Photo Credit: Dave Hoefler via Unsplash

This is the fourth installment in a blog series from CA FWD and Insurance for Good. CA FWD and Insurance for Good have partnered to develop an actionable guidebook that outlines replicable funding and financing strategies for risk reduction and resilience. Special thanks to Shalini Vajjhala and Caroline George at PRE Collective for this guest contribution.

By Shalini Vajjhala and Caroline George

Capital planning in most sectors starts with, well, capital. Available resources are allocated based on needs. Projects are planned around anticipated costs and benefits. Stakeholders are engaged and aligned as a project unfolds. For climate adaptation and resilience finance, this process works in reverse. Capital follows motivated beneficiaries and robust data.

In many ways, the business case for resilience looks more like preventative healthcare or early childhood education than traditional capital planning or infrastructure finance. Early action creates the greatest value. There are both direct, individual beneficiaries and diffuse, indirect beneficiaries. Benefits accrue over long timeframes. Progress depends on sustained, coordinated investment over time. Success comes in the form of both financial gains and reduced future losses. In other words, success looks like a bad outcome that didn’t happen: a disease caught early, lower school dropout rates, a storm or wildfire that didn’t devastate a region.

For these types of projects, finance starts on the drawing board. The strongest business cases are shaped in predevelopment, the earliest stage of project framing and design. In the absence of an upfront business case, preventative investments are treated as public goods requiring public funding. Importantly, this happens even when projects and programs generate significant private financial value. The result is a constant scramble for scarce philanthropic grants and public funding.

Breaking this cycle and mobilizing more capital for resilience requires attention to two key dimensions of project finance:

- Degree of alignment across project beneficiaries (motivated payors).

- Level of confidence in the financial value of risk reduction measures (repayment pathways).

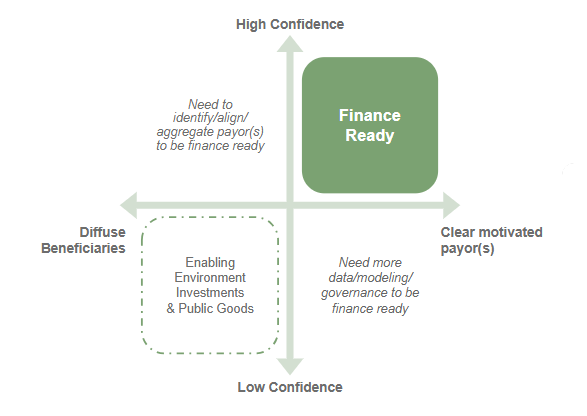

The most effective predevelopment processes start by identifying where opportunities sit along the two axes in Figure 1, the alignment of beneficiaries (x-axis) and the confidence in the financial value of risk reduction outcomes (y-axis). This provides a clear picture of finance readiness and the necessary steps to walk from needs to ideas to projects to capital. For example, opportunities in the top right quadrant with clear, well-defined beneficiaries who are willing and able to pay for resilience and robustly quantified financial benefits can readily attract private financing. In contrast, projects in the bottom-left quadrant that serve diverse and diffuse beneficiaries and have more uncertainty around the financial value of the proposed risk reductions are more likely to require grants or other funding to first fill data gaps, align beneficiaries, and/or aggregate benefits to demonstrate that repayment is possible for future financing.

Figure 1. Dimensions of Resilience Funding & Finance

The goal isn’t to move all resilience projects toward financing, but rather to make sure that financeable projects don’t deplete scarce resources for essential, harder-to-finance activities, such as planning and capacity building. Making effective transitions from funding to financing — moving across quadrants in Figure 1 — depends on three core predevelopment activities: (1) identifying and aligning beneficiaries; (2) building borrower, lender and investor confidence; and (3) sequencing “colors of money” as projects unfold. Below are examples of how PRE Collective iteratively works through each of these core predevelopment activities.

Identifying and Aligning Beneficiaries

Because the biggest benefits of investing in resilience often come in the form of reduced long-term risk and costs, predevelopment starts with identifying and aligning motivated stakeholders who are willing to pay for a risk reduction benefit. We do this by asking two simple questions:

- Who loses money (today and in the future) if nothing is done about this risk?

- Who suffers most (today and in the future) if we don’t address this problem?

