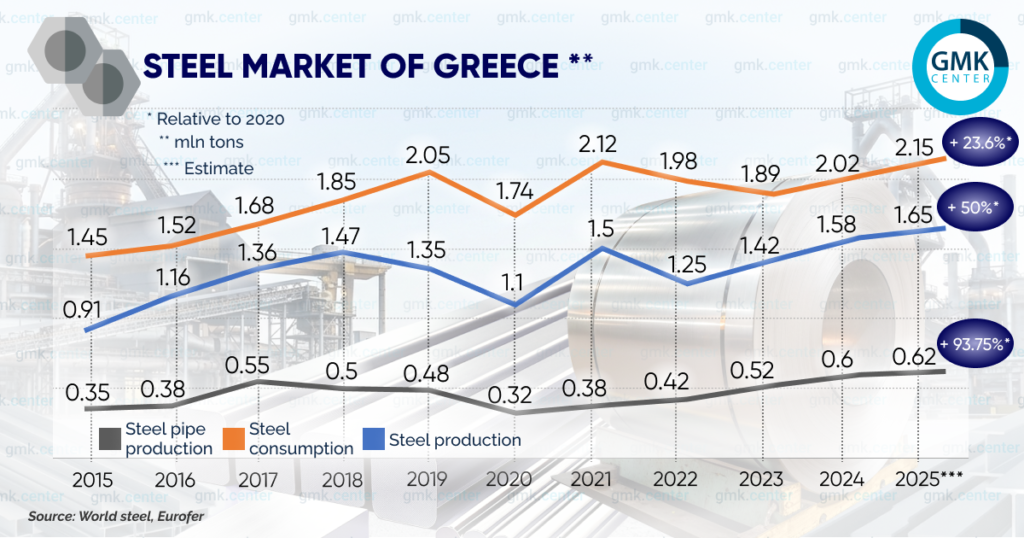

Demand for steel in Greece is slowly recovering after the default crisis of the 2010s

The economic downturn of 2008–2015, caused by a huge budget deficit, caused Greece’s GDP to plummet by 26.8% – to €177 billion. Gradually, the country managed to climb out of the debt abyss and return to a growth trajectory, which affected the consumption of finished steel. However, even now, the capacity of the steel market is still half of what it was before the crisis, which is often compared to the Great Depression of the 1930s in the United States.

Market profile

The main local player is the Viohalco holding company, which owns the Sidenor Steel electric steel mills in Thessaloniki and Sovel in Almiros with a total capacity of 2 million tons per year. The Hellenic Halyvourgia plant also has an active status. It has a small steel production volume and focuses mainly on rolling.

These manufacturers specialize in rebar, long products, and wire rod. Local production covers 85-90% of the market in this segment. The rest is accounted for by imports of specific steel beams from Italy, as well as rebar from Bulgaria and Turkey. It is purchased in the northern regions due to cheaper logistics compared to deliveries from Thessaloniki and Almiros.

In 2015–2018, when the construction industry was testing the bottom, Greek steel mills exported most of their products. Now they mainly work for the domestic market. Small volumes are shipped to the Balkan countries, Cyprus, and Libya.

An interesting fact: Viohalco used to periodically send steel billets to Egypt if the load on its own rolling capacities was less than the smelting capacity. Now, Greek steel mills themselves purchase additional billets in Bulgaria, where Viohalco also has steel production facilities.

The situation is different with flat rolled products. The only producer, Hellenic Steel in Elefsina, has not been operating since 2015, and the demand for sheet rolled products is covered by imports. Mostly hot-rolled coils and galvanized steel are supplied from Turkey ($339 million in 2024). In addition to beams, premium thick-gauge rolled products are delivered from Italy to Greece, which are purchased by shipyards ($192 million).

Sheet rolled products from Austria and France are high-tech steel for wind energy ($155 million and $153 million). China closes the top 5 importers with sales of $143 million. These are mainly steel products and cheap flat rolled products for the budget segment in construction and the production of household appliances.

Demand for flat rolled products

There is no machine building industry as such in Greece. Industrial consumption of steel sheets is provided by several industries, among which shipbuilding stands out. Until 2018, the situation was critical. Changes began after the acquisition of shipyards in Elefsina and Syros by the American Onex Group, owned by Greek-born businessman Panos Xenokostas.

Large-scale investments made it possible to resume ship repair first and foremost. As a result, Onex Neorion Shipyards and Onex Elefsina Shipyards significantly increased their purchases of thick steel sheets needed to replace ship hull structures.

The Greek Ministry of Defense’s program to build frigates for the local navy contributed to the revival of the industry. The French Naval Group became the general contractor, with most of the production taking place in France at the shipyard in Lorient. The Greek shipyard Salamis Shipyards is participating in the project by manufacturing individual sections of the hulls for these ships.

The first frigate, HS Kimon, was delivered to the customer in December 2025. The completion of the frigates HS Nearchos and HS Formion is scheduled for 2026.

The pipe industry is one of the main consumers of flat rolled products. The Corinth Pipeworks (CPW) plant, owned by Viohalco, has a capacity of 1 million tons per year and is one of the world’s leading manufacturers of large diameter pipes (LDP).

In 2024, the company reported a record portfolio of new orders. This made it possible to increase production in 2025 and boost strip purchases. CPW’s pipe production volumes now exceed the previous record set in 2017, when there was a peak in deliveries of large-diameter pipes for the TAP gas pipeline, even though there are no similar new landmark projects in Europe.

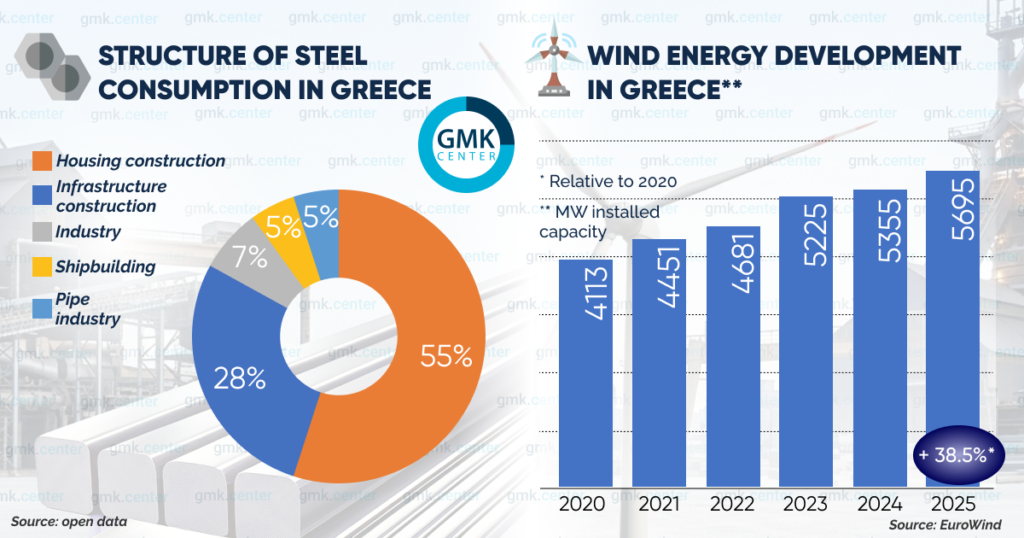

One of the main drivers of demand for flat rolled products is wind energy, which is developing rapidly in Greece. The level of localization during the construction of wind farms is quite high, at around 50%.

In particular, the Greek company EKME manufactures wind turbine tower sections at its own metalworking plants under a contract with the Danish wind turbine manufacturer Vestas. The reinforcement used is 100% Greek-made and is supplied by Sidenor Steel and Hellenic Halyvourgia. The steel for lattice towers and transformer substation buildings, which connect the wind farm to the grid, is also predominantly Greek.

The rest of the sheet steel consumption is accounted for by the production of household appliances. Greece is one of the leading manufacturers of solar water heaters, built-in appliances, and refrigeration equipment in the EU. Among the main buyers of finished rolled products are:

- DIMAS Solar – the largest manufacturer of solar water heaters in the country;

- Cosmosolar – the second largest player in the market;

- HELIONAL – a large factory producing solar water heaters in Thessaloniki;

- Pitsos (part of the Bosch/Siemens group) – leader in the built-in appliances and refrigerators segment for the Greek market;

- Pyramis – global player in the production of kitchen sinks and built-in appliances.

Demand for long-length rolled products

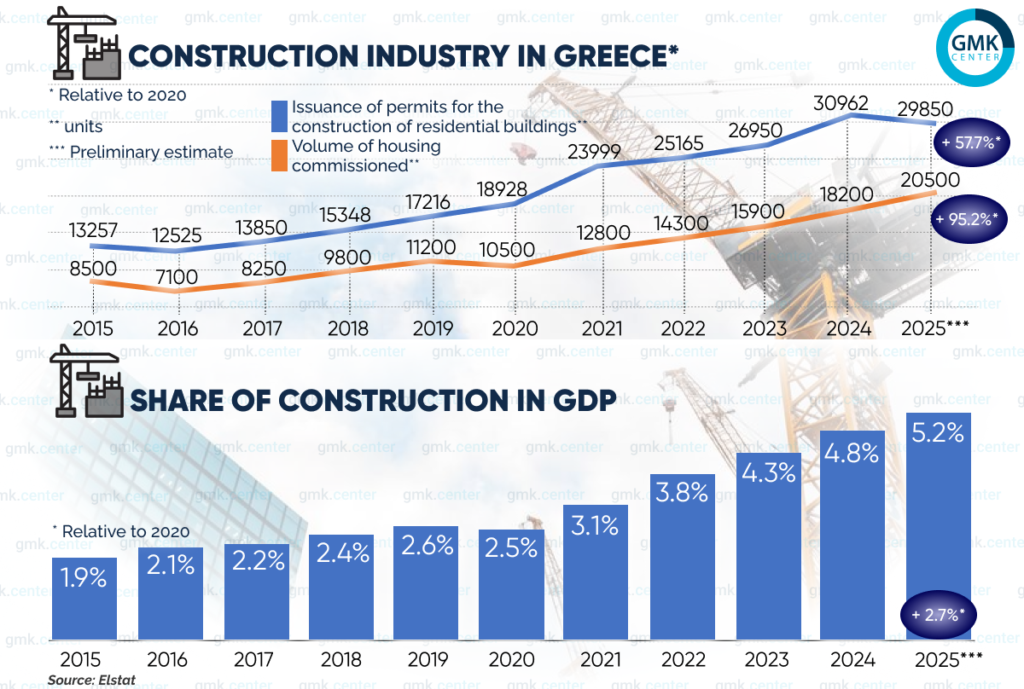

The construction industry, like the economy, is gradually recovering from the debt crisis. However, even now, market volumes are half of the peak recorded in 2006.

The residential sector is the main consumer of rebar and rolled steel, accounting for approximately 45% of all sales. It partially overlaps with the third largest consumer, the tourism sector, which accounts for almost 15%. Some villas and boutique hotels are registered by their owners as ordinary residential buildings.

Since 2021, the pace of residential construction has accelerated sharply. The Golden Visa program, which grants a residence permit in exchange for an investment of at least €250,000, has contributed to the mass construction of apartments for citizens of China, Israel, and Arab countries.

Another driver was the Spiti Mou («My Home») state program, which was active in 2023–2024. It provided government-subsidized mortgage loans for young people at a rate of 1–1.5%.

Greek banks ran aggressive marketing campaigns in 2022, offering fixed mortgage rates of 3–3.5%, while the EU average was 5–6%. The housing sector in Greece continued to grow even when most EU countries were experiencing a decline.

The revival of infrastructure construction, which accounts for approximately 40% of long-term rolled steel consumption, began after 2020 with the advent of European budget financing programs (RRF). Among the largest projects are:

- Interconnection of the power systems of the islands of Serifos, Milos, Santorini, and Folegandros. A large amount of galvanized steel is used here for supports and protective structures during cable laying and substation construction.

- Construction of the fourth line of the Athens metro. This creates a steady demand for reinforcement for tunnels and deep-level stations. The tunnel laying phase is scheduled to be completed by the end of the year.

- Construction of the Flyover flyover over the ring road in Thessaloniki. This is one of the largest consumers of bridge steel structures.

The Ellinikon megaproject stands out in particular—the construction of Europe’s largest “smart” city on the site of the former airport of the same name near Athens. It combines residential (skyscraper construction) and infrastructure construction. Colossal amounts of long-length rolled steel are used here.

Such buildings consume 2–2.5 times more steel than a typical five-story building. Due to the high seismicity in Greece, the strictest technical requirements for building strength (Eurocode 8 standard) apply. An average of 45–55 kg of reinforcement is used per 1 m² of living space, and for skyscrapers, this figure is 80–100 kg/m².

The buildings in Ellinikon (in particular, the Riviera Tower with a planned height of 200 m) are comparable to infrastructure projects in terms of steel consumption, but the infrastructure projects themselves are even more ambitious. The underground section of Poseidonos Avenue alone is worth mentioning — a 2.5 km long tunnel. Sidenor Steel is the exclusive supplier of reinforcement and rolled steel for Ellinikon.

Consumption outlook: flat rolled products

The revival of Greek shipbuilding continues. In December 2025, Onex Shipyards signed its first commercial contract for new construction in Greece in several decades. The agreement provides for the construction of four harbor tugs.

At the end of last year, the Greek Ministry of Defense ordered the construction of a fourth frigate from Naval Group. Salamis Shipyards will likely retain its status as a subcontractor for this project.

Wind energy is developing at a pace that exceeds the national target of 7 GW of installed wind power capacity by 2030. According to the most conservative estimates, it will reach 6.1–6.2 GW by the end of 2026. If Greek bureaucracy loosens its grip a little, the annual figure could be significantly higher. Currently, projects exceeding 1.1 GW already have contracts, but final permits are required to connect to the power grid.

CPW’s demand for strips has all the prerequisites for growth. One of the EU’s largest gas transmission system operators, Gasunie, through its subsidiaries Gasunie Netherlands and Gasunie Germany, completed a large-scale tender in December 2025 for the purchase of TBD for hydrogen (H2), gas (NG), and carbon dioxide (CO2) infrastructure. As a result, CPW was officially selected as a strategic supplier. The contract is valid for four years with the possibility of renewal for a similar period.

These are the main drivers of demand growth for flat rolled products in 2026. As for Greek manufacturers of household appliances, they confidently occupy niche market segments where it is very difficult to displace such manufacturers. This implies at least stable steel consumption on their part.

Consumption outlook: long products

The construction boom in Greece will continue in 2026–2027, which will require additional volumes of long products. A distinctive feature of the Greek housing market is that construction takes a long time. The period from excavation to completion of a finished building averages 2–2.5 years (in neighboring Bulgaria, it is 1.5–2 years). Therefore, the record volumes of new residential space commissioned in 2025 were achieved on the basis of permits issued back in 2023.

The construction of buildings for which the maximum number of permits was issued in 2024 will be completed this year. Considering that in 2024 developers received permits to build 7.2 million m² of residential space, and in the first half of 2025 another 3.1 million m², the potential for steel consumption by the residential sector alone in 2026 is approximately 519,000 tons. Among the current market drivers, the following can be highlighted:

- The minimum investment threshold for obtaining a «golden visa» has been raised to €800,000 in popular regions and €400,000 in others, effective September 1, 2024. As a result, instead of foreign individuals, large investment funds from Israel, the UAE, and Northern Europe are now the main buyers of new housing in Greece. They are purchasing entire residential complexes with ready-made infrastructure rather than individual apartments.

- In 2025, Greece set a historic record in tourism, welcoming an estimated 37.98-40 million visitors. This contributed to the construction of new villas and boutique hotels, which are registered as residential buildings.

- The government launched the Spiti Mou II program. Its funding was doubled to €2 billion. Half of the funds are provided by the European Union. The age limit for participation has been extended from 39 to 50 years. A loan of up to €190,000 is provided at 0% for half of the amount (at the expense of the RRF) and at a low interest rate for the second half.

- In November 2025, the government extended the VAT exemption (base rate 24%) for new buildings until the end of 2026. Developers are trying to make the most of this window of opportunity.

Infrastructure construction will continue and expand. This year, there are plans to start construction of a new branch of the second line of the Athens metro towards the Ilion district, as well as the reconstruction of port infrastructure. Ellinikon and other projects are still far from completion.

Given this, steel consumption in Greece could grow to 2.25–2.3 million tons in 2026. Imports of flat products from non-EU countries (primarily Turkey and China) will decline by approximately 25–30% under the influence of CBAM.