine a Europe with a strong Ukraine?

Q. What stage is the BlackRock-led fund for Ukraine’s reconstruction at?

A. It’s coming along. It hasn’t been finalized yet.

Q. How much money do you estimate is needed for the country’s reconstruction?

A. The numbers are wildly different. If the security agreement with NATO and the United States is absolute, that’s a very different outcome than if there’s uncertainty. In that case, Ukraine would need to spend a great deal of money on their military. That’s a big difference. But to give you a framework, it’s in the hundreds of billions of euros.

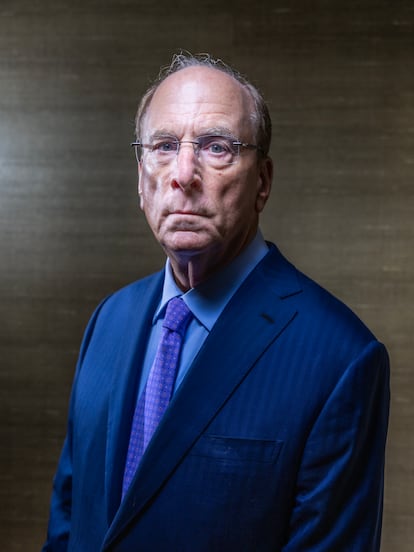

Minutes before his arrival, Fink’s security detail inspects the area. Averse to photos and thinner than the last time we saw him in 2023, he has a tan that would seem out of place in New York, where BlackRock is headquartered. He wears an impeccable custom-made pinstripe suit by the Italian firm Brioni. A prominent watch from the Swiss luxury brand IWC hangs from his left wrist. Amidst all this classicism, his ladybug cufflinks provide a cheerful contrast.

In 2024 (the latest available data), Fink’s salary was $36 million. However, his vast fortune – valued by Forbes at $1.3 billion – is due to BlackRock’s incredible stock market rise. The shares debuted on the stock exchange in 1999 at a price of $14 and currently trade at $982 per share. Like a modern-day version of the Apostle Paul and his letter to the Corinthians, Fink sends out a lengthy letter to investors each year, analyzing financial, energy, sociodemographic and geopolitical issues.

Q. Your annual letter was published on March 23. In it, you assert that the world is moving toward a phase in which each country or region will have to consider its own self-sufficiency. Does this mean that globalization, as we understand it, is over?

A. Globalization was largely established in the period following World War II, when the United States helped other countries rebuild from the calamity. Asymmetrical trade agreements were established, whereby Americans had to pay tariffs, while their partners enjoyed free access to their markets. That framework was fantastic, because it brought prosperity to millions of people around the world… but does it make sense for globalization to continue operating the same way it did 50 years ago? The answer is no. Those countries that the United States helped are now stronger. Maybe it’s time to return to a more symmetrical type of trade relationship.

Q. What economic consequences would this autonomy – which you believe each country should pursue – have?

A. Self-reliance – as my letter states– is more expensive. This is because globalization was done with the idea that we could get the cheapest things worldwide. But then, we became much too dependent on other entities. Maybe now we should manufacture chips in Europe or in the United States… maybe we’ve been too reliant on having only one country provide rare minerals. Maybe there should be multiple sources. All of this is just a recalibration. It doesn’t mean that globalization is over. I look at globalization as resilient, but it’s evolving to meet our needs. Self-sufficiency in areas like security and artificial intelligence (AI) is more expensive, but over time, it will be deflationary if each country can provide for its own basic needs.

Q. And what effect will this have on inequality? Since COVID-19, the global economy has grown significantly, but not everyone has benefited equally. How can this imbalance be addressed?

A. In my letter, I talk about how we have to [take another look] at Social Security. Social Security isn’t great: it’s a forced insurance policy. When you rely on it, you’re not growing with your country. There’s huge inequality because those who haven’t invested – those who’ve kept all their money in a bank account – or those who cannot meet their monthly needs are being left behind. Why is Europe growing so much slower than the United States? Much of this has to do with the fact that Europe doesn’t have a banking union. Europe doesn’t have an [integrated] capital market. In the United States, at least 60% of Americans are invested in the growth of their country. In Europe, the percentage of the population that invests in the stock market is far smaller.

Q. You’ve warned that the use of artificial intelligence could increase economic inequality. What needs to be done to prevent that?

A. We all know that AI is coming. The future is today. But we’re not doing anything about it: we’re just spinning. AI is going to reshape society. It’s going to create a huge amount of jobs and it’s going to remove a lot of jobs. We know that: we see the train, we see it leaving the station. What are we doing about it? How are we responding? We need to address these issues. We need to be forthright, working together with the government and trying to be prepared. AI is going to be very influential in our lives.

AI requires a lot of power. So, we need to be building out our power grids. We need a huge amount of capital for data centers. And, for a lot of people, this change is frightening, because it creates uncertainty. But we can eliminate a lot of the uncertainty by navigating our society to be prepared for this transformational technology. That, to me, is what we need to be doing: not wondering whether the war is going to be a two-week war, or if oil prices are $40 or $150 a barrel. That doesn’t matter as much as how we’re preparing ourselves for this technology that’s transforming the world. And the big issue is, if we don’t do it — Europe and the United States — China will. So, it’s not a question about whether AI will transform our lives. Rather, it’s about who will guide that transformation. And how.

There are few centers of power where Fink doesn’t play a leading role. Davos is a prime example. In 2026, as co-chair of the World Economic Forum, he has tried to revive the former glory of an event that, in recent years, has been marred by various scandals. His extensive agenda helped bring the cream of the global business community to the idyllic Swiss town this past January. He also secured the attendance of 65 heads of state, including Donald Trump himself, at an event whose theme this year (ironically) was “A Spirit of Dialogue.”

BlackRock’s success cannot be understood without considering its clearly predatory approach. Between 2006 and 2009, it made its major leap forward with the acquisition of Merrill Lynch Investment Management and Barclays Global Investors. These moves allowed the firm to achieve a leading position in the then-nascent passive fund management business, a strategy in which the manager doesn’t select individual companies to invest in, but simply replicates indices, resulting in much lower fees.

In recent years, BlackRock’s focus has shifted to growth in the alternative asset segment: private equity, private credit, infrastructure and real estate. To this end, it has invested heavily, acquiring companies like Global Infrastructure Partners (GIP), HPS Investment Partners and Preqin Ltd.

BlackRock began as a fixed-income specialist. However, over the years, it has diversified its portfolio. More than 50% of its assets are now invested in equities, according to data from the end of fiscal year 2025. But it also has exposure to cryptocurrencies, currencies, commodities, corporate debt and infrastructure projects. The firm has 22,000 employees in more than 30 countries. Small investors account for just 9% of its total assets under management, with the bulk of its business coming from institutional clients: private banks, pension funds, sovereign wealth funds and family offices (wealth management firms serving families with high net worths).

Q. Why this significant focus on unlisted assets?

A. As the markets have evolved, as the capital markets have grown, clients are now looking at private markets in the same way they look at public markets. And they’re blending their investments, utilizing some private investing and some public investing. And so, for us, we want to be working with our clients across the spectrum of passive and active investing, across private markets and public markets. In addition, we’re overlaying that with our technology system, Aladdin. And we also bought Preqin, which is a private markets data company, so we could have the proper risk analytics that help us understand the appropriate risk of both private markets and public markets. Therefore, what we do is offer clients the broadest possible range of investment products and solutions.

Q. This focus on alternative assets isn’t without its challenges. In recent months, BlackRock and other large asset managers have frozen redemptions for small investors in funds that specialize in corporate loans. The technology sector – especially AI-related companies – has raised hundreds of billions of dollars in funding rounds. However, the benefits of these investments will take time to materialize. Is the private credit market currently the biggest risk to the stability of the financial system?

A. No. This is another artificial debate fueled by the press. Let’s put this in context: the private credit market is worth $2.2 trillion. The retail portion of private credit is $300 billion. That is, it’s a small part of this industry. Furthermore, the first page of the prospectus (the disclosure document) for these retail products states that the fund’s structure limits redemptions to 5% per quarter. It’s not hidden; it’s not in the fine print. It’s on the first page of the prospectus and clearly states that you’re investing in a product that will provide you with higher returns, but less liquidity.

As always, the press only sees the most negative side of things. In the past quarter, we’ve had more subscriptions to this fund than redemptions; that is, we’re growing. And we’re going to honor what’s stated in the fund’s contract, because my fiduciary responsibility isn’t only to those investors who want to withdraw their money: I also have to act as a fiduciary for the majority of investors who invested in this structure, knowing that there’s a 5% limit. If I do more than that, then I’m going to get sued by those who want to stay in the fund.

Within this market segment, there are asset managers whose clients are all retail investors. They’re going to have problems [when redemptions are frozen]. So, is there short-term tension in the private credit market? Of course. But if you look at the default rates in private credit, they’re at normal levels. Some defaults come from fraudulent companies whose revenue model wasn’t what they claimed it was. But hey, that’s capitalism. We might have some short-term losses, but in the long run, the return that these funds pay out is the best option for investors willing to take the risk.

Q. The problem is that the industry is selling these products to people who may not be aware of the risks they’re taking. The marketing of alternative assets to small investors has been touted by the industry as the success of democratizing investment. However, this democratization also hides many dangers, don’t you think?

A. Fair point, yes. But that’s why it’s on the front page of the document. It’s not hidden. Getting back to AI: [when it comes to] most AI companies – especially some of the startups, like Anthropic or OpenAI – retail investors can’t invest in them [directly], because they’re private. So, I believe that if we can get a small percentage of retail investors to invest in these new companies, or in private credit, they’ll benefit over the long run. I’m not suggesting having a 20% allocation in privately-held firms… but why would it be bad to have a 5% allocation? The retail investor is emotional. We need to teach them about how to invest for the long term, because there’s no panic in the institutional market right now, only in the retail one.

Q. The private credit boom is closely linked to so-called “shadow banking.” Do you think supervision of these new lenders should be increased?

A. I think one of the big reasons why Europe hasn’t grown like the United States is because of that worry. Who came up with the word “shadow banking”? It’s a negative word. It portrays negativity. After the financial crisis [of 2008-2009], capital requirements for banks were raised by 20%, which meant 20% less credit for businesses. In the United States, because of the growth of the capital markets, the [country] was able to rebound faster. It took Europe about five [to] seven more years to rebound after 2009 because it has a weak capital market. Because people use the word “shadow banking.” BlackRock is regulated. So, the notion that I’m not regulated is crazy, it’s wrong. It’s misleading. The capital market is fully regulated.

Despite being over 70, Fink has no designated successor. Moreover, some of his potential heirs, whom the market was speculating about, have been leaving the company. The latest to depart was Mark Wiedman.

For now, BlackRock’s numbers put an end to any debate about his replacement. In 2025, the firm grew its revenue by 19%, to $24.216 billion, taking in $7.736 billion in just the fourth quarter alone.

Q. BlackRock was one of the pioneers of socially responsible investing (SRI) and environmental, social and corporate governance (ESG), making climate risk a central factor in its investment strategy. However, in 2023, the company announced that it was ceasing to use the term ESG, considering it too politicized. Does that mean that the climate crisis is no longer a risk for BlackRock?

A. In fact, this year, in my letter, I emphasized the need to invest more in solar energy. I don’t use the word ESG, but we do talk about decarbonization technology. We need to be more pragmatic regarding different energy sources. We talked earlier about increasing inequality, and one of the factors contributing to inequality is the rising cost of energy for the poorest segment of the population. [Previously], we were just focusing on one source of energy: renewables. And that raised the price on everybody. I talked about that in my letter to investors in 2022 and 2021, about the “green premium.” We haven’t created the technology to bring down the green premium. And so, the cost of decarbonization was a tax on everybody. And that’s just unacceptable in society today. With AI and the power it consumes, we need to have more pragmatic energy policies. That being said, today, BlackRock has just as many decarbonizing investments as we did three years ago. So, my language has changed, but our investment patterns have not.

Q. What’s your take on the Spanish economy? How do you assess the current government’s policies?

A. The Spanish economy has done quite well. It’s one of the outstanding growth areas of Europe. I’ve said this for the last 10 years: Spain has some of the greatest international companies in the world. It has great innovation. It has great companies and infrastructure. It has some of the best banks. I look at the resilience of Spain. It’s a great place to live. It’s a place that has excellent dynamism. And I’m not going to get into one politician versus another, but I can say that, over the last 10 years – beyond this present prime minister (Pedro Sánchez) – Spain has done many great things to improve itself. I would hope that other European countries look at Spain and see what the Spanish government has done to improve the future [outlook].

Q. You’ve set a goal of increasing BlackRock’s annual revenue to $35 billion by 2030. How do you plan to achieve this?

A. By supporting our clients, being a better steward of the money they entrust us with and offering the best investment solutions. Our ties with the countries where we operate – with their companies and with our clients – are becoming increasingly close. Our job is to reduce tensions and find the best long-term options. I don’t focus on the noise. Noise sells newspapers, but it’s detrimental for investing.

Q. Will the projected growth come from BlackRock’s acquisition of more companies?

A. It’s true that we’ve made some significant acquisitions in recent years, but I also want to emphasize our ability to grow without acquisitions. In the last five years, we’ve increased our assets under management by $5 trillion. To put that achievement into perspective: there isn’t a single fund manager in Europe with a size of $5 trillion.

Q. BlackRock currently manages $14 trillion. How can you prevent this enormous amount of money from leading to less efficient management of client funds?

A. We reflect the global economy. If it grows, we grow with it; if it contracts, our size will also decrease. I don’t think any other firm in financial services has understood the role of the capital markets as well as we have. And the second thing that BlackRock has is an enormous amount of technology: so, whether you’re a client who’s awarded us $1,000 or $100 billion, we have to treat each client the same. And we have to make sure that we have the technology to honor each and every client. One of the great foundational strengths of BlackRock is the undeniability that our technology is world-class.

Sign up for our weekly newsletter to get more English-language news coverage from EL PAÍS USA Edition