The overlap between these two questions offers an entry point for equity-centered project development. When the answer to the first question points to a single large beneficiary (or a small number of motivated actors), there is an opportunity to build a direct business case for action. The ideal is for this business case to also create positive externalities that reduce suffering for those without the financial capacity to address the problem, for example, families living with mold in their homes after recurring floods.

If costs/benefits are spread out more widely, these are risks that are typically “everyone’s problem, no one’s job.” In these cases, additional time and resources are often required to align larger groups of beneficiaries, for example, with shared governance models. A key part of this process is focusing on specific financial beneficiaries over broad characterizations of benefits and finding the smallest possible number of motivated beneficiaries that can drive large projects forward to both capture financial value and reduce suffering. The most effective and equitable predevelopment keeps sight of both of these questions and generates project opportunities at the intersection of both.

Building Borrower, Lender, and Investor Confidence

The next element of climate adaptation and resilience focused predevelopment is to refine a proposed intervention, estimate anticipated physical risk reductions, and generate preliminary financial projections. Adapting to climate change will require a wide range of interventions to reduce short- and long-term risks across various perils — wildfire, flooding, wind, severe storms. Interventions can range from engineered solutions, such as coastal flood barriers, to ecological interventions, like wetlands and mangroves, to planning and capacity building. The effectiveness of many of these measures for delivering quantifiable savings or financial risk reductions has yet to be demonstrated for private investors or insurance markets.

Take for example, safe driver discounts or life insurance discounts for quitting smoking. In these cases, insurance providers have enough data on the individual and societal costs of unsafe driving and smoking that they can clearly reward behaviors that reduce risk with lower insurance premiums. By contrast, exercising regularly also has widely noted benefits, but there is more variability in physical impacts and uncertainty around the financial value of different actions. Although getting a gym membership doesn’t measurably change your risk, in and of itself, it can make it more likely that effective risk reduction behaviors and investments will follow. Similarly, investing in strengthening enabling conditions, like building code enforcement and contractor training, can have broad follow-on benefits.

Making the case for specific resilience interventions requires a clear picture of where available baseline data and models can show the financial value attributable to an intervention and build confidence in a project as an investment opportunity, and where perceived and real uncertainty will limit financial readiness.

Sequencing Colors of Money

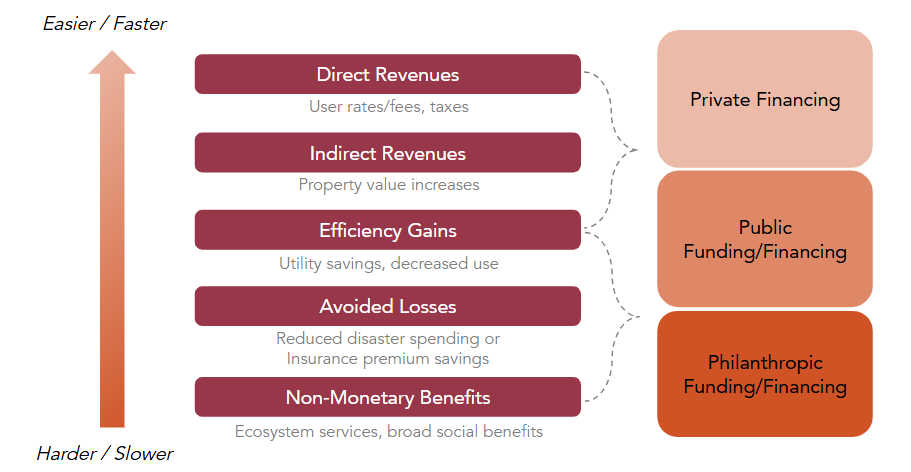

The third core predevelopment activity involves identifying and sequencing the most efficient and accessible forms of capital for each relevant stage of project development. Unlike traditional project finance, resilience finance requires more early work to quantify the benefits of specific investments and capture their financial value. This means that upfront funding is often necessary to enable future financing. Figure 2 highlights where resilience projects that are not associated with direct revenue streams are likely to require a combination of early-stage philanthropic “catalyst” grants and public funds for project design and development to open the door to private capital.

Figure 2. Matching Capital Sources with Resilience Benefits

Resilience projects and programs often start long before the feasibility stage of traditional projects. How projects are framed at this early stage can determine whether financing is even an option